Buy Bharat Electronics Ltd for the Target Rs 510 by Motilal Oswal Financial Services Ltd

Decent performance

Bharat Electronics’ (BHE) 4QFY26 revenue/EBITDA/PAT came in line with our estimates, driven by strong execution and better-than-expected margins. Its order inflows for FY26 stood at INR300b, ahead of its own guidance. Margin performance for the year remained strong at 29%; however, NWC increased on lower customer advances and higher receivables. Going ahead, the company expects QRSAM order to be awarded by Jun-Jul’26. BHE remains a key beneficiary of large platform orders across Army, Navy, and Airforce, and with a strong addressable market, BHE can sustain revenue growth of 15%+ over the next few years. With improved indigenization levels and operating leverage benefits, we expect BHE’s strong margin performance to continue. We marginally tweak our estimates and expect a CAGR of 17%/17% in revenue/PAT over FY26-28. Maintain BUY with a revised TP of INR510 based on 45x Mar’28E EPS (INR520 earlier).

Decent set of results, in line with our estimates

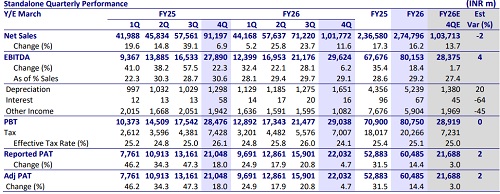

BHE reported a decent set of results in 4QFY26, broadly in line with our estimates. Revenue grew 12% YoY to INR102b, supported by a strong opening order book of INR730b. Gross margin expanded 40bp YoY to 48.2% (170bp higher than our estimates). Absolute EBITDA increased 6% YoY to INR29.6b (vs. our est. of INR28.4b), while margin contracted 150bp YoY to 29.1% (vs. our estimate of 27.4%), mainly due to higher other expenses. PAT rose 5% YoY on a high base to INR22b, in line with our estimates. Order book as of FY26-end stood at INR739b, with an order inflow of ~INR300b during the year. For FY26, revenue/EBITDA/PAT grew 16%/18%/14% YoY, while margin expanded 60bp YoY to 29.2%. OCF increased 211% YoY to INR14.9b, while the company reported FCF inflow of INR5b in FY26 vs. FCF outflow of INR5b in FY25

Current order book composition

BHE’s order book stood at INR739b as of Mar’26, providing strong multi-year execution visibility. Major projects include electronic fuses (INR43b executable over seven years), LRSAM orders (INR35b), LCA Mk1A-related systems (INR32b), BMP-2 upgrades (INR28b), Ashwini radar (INR24.6b), Mi-17V5 EW suites (INR22b) and spare/services contracts (INR25b). Most programs are executable over the next 1-3 years, while select long-gestation projects such as electronic fuses extend over a longer horizon.

Pipeline remains strong with large orders expected in near term

BHE’s near-term order pipeline remains strong across missile systems, naval electronics, EW systems and strategic defense programs. The company expects order inflows exceeding INR550b in FY27 (including QRSAM). Beyond QRSAM, key opportunities include order from projects such as Next-Generation Corvette (NGC), Shatrughat and Samaghat EW systems, P75I submarine, Hammer, Shakti Phase-4 and naval multi-function radar (MFR). The company also highlighted large opportunities emerging in indigenous data center solutions, where initial opportunities could range around INR10b-50b, while broader fully indigenous data center projects may eventually scale up toward INR100b.

Financial outlook and valuation

We marginally trim our estimates by 1% each for FY27/FY28 and expect a CAGR of 17%/16%/17% in sales/ EBITDA/PAT over FY26-28. We expect OCF/FCF to remain strong, led by control over working capital. BHE is currently trading at 43.0x/36.6x on FY27E/FY28E EPS. We arrive at a revised TP of INR510, based on 45x two-year forward earnings. Maintain BUY.

Key risks and concerns

A slowdown in order inflows from the defense and non-defense segments, intensified competition, further delays in the finalization of large tenders, a sharp rise in commodity prices, and delays in payments from the MoD can adversely impact our estimates on revenue, margins, and cash flows.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412