Neutral ITC Ltd for the Target Rs. 300 by Motilal Oswal Financial Services Ltd

Cigarette earnings under a cloud; remain cautious

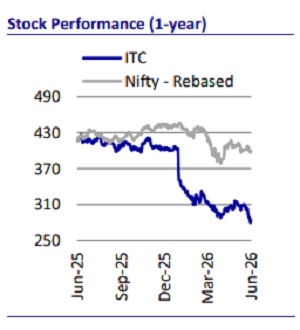

Effective 1st Feb’26, the cigarette industry is witnessing one of its most disruptive regulatory resets after the implementation of GST 2.0. The revised taxation framework has resulted in an estimated 60-65% surge in cigarette taxes for ITC, implying the need for around 35% hike in MRPs (at historical mix). This was the steepest hike seen historically and a sharp departure from the largely stable tax regime maintained during 2018-25. The transition has also been unusual due to the one-month gap between the announcement (1st Jan’26) and the implementation (1st Feb’26), compared to the typical immediate or near-immediate execution seen historically. In response, ITC has adopted a calibrated and phased price hike strategy instead of taking an upfront full tax pass-through, with the objective of limiting the shift toward illicit cigarette markets and retaining market share among legal players.

* We believe the current phase can be viewed in two stages. The first stage represents a transitionary adjustment period wherein ITC is gradually taking price increases to eventually reach tax-neutral levels. During this phase, the company focuses on balancing steady price hikes and market share protection while continuously assessing consumer response, competitive actions, and illicit trade dynamics across markets. Although this strategy may temporarily hurt cigarette unit economics and margins, it reduces the risk of sharp consumer disruption that could emerge from an immediate steep price reset.

* The second stage is likely to emerge once the full tax increase is absorbed into retail prices and the competitive equilibrium between legal and illicit trade stabilizes. By then, the extent of consumer dropouts, particularly among price-sensitive segments, should become clearer, enabling the industry to operate in a more predictable demand environment.

* We expect volatility in cigarette volumes and EBIT to moderate from the initial transitionary phase. In this normalized phase, ITC’s product portfolio, innovation pipeline, and premiumization strategy will play a critical role in rebuilding the growth momentum and defending its market positioning. Given the MRP revisions are still underway, the outlook for ITC’s cigarette business remains uncertain. We do not rule out any possibility for further earnings cuts. That said, the extent of consumer acceptance for revised prices will be a key monitorable. We model 15% revenue decline and 19% dip in EBIT in the cigarette business in FY27.

* ITC’s non-cigarette business continues to exhibit structural improvement. FMCG remains a key growth driver, with FY26 revenue of INR243b, implying a ~10% CAGR over FY19-26, alongside EBITDA margin expansion of ~450bp to 10% over same period. The portfolio now has four franchises with consumer spends in the INR20-50b range, reflecting increasing scale and diversification. We model a 10% revenue CAGR over FY26-28E for the segment. Meanwhile, Agri and Paperboards are positioned for a gradual recovery.

* Positive catalysts such as improving FMCG performance and paperboard margin normalization are overshadowed by the cigarette earnings headwind stemming from illicit competition, constrained pricing flexibility, and the inevitable volume-versusmargin trade-off that defines ITC's near-term trajectory. We maintain our Neutral rating with an SoTP-based TP of INR300 (18x Mar'28E EPS).

First stage - Transitory phase of pricing post tax hike

* The revised cigarette taxation structure marks one of the sharpest hikes historically. Based on our estimates, ITC may require a >35% MRP hike (based on historical mix) across its portfolio to remain EBIT neutral.

* The revised structure is expected to increase the aggregate tax on cigarette MRP to ~65%, marking one of the sharpest tax hikes historically. This steep revision comes after nearly eight years (2018-2025) of a relatively stable taxation regime (post GST), during which ITC delivered a healthy 4-5% cigarette volume CAGR.

* ITC has adopted a calibrated pricing strategy to focus on protecting market share rather than fully passing on tax hikes immediately. Unlike history, where full price hikes were immediate after the tax increase, ITC has been following up with steady increases to avoid losing market share to illegal players. Moreover, ITC is taking a portfolio-wide approach, launching higher-length brands into lower lengths to maintain the same consumer price for the brand.

Channel checks indicate cautious pricing actions amid downtrading risks

* While the revised tax was implemented in Feb’26, old stock continued to be sold in the market through April and in May in select regions.

* To manage the impact of taxation and maintain price points, manufacturers are reducing the physical length of cigarettes. Godfrey has already transitioned its Four Square Clove Crush brand from 69mm to 64mm. This new 64mm version was launched around late March or early April with a revised MRP of INR85 (pack of 10). ITC has launched a 74mm version for its key 84mm brands like Ultra Mild, Ice Burst, etc. for INR17.5 per stick.

Second stage – Tax neutral, illegal share gain will be watchful

* After the full tax pass-on, it will be critical to see portfolio changes, share loss to illegal, downtrading, etc. Given the unprecedented price hike, it is difficult to assess the deceleration in the industry volumes, consumer drop-outs to illegal brands, and product mix changes.

* Stable taxes during 2021-2025 impacted illegal brands, with a 150bp fall in the illegal market. However, with the recent price hike, there is a significant price gap between legal and illegal brands. Given the historical learnings, it will impact the legal industry’s cigarette volume. The illicit cigarette industry saw strong gains during 2012-2021, with almost 1,000bp gain to ~28% volume mix.

We estimate EBIT contraction of 19% in FY27

* ITC delivered a ~4% volume CAGR over 2018-25; however, recent tax hikes could weigh on near-term volume, keeping growth subdued. We expect cigarette volume to decline 10% in FY27E and to remain flat in FY28E.

* On the EBIT front, the high price differential after the tax increase constrains pricing flexibility, making it challenging to drive earnings growth.

* We model 15% revenue decline and 19% dip in EBIT in the cigarette business for FY27. We model a negative EBIT CAGR of ~8% for the cigarette segment over FY26-28E.

Other FMCG business: Operating metrics continue to optimize

* ITC’s FMCG Others segment now the second-largest contributor to ITC’s revenue, has demonstrated consistent double-digit growth and steady margin expansion, outperforming most staple peers despite a challenging demand environment.

* Growth momentum has been robust, with FMCG Others delivering a revenue CAGR of 10% over FY19-26. We expect the same CAGR over FY26-28E. With revenue at INR243b in FY26, ITC FMCG segment is the fourth-largest consumer business in our coverage universe, behind Titan, HUL and Asian Paints.

* Over the years, margin delivery has remained resilient despite high commodity costs, in contrast to peers. EBIT margins have continued to expand, supported by structural levers premiumization, scale benefits and operating leverage.

Agri and Paperboards businesses set for steady recovery

* The Agri business delivered a strong revenue CAGR of 12% over FY19-26, led by leaf tobacco and value-added products. FY26 was impacted by geopolitical disruptions (such as US tariffs and regional conflicts) and domestic regulatory measures, including stock limits and export restrictions on key agricommodities. Over FY26-28E, we model ~14% revenue CAGR and stable EBIT margins of ~7.5%.

* The Paperboards, Paper & Packaging business remains affected by cheap supplies from China and Indonesia in global markets (including India), as well as weak demand conditions. Higher wood prices have been adversely impacting the segment’s profitability for the last couple of years. However, wood prices showed signs of moderation in 2HFY26 and we expect a gradual recovery ahead.

* To strengthen its Paper business, ITC has announced the acquisition of the Century Pulp and Paper undertaking from Aditya Birla Real Estate for up to INR35b. The acquisition is aligned with the company’s ITC Next strategy and is expected to address capacity constraints, accelerate scale-up versus greenfield expansion, and improve supply-chain access to northern markets.

Valuation and view

* Historically, ITC has taken immediate price increases to stay EBIT-neutral. However, given the quantum of tax increase this time, this approach is unlikely.

* We expect 10% volume decline in FY27E and flat volume in FY28E in cigarette segment. Earnings pressure on cigarettes would take away near-term catalysts (improving FMCG and Paper). Valuations remain comfortable however we do not see any near-term positive catalyst.

* ITC has a full cigarette portfolio to better navigate the tax hike, but competitive pressure from illicit cigarettes will weigh on the formal cigarette industry.

* We did a bull/bear scenario analysis (link) for ITC. In the bear case, full passthrough of the steep tax hike could trigger sharp price-led revenue decline (~20%) and ~28% EBIT contraction due to an accelerated shift toward illicit cigarettes. Conversely, the bull case assumes better consumer absorption and limited downtrading, restricting revenue decline to ~8% and a moderate cigarette EBIT decline of ~11%, supported by price/mix benefits. ? We maintain our Neutral rating on ITC with our SoTP-based TP of INR300 (implying 18x Mar’28E P/E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412