Buy Gabriel India Ltd for the Target Rs 1,266 by Motilal Oswal Financial Services Ltd

Transforming into a scalable mobility platform

* Gabriel India (GABR) has, for nearly six decades, operated as a single-product suspension player, which inherently constrained its scalability. The company is now undergoing a structural transformation into a diversified mobility platform with a significantly larger growth runway. Over the past two years, management has adopted a more aggressive stance (the group’s aspiration to scale revenues to INR500b by 2030), with plans to launch at least one new product annually and expand into adjacencies such as sunroofs, solar dampers, and e-mobility.

* While the Anand Group has historically diversified across multiple verticals through global partnerships, much of this value remained outside GABR. This is now changing, with GABR being positioned as the primary growth vehicle for the group, as evidenced by the recent restructuring initiatives (integration of Dana and Henkel) and JVs (Enmove and Jinhap) being routed through the listed entity. These initiatives are driving long-term shareholder wealth creation. We initiate coverage on GABR with a BUY rating and a TP of INR1266, based on 35x FY28E.

Key investment thesis

* Gaining SOB in the suspension business: GABR has consistently outperformed the industry (~10% CAGR vs ~4%) and is well positioned to sustain this momentum, with growth driven by new customer additions (added Hero Motocorp- SOP from 2HFY27E) and rising share of its business with MSIL (company has order wins from multiple new platforms), TMPV (company has won new EV model), and premiumization.

* Strategic integration of Dana Anand to drive scale: Dana Anand is a premier driveline player with a market-leading position in PV, CV, and offhighway segments (estimated- 30-40% market share), and supplies to key OEMs such as M&M, MSIL, and Tata Motors. The company is being positioned as an export hub for Dana global entities.

* Broadening market presence through the Henkel Anand India integration: Henkel Anand is one of India’s leading automotive adhesive players, supplying key OEMs such as MSIL and TMPV. Henkel could benefit from a gradual increase in content per vehicle driven by SUV premiumization, EV adoption, and rising use of multi-material vehicle architectures.

* Building the next growth pillars: GABR is diversifying beyond suspensions via adjacencies and JVs. Inalfa gains from increase in penetration of sunroof in India. Jinhap (fasteners) and SK Enmove (lubricants) expand into import substitution and large aftermarket-driven segments. Together, these initiatives broaden increase CPV, and strengthen long-term scalability.

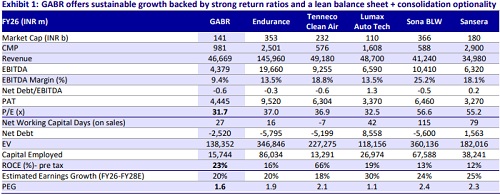

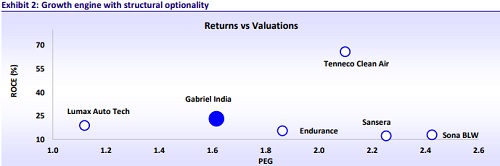

* Robust financials support growth: GABR has a net cash balance sheet, lean working capital (~27 days), and strong return ratios (~30% core ROCE). Cash conversion is robust (10-year net CFO/EBITDA ~81%, FCF/PAT ~61%), while consistent dividends (more than 20% payout) reflects the company’s ability to generate and return surplus cash to shareholders across business cycles.

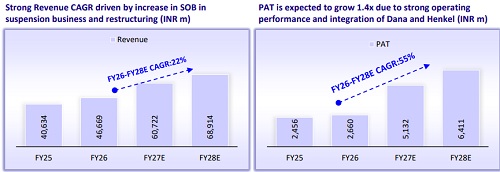

* We estimate a Revenue/EBITDA/PAT CAGR of 22%/23%/55% earnings CAGR for the consolidated business (FY26-FY28E), primarily driven by increase in SOB with customers and restructuring. We estimate the Core ROCE of the company to expand by 800bps to 37.7% and ROE to expand by 780 bps to 28.4% by FY28E. We initiate coverage on GABR with a BUY rating and a TP of INR1,266, based on 35x FY28E. Further group consolidation could unlock significant upside, with unlisted Anand Group ventures (having a PAT of INR2.3b) potentially equivalent to the value of GABR’s standalone suspension business.

A premium to its historical average one-year forward multiple is warranted by:

1) restructuring-led earnings growth

2) Gabriel’s emergence as the group’s primary growth platform for future restructuring and JV opportunities

* Key risks:

1) Rise in competitive intensity

2) Fluctuations in commodity prices

3) Changes in technology

4) Continued geopolitical headwinds causing slowdown in end markets

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412