Buy Cummins India Ltd for the Target Rs 6,600 by Motilal Oswal Financial Services Ltd

Powering balanced growth

We hosted Cummins management for investor meetings. Here are the key takeaways: The company’s key business segment, Powergen, continues to benefit from strong industry tailwinds on both non-HHP and HHP sides. A strong installed base, a wide product portfolio and higher geographical penetration continue to provide a stable stream of distribution revenue. Industrial segment is growing selectively, while exports are stable across larger geographies with a little cautious approach toward the Middle Eastern markets. We expect overall EBITDA margin to remain strong on a healthy revenue mix despite higher RM prices, which are currently passed through to clients. We maintain our estimates and retain BUY with an unchanged TP of INR6,600, based on an average P/E of 45x and DCF on Sep’28 estimates, which will capture long-term gains from high-growth segments.

Powergen segment has strong tailwinds from data centers

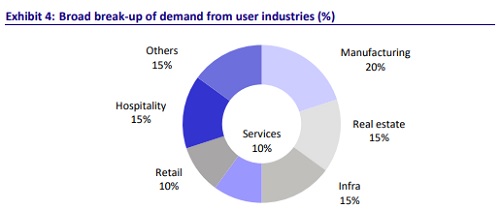

Cummins’ powergen segment has seen broad-based growth across both HHP and non-HHP ranges. Growth in non-HHP nodes was largely driven by volume growth in FY26, and the demand is coming from manufacturing, pharma, quick commerce, luxury residential and commercial real estate. HHP segment growth in the past few years was more dominated by high data center-related revenue. Going ahead, we also expect growth in the HHP segment to be largely driven by data centers (DC) as the overall DC market grows from 1.5GW in FY26 to 8GW by FY30 as per industry estimates. As the demand from both colocation DC as well as hyperscalers grows over the next 4-5 years based on the capacity expansion plans announced by various players (Exhibit 7), we expect KKC to benefit from both HHP product and project revenue. Along with the HHP product revenue, we also expect project revenue to increase for KKC as it gets incremental contracts from data center players. Most of the demand from co-location-based DC is coming for QSK60 nodes, which are fully localized by the company, while QSK78 and QSK95 will remain imported for the next few years till volumes reach an optimum level for any new lines for these nodes. We maintain our estimates and expect powergen revenue to clock 20% CAGR over FY26-28.

Industrial segment growing in select areas

Industrial segment is witnessing growth in mining, marine and railways, while construction and compressor segments may remain weak in the near to medium term. Construction and compressor together formed nearly 48% of industrial segment revenue in FY26. Compressor segment is going through a weak cycle after witnessing strong growth over the last three years. Within construction segment, road construction is weak, while smart city-related projects are growing. We thus expect growth in this segment to be a bit weaker than other segments. We bake in 11% revenue CAGR for industrial segment over FY26-28.

We expect distribution segment growth momentum to continue

Distribution segment has benefited from a large installed base, new product introductions, new geographies, RECD installations and now with the telematics offerings in CPCB 4+ products. With Maharashtra government now too mandating installing RECD devices on older CPCB 2 gensets, KKC stands to benefit from its offerings. The company can also install telematics on CPCB 2 installed base. We expect the pace of growth to continue in the distribution segment as it also stands to benefit from warranty renewals for CPCB 4+ products starting Jul’26 and its data center offerings. We maintain our growth estimates and expect distribution segment revenue to post 22% CAGR over FY26-28.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412