Buy Cummins India Ltd for the Target Rs. 6,600 by Motilal Oswal Financial Services Ltd

Strong performance

Cummins reported a strong performance in 4QFY26 and FY26, mainly led by powergen, distribution and export segments, while the industrial segment remained largely flat YoY in FY26. In the powergen segment, data centre revenue contributed 30-35% in FY26 on strong traction in DC-related products and project revenue. During 4Q too, the company booked strong project revenue from data centers, which historically used to be booked once in a year. We believe that as traction in data center market increases, the company will be able to maintain a strong growth trajectory in both product and project-related revenue from data centers. While we expect powergen and distribution segments to maintain a healthy growth trajectory on strong demand and higher penetration of its products, we do expect near-term pressure on industrial and exports, with dependence being on government capex and various export geographies, respectively. With a healthy revenue mix from highmargin segments and the ability to pass on cost pressure, we expect margin performance to remain strong. We raise our FY27/FY28 estimates by 4%/7% to bake in better powergen revenue and slightly lower industrial revenue. We roll forward our valuation and arrive at a revised TP of INR6,600, based on average of 45x P/E and DCF on Sep’28 estimates, which will capture long-term gains from high-growth segments. Retain BUY.

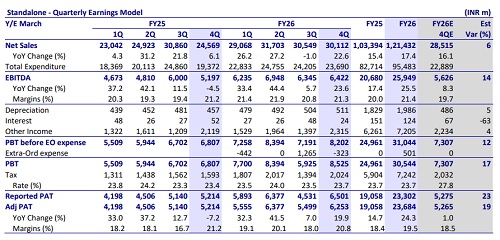

Strong set of results with beat across all metrics

KKC results were ahead of our estimates on revenue, EBITDA and PAT. Revenue increased 23% YoY to INR30.1b (6% above our estimate). Gross margin of 36.0% was 190bp higher than our estimate of 34.1%. This led to absolute EBITDA of INR6.4b (+24% YoY), beating our estimates by 14%, while margin expanded 10bp YoY to 21.3% vs. our estimate of 19.7%. Better-than-expected execution and margins led to adj. PAT of INR6.3b (+20% YoY), beating our estimates by 19%. The company has reversed the impact of labor code change during the quarter by INR323m. Adjusting for that, reported PAT increased 25% YoY to INR6.5b (23% ahead of estimates). For FY26, revenue/EBITDA/PAT grew 16%/26%/24% YoY, while margin expanded 140bp YoY to 21.4%.

Powergen segment to benefit from expanding data center base

Powergen revenue grew by 48%/24% for 4QFY26/FY26, driven by demand growing around mid-teens across non-HHP portfolio and strong demand across HHP portfolio, mainly led by data centre. Data centre formed 35% of total powergen revenue for 4QFY26 (~INR2.5b) and 30-35% for FY26, and this increasing traction across DC market has been visible since 3QFY26 with increasing enquiries from colocation-based data centers and hyperscalers. The nearest competitor to KKC was able to grow its overall powergen revenue by 32% during FY26. Going ahead, we expect demand momentum to remain strong as manufacturing, pharma, quick-commerce, luxury residential and commercial real estate continue to drive demand for non-HHP portfolio. For HHP portfolio, demand continues to be centered around the localized QSK60 platform, which is expected to remain the dominant product over the next two years. The company also expects a gradual transition towards larger QSK78 and

QSK95 platforms as data center capacities scale up, although these engines continue to be imported across the industry. KKC continues to keep investing in capacity upgrades and improving throughput of its existing plants, and it is currently operating at nearly 70% utilization for the company as a whole. We raise our powergen estimates and expect powergen revenue to clock 20% CAGR over FY26- 28.

Industrial segment recovery to be supported by railways and mining

Industrial segment performance remained subdued during 4QFY26/FY26, with revenue growth of +1%/-1% YoY, lower than our estimates. Within this, railways and mining witnessed strong growth, and the outlook is also fairly healthy. However, we expect construction and compressor-related revenue to be little weaker as the underlying industry is witnessing weak activity. We thus revise our growth estimates for industrial segment a bit downward to bake in weakness in these two segments. We expect industrial segment to grow at 11% over FY26-28.

Distribution segment to provide sustainable growth

Distribution segment performance remained strong and revenue grew by 21%/22% for 4QFY26/FY26. Growth continues to be driven by expanding service offerings, predictive maintenance solutions, extended warranty packages, and higher customer engagement across multiple end-markets. Going ahead, we expect growth momentum in distribution segment to be maintained by 1) CPCB4+ products, which will begin exiting warranty coverage from FY27 onward, 2) distribution revenue increasing from its data center-related offerings too as deliveries increase, 3) dual fuel kits and RECD devices, and 4) increased penetration of its products. We maintain our estimates and expect the segment’s revenue to grow at 22% over FY26-28.

Exports may remain lumpy amid geopolitical uncertainty Exports

declined 6% YoY to INR4.5b in 4QFY26 and grew by 12% in FY26. Despite the quarterly softness, FY26 revenue growth was supported primarily by healthy demand from Europe and Asia-Pacific markets. These regions continue to exhibit decent growth, whereas demand from the Middle East and certain other markets remains relatively subdued. The company also indicated that while currency depreciation provides a near-term benefit to export realizations, a portion of these gains is typically passed on to customers over time through pricing negotiations, including transactions with group entities. Growth in exports is expected to remain moderate, with geopolitical uncertainties and global trade disruptions continuing to impact demand visibility. We expect revenue CAGR of 15% over FY26-28 in exports

Margin pressure managed through pricing and localization

The company has started witnessing inflationary pressures in commodity, fuel and logistics costs, along with labor shortages at supplier facilities and freight disruptions arising from ongoing geopolitical issues. While pricing actions are being undertaken to offset these headwinds, there is typically a lag in passing on higher costs for already-booked orders. As a result, these factors could weigh on margins in the near term, although high localization levels and a favorable business mix should help partially mitigate the impact. We factor in margins of 21.5%/22.0% for FY27/FY28.

Valuation and outlook

We raise our FY27/FY28 estimates by 4%/7% to bake in better powergen revenue and slightly lower industrial revenue, and thus expect KKC’s revenue/EBITDA/PAT to clock a CAGR of 18%/20%/21% over FY26-28. The stock is currently trading at 55.2x/45.7x/38.7x on FY27/FY28/FY29 EPS. We roll forward our valuation and arrive at a revised TP of INR6,600, based on average of 45x P/E and DCF on Sep’28 estimates, which will capture long-term gains from high-growth segments. Retain BUY.

Key risks and concerns

Key risks to our recommendation would come from lower-than-expected demand in key segments, higher commodity prices, increased competitive intensity, and lowerthan-expected recovery in exports.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412