Buy Indraprastha Gas Ltd for the Target Rs 220 by Motilal Oswal Financial Services Ltd

1QFY27 margins pressured by higher gas costs

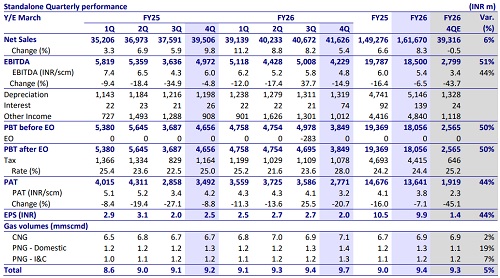

* Indraprastha Gas’ (IGL) 4QFY26 EBITDA/scm came in 44% above our est. at INR4.8. Gas costs and opex increased ~INR1/0.8 per scm QoQ in 4Q. Total volumes were slightly below our estimate at 9.69mmscmd, rising 6% YoY. Resulting EBITDA beat our estimate by 51% at INR4.2b (-15% YoY). IGL’s PAT beat our est. by 44% at INR2.8b (-21% YoY).

* Key things we liked about the result:

1) Total 4Q volumes were slightly above our estimate at 9.7mmscmd (our est.: 9.3mmscmd), rising 5.6% YoY. CNG volumes grew 5.5% YoY.

2) Management has guided for a robust 10.6mmscmd exit volume for FY27, driven by 10-13% YoY growth in CNG volumes, and EBITDA margins at INR7-8/scm.

3) The National PNG drive 2.0 is expected to support natural gas adoption. IGL has connected a total of 3.44m D-PNG customers, of which 2.45m are currently billed. Under PNG Drive 2.0, the company is targeting 0.35m new billed domestic connections in FY27 (vs. 0.23-0.25m earlier), supported by a strong pipeline of ~0.5m already-connected but non-consuming customers that offer a low-cost, near-term conversion opportunity with minimal incremental infrastructure requirement.

* Key investor concerns:

1) Management indicated that gas procurement costs have increased ~25% from pre-geopolitical crisis levels (3QFY26 gas cost: INR35.8/scm). However, it has taken an INR3/kg CNG price hike, which is likely to provide margin support.

2) Supply to I&C customers has been cut by 20%, leading to soft I&C-PNG volumes in 4Q. Volumes are expected to remain weak in 1QFY27.

3) Delhi volumes growth is still lagging, with only 1% YoY growth in 4Q. Additionally, while only 25 DTC buses are left, there are 1,790 DIMTS CNG buses with 0.13m kg consumption per day.

* Valuation: We value IGL at 15x Dec’27E SA P/E and add INR43/sh as the value of JVs to arrive at our TP of INR220/sh. At 2% FY27E dividend yield and 18% EPS CAGR over FY26-28, we believe the valuation is attractive. Reiterate BUY.

Higher-than-estimated EBITDA/scm margin drives beat

* Total volumes were slightly above our estimate at 9.7mmscmd (our est.: 9.3mmscmd), rising 5.6% YoY.

* CNG volumes came in line with our estimate, while D-PNG/I&C PNG volumes stood 19%/7% above est.

* EBITDA/scm beat our estimate by 44% at INR4.8 (est.: INR3.4/scm).

* Realization increased ~INR0.8/scm QoQ and gas costs/opex increased ~INR1/0.8 per scm QoQ.

* EBITDA was 51% above our estimate at INR4.2b (-15% YoY).

* IGL’s PAT was 44% above our est. at INR2.8b (-21% YoY).

* Interest expense stood above estimate.

* The Board has recommended a final dividend of INR1.5/sh (FV: INR2/sh).

Valuation and view

* IGL currently trades at 18.3x one-year forward P/E, at par with its mean – 1 S.D. P/E. We estimate EBITDA margin of INR4.3/INR6.5 per scm in FY27/28 and volumes to clock 8% CAGR over FY26-28. Resultant EBITDA and PAT are estimated to clock a CAGR of 18% each over FY26-28.

* We value IGL at 15x Dec’27E SA P/E and add INR43/sh as the value of JVs to arrive at our TP of INR220/sh. At 2% FY27E dividend yield and 18% EPS growth over FY26-28, we believe the valuation is attractive. Reiterate BUY

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412