Add Lumax Industries Ltd for the Target Rs. 7,100 by Choice Institutional Equities

Robust order book & rising LED penetration to drive growth: LUMX has bagged contracts worth INR 22,000 Mn (~53% of FY26 revenue), wherein PV contributed 66% and LED-based products accounted for 88% of the total order book. In Q4FY26, the company secured key lighting programs from Mahindra (XUV 7XO), Toyota (Urban Cruiser), Skoda (Kushaq Facelift) and Royal Enfield. LED lighting contributed 61% to FY26 revenue as compared to 58% in FY25, reflecting accelerating premiumisation across vehicle segments. We expect LED contribution to continue increasing in the medium term, supported by a higher adoption of advanced lighting technologies such as ADB, multipixel LEDs and animated lighting solutions.

Bengaluru facility to support growth visibility: LUMX is accelerating capacity expansion through its upcoming Bengaluru facility, which is expected to commence operations by Q4FY27E. The plant is being established to cater primarily to newly secured programs from Maruti Suzuki and Toyota, thus strengthening the company’s presence in the southern automotive hub. Additionally, Phase II of the Chakan facility has already commenced operations, enhancing execution capability for the growing order pipeline.

Margin expansion driven by product mix & localisation: LUMX delivered EBITDA margin of 10.3% in Q4FY26 and guided for 10.5–11.0% margin in FY27E. The expansion was supported by operating leverage, richer LED mix and localisation initiatives. The company has already reduced import dependence to 25–30% and continues to localise critical LED components. We expect profitability to improve further, supported by scale benefits, localisation gains and increasing contribution from premium lighting solutions.

View and Valuation: We largely maintain our FY27/28E EPS estimate, valuing the company at 22x (maintained) on FY28E EPS and maintain our target price of INR 7,100. Accordingly, we upgrade our rating from ‘ADD’ to ‘BUY’, supported by the recent correction in the stock price, strong revenue visibility from order book, accelerating LED penetration and upcoming Bengaluru capacity commissioning

Q4FY26 beats our estimate across the board

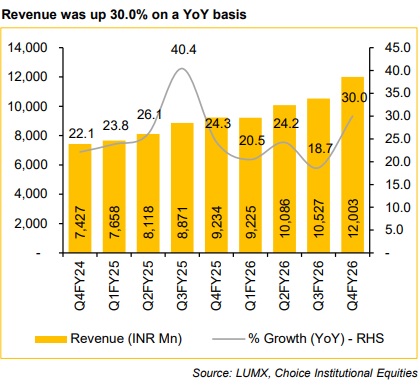

* Revenue was up 30.0% YoY and up 14.0% QoQ to INR 12,003 Mn (vs CIE estimate of INR 10,776 Mn)

* EBITDA was up 56.3% YoY and up 12.1% QoQ to INR 1,240 Mn (vs CIE estimate of INR 1,088 Mn). EBITDA margin was up 174 bps YoY and down 18 bps QoQ to 10.3% (vs CIE estimate of 10.1%)

* APAT was up 27.5% YoY and down 10.1% QoQ to INR 561 Mn (vs CIE estimate of INR 534 Mn)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131