Buy Ather Energy Ltd for the Target Rs.1,000 by Emkay Global Financial Services Ltd

We met Ather’s management—Tarun Mehta, Co-founder and CEO, and Sohil Parekh, CFO—to discuss E-2W demand trends and Ather’s growth outlook and strategy wrt its EL platform. KTAs: 1) Domestic E-2W industry seeing strong growth momentum (20-30% YoY during Dec ’25-Feb ’26), led by the >Rs0.1mn segment and the Rs0.1mn market volume showing signs of bottoming; stepup in ICE-2Ws has not slowed the E-2W industry. 2) EL platform (traditional design; targets the Rs0.1-0.13mn segment, which is the belly of the market with 50% share) to meaningfully expand Ather's TAM, margins (huge mechanical cost savings while retaining quality/software), and market share (especially in non-South markets); cannibalization is welcome, given EL’s superior cost structure/margin. 3) AURIC (42k units/mth capacity) to be fully operational before FY27-end; margin benefits to accrue in ensuing quarters; high-volume variants to be launched once plant stabilizes. 4) E-2W industry could see price hike from Apr-25 (Rs5k/unit), on PM E-Drive scheme expiry in Mar-26; ongoing geopolitical tension may cause a temporary 300-400bps hit; OEMs may raise price/absorb impact (based on longevity). We expect strong volume ramp-up at Ather (led by EL) and believe it can achieve EBITDA/PAT breakeven in H2FY27. We retain BUY/TP of Rs1,000, at 7x EV/S (like EIM’s implied valuation of 7.5x EV/S for RE over the 2013-17 high-growth phase; 10x peak valuation).

E-2W industry momentum stays strong; policy, commodity risks to be watched The domestic E-2W industry is seeing strong momentum (20-30% YoY over Dec ’25-Feb ’26), led by the Rs0.1mn segment (35% CAGR, per the mgmt) and the Rs0.1mn category showing signs of bottoming out. Notably, acceleration in ICE-2W sales has not come at the cost of E-2W adoption. The E-2W industry could see a price hike (Rs5k/unit) from Apr-25 due to expiry of PM E-Drive scheme in Mar-26. Ongoing geopolitical tensions may drive temporary commodity cost volatility (~300-400bps impact), with OEMs either raising prices or absorbing the impact (depending on the longevity of the impact).

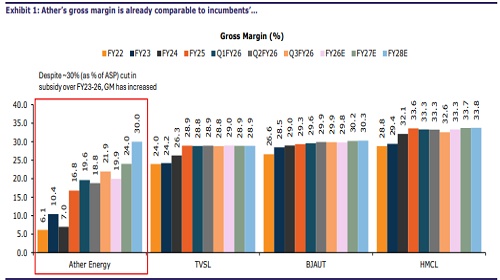

EL platform ramp up via AURIC to power volume/margin, drive share gains EL platform (traditional design; multiple price-points; targets the Rs0.1-0.13mn range— belly of the market; 50% share) to significantly expand Ather's TAM, margin (significant savings in mechanical cost while sustaining quality/software), market share (especially in non-South markets, potentially driving 70-80% volume growth); cannibalization is welcome, given EL’s superior cost structure/margin. ‘Consideration’ for brand Ather greatly rose with Rizta launch; EL platform expected to help convert ‘consideration’ into ‘customer preference’. AURIC to be fully operational before FY27-end; margin benefit to accrue in ensuing quarters; high volume variants to be launched on stabilization.

3-pronged strategy to counter risk; marketing pivoting toward mass premium The mgmt highlighted its 3-pronged strategy for countering macro headwinds/volatility – i) Technology hedge via mix of LFP/NMC/NCA chemistries to optimize cost, supply flexibility, performance. ii) Supplier hedge to reduce single vendor dependency. iii) Geographic hedge via diverse sourcing (LFP/NCA/NMC from China/Malaysia-Japan/Korea to mitigate regional risks). Also, Ather’s marketing focus is increasingly shifting toward the mass-premium (>Rs0.1mn) segment due to the upcoming EL platform.

Other key takeaways from the management meeting

Ather’s pricing power

* Industry discounting has moderated from the CY25 peak; Ather’s discounts (1–1.5% in specific markets) are lower than the industry’s 8-12%.

* Ather has demonstrated relatively strong pricing power over the last 1-1.5 years, aided by healthy demand elasticity and financing penetration (60% of its volume).

* States such as UP, Bihar, Jharkhand, and Gujarat are more impacted by price hikes.

Cost reduction in the EL platform

* Mechanical simplification (eg belt drive, drum brakes, steel chassis vs aluminum) significantly reduces material costs, making the cost delta vs Rizta larger than that of Rizta vs 450.

* Positioned to compete with Honda Activa and Hero Destini 125 in the high-volume, midprice segment.

* EL is expected to be priced at ~20% premium to the broader market.

Ather stack; software ecosystem emerging as a key moat

* Customers are opting for the Ather stack, with willingness to pay Rs15k premium.

* Ather Stack adoption stands at ~91%, significantly higher than the low 10–15% for competitors, with several features show strong daily usage (eg Auto Hold, Cruise Control, etc).

* The company is positioning software as a key differentiation lever, supported by a new marketing narrative (“Life is easy on an Ather”).

Product and feature innovation to strengthen user experience

* 70% of software features can be delivered via OTA updates, improving the long-term product value.

* Customers show preference for one-time upfront software payments vs recurring subscription models.

Brand strength and conversion metrics improving

* The extent of brand awareness and ‘consideration’ have risen sharply after the launch of Rizta.

* Test ride to purchase conversion exceeds 60%, while store walk-in conversion stands at ~35–40%.

* Marketing focus is shifting toward the mass-premium segment (>Rs0.1mn).

Distribution expansion

* Dealer expansion will largely occur via existing partners who drove 70–80% of store additions previously, from 350 to 700 stores.

* Of the top-50 dealers in FADA, half are already a partner with Ather.

Competitive landscape

* The >Rs0.1mn segment is likely to remain highly competitive and discount-heavy, especially with legacy OEM participation.

* Entry of Japanese OEMs could accelerate overall EV penetration, given their strong share in the ICE 2W market

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354