Accumulate Federal Bank Ltd For Target Rs.300 by Prabhudas Liladhar Capital Ltd

.jpg)

RoA delta to be driven by asset/liability mix

Quick Pointers

* Core PPoP beat of 9.5% due to better fees & TWO recovery

* CASA momentum continues; ratio is up 270bps YoY to ~33%

* PCR shored up to ~88%; downside risks to provisions

FB saw a decent quarter as core PPoP beat PLe by 9.5% due to better fees and TWO recovery. Interest on IT refund of INR 4.6bn was used to shore up PCR QoQ from 76% to 87.8% against likely ECL requirement; credit cost guidance of 50-60bps would be reassessed. We are factoring provisions of 48bps, but there are downside risks. While loan growth was a tad lower; recalibration is progressing well with targeted segments of CoB, gold, unsecured and LAP seeing good growth. Liability mix too is being refined with higher share of CASA/RTD. We tweak multiple on Mar’28 ABV to 1.5x from 1.4x and raise TP to INR 300 from INR 275. Change rating to ‘ACCUMULATE’ from ‘BUY’.

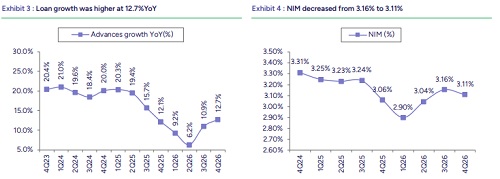

Decent quarter; core PPoP beat due to higher fees/lower opex: NII was in-line at INR 27.2bn with NIM meeting expectations at 3.11%; reported NIM was up 2bps QoQ to 3.20%. Loan growth was a miss at 12.7% YoY (PLe 14%). Deposit accretion was largely in-line at 10.7% YoY (Ple 11%). LDR decreased to 84.3% (85.8% QoQ). CASA ratio increased to 32.9% (32.1% in Q3’26). Other income came in at INR 11.45bn (PLe INR 11.1bn); fees and TWO recovery were higher. Opex at INR 20.4bn was 1.9% below PLe led by lower staff cost partly offset by higher other opex. Core PPoP at INR 18.1bn was 9.5% above PLe; PPoP was INR 22.7bn. Asset quality was steady; GNPA was 1.6% (PLe 1.6%) as net slippages were in-line. Provisions were higher. Core PAT was 14% above PLe at INR 11.35bn; PAT was INR 12.6bn.

Loan portfolio recalibration and CASA momentum continues: Credit growth was lower at 3.5% QoQ (PLe 4.8%) due to corporate (0.4%) and BuB (-0.9%). However, the bank continues on its path of re-calibration; there was healthy QoQ offtake in CoB (5.9%), LAP (7.7%) gold (9.0%), CV/CE (8.5%) and unsecured (PL+CC+MFI) growth has picked up to 4.2% (2.5% in Q3’26). Deposit growth was lower than system due to fall in wholesale deposits; however, RTD and CASA accretion has been higher. Bank continues to restructure its deposit profile, focusing on quality over quantum, with CASA and RTD becoming core drivers of liability growth.

IT refund allows increasing PCR: Provisions jumped QoQ to INR 7.4bn (PLe INR 3.1bn) as interest on IT refund of INR 4.6bn was used to shore up PCR to 87.8% from 76%. Management suggested that this has been partly done against likely requirement of ECL, and credit cost guidance of 50-60bps would be reassessed. We trim provisions for FY27/28E by 2bps each to 48bps.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271