Buy Samvardhana Motherson Ltd for the Target Rs 160 by Motilal Oswal Financial Services Ltd

Strong performance amid a tough macro environment Emerging business segment set to scale up rapidly from here on

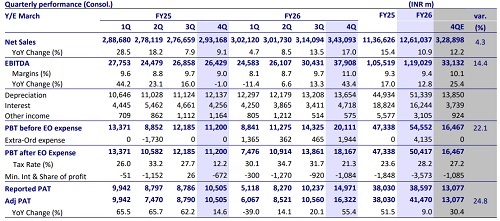

* Samvardhana Motherson’s (SAMIL) 4QFY26 adjusted PAT at INR16.3b was above our estimate of INR13b, up 55% YoY. EBITDA margin grew 200bp YoY to 11% and ahead of our estimate of 10.1%. Margin beat was driven by Emerging business (+240bp YoY to 14.5%), and Integrated Assemblies (+500bp YoY to 15.6%).

* Given the better-than-expected performance in 4Q, we raise our earnings estimates by 8% each for FY27/FY28. Management alluded to its next fiveyear revenue growth aspiration, which now stands at a staggering USD108b. We expect SAMIL to continue to outperform global automobile sales, fueled by rising premiumization and EV transition, a robust order backlog in autos and non-autos, and successful integration of recent acquisitions. Given the long-term growth opportunities, we reiterate our BUY rating on the stock with a revised TP of INR160, based on 24x FY28E EPS.

Strong operating performance

* Consolidated revenue grew 17% YoY to INR343b (in line with our estimate of INR328b), aided by organic growth, favorable forex rates, and integration of Atsumitec.

* EBITDA margin expanded 200bp YoY and 130bp QoQ to 11%, above our estimate of 10.1%. This was led by a better-than-expected performance in wiring harness, integrated assembly, and emerging business segments.

* Wiring harness revenues grew 19% YoY to INR102b (7.5% above est) and managed to expand margins by ~170bp QoQ to 11.4% vs est of 10.9%, despite 16% QoQ rise in copper prices.

* Integrated assemblies’ revenue grew 20% YoY to INR28.7b (16% above est.), and margin improved 500bp YoY to 15.6% vs. our est. of 12.8%, fueled by strong operating leverage, continued execution of the existing order book, and cost control measures.

* Emerging business revenues grew 60% YoY to INR51.5b (11% above est.), and margins also expanded 240bp YoY to 14.5% vs. our est. of 9.7% due to better performance from Lighting & Electronics and Aerospace businesses.

* Vision systems was the only laggard, with revenue 4% below and margin 70bp below our estimate at 11.2%.

* Overall, EBITDA grew 43% YoY to INR37.9b, ahead of our est. of INR33.1b.

* The company incurred an extraordinary expense of INR2b in respect of phased operational restructuring at certain units primarily located in Europe. Adjusted for this expense, PAT beat our estimates, growing 55% YoY to INR16.3b (ahead of our estimate of INR13b).

* FY26 performance: Revenue/EBITDA/PAT grew 11%/13%/9% to INR1.2t/ INR119b/INR41.5b. The OCF/FCF stood at INR113b/INR54b.

Valuation and view

Given the better-than-expected performance in 4Q despite adverse global macro, we raise our earnings estimates by 8% each for FY27/FY28. Management has alluded to its next five-year revenue growth aspiration, which now stands at a staggering USD108b. We expect SAMIL to continue to outperform global automobile sales, fueled by rising premiumization and EV transition, a robust order backlog in autos and non-autos, and successful integration of recent acquisitions. Further, the current adverse global macro is likely to lead to industry consolidation, with players like SAMIL likely to emerge as key beneficiaries in the long run. Given the long-term growth opportunities, we reiterate our BUY rating on the stock with a revised TP of INR160, based on 24x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412