Buy Canara HSBC Life Insurance Ltd for the Target Rs. 180 by Motilal Oswal Financial Services Ltd

Consistent outperformer with improving profitability

* We had initiated coverage on Canara HSBC Life Insurance (CANHLIFE) in Jan’26 as a multi-year compounding story, consistently outperforming industry growth over the past few years with an alpha of 700-800bp, resulting in a private market share of 2.6% in FY26 (vs. 2.2% in FY22).

* While near-term growth has moderated (Apr’26 APE growth of 11% YoY vs. 38% YoY growth for the industry) amid product mix recalibration and implementation of revised underwriting processes, we expect the insurer to maintain a 20% APE growth trajectory.

* The insurer benefits from the strong operational integration within the Canara Bank ecosystem (72% of APE in FY26) with multiple initiatives underway to improve the branch activation (54% in FY26) and harness the underpenetrated opportunity (<2% penetration within Canara Bank’s ~85m customer base). Further, the exclusive relationship with the expanding HSBC network (14% of FY26 APE) and the gradual expansion of the agency provide a strong growth lever.

* The aggressive shift towards traditional products, robust operational efficiency, and rising rider attachments have led to a 320bp YoY expansion in FY26 VNB margin (to 22.4%), despite GST-related headwinds and investments toward agency scale-up. We expect the VNB margin to improve 10bp/50bp in FY27/ FY28, reaching 23% in FY28 with the impact from rising traditional contribution apart from agency channel scale-up.

* Given relatively disciplined payout structures (commission ratio of 6.4% in FY26 – second lowest in the industry) and strong operational positioning within banca ecosystems, the possible commission regulations could potentially improve competitive positioning and partnership accessibility over time rather than structurally impairing the franchise.

* With one of the most underpenetrated PSU-bank funnels and clear visibility on branch activation, product mix upgrades, and operating leverage, we expect the company to deliver high-teens operating RoEV going ahead despite near-term ITC and agency drag. We estimate a CAGR of 20%/22% in APE/VNB. Maintain BUY with a one-year TP of INR180 (based on 1.7x FY28E P/EV).

Poised for an industry-leading growth momentum

* CANHLIFE has grown better than the industry with an FY22-26 APE CAGR of 16% compared to 11% for the industry, resulting in market share gain from 2.4% in FY22 to 2.6% in FY26 among private players. Individual APE continues to outperform the industry with a five-year CAGR of 20%.

* The GST exemption (implemented from 22 Sep’25) further boosted the growth momentum for the insurer with total APE growth of ~26% for 2HFY26 compared to industry growth of ~20%.

* However, the insurer experienced a slowdown in momentum in Mar’26/ Apr’26, with APE declining 4% YoY/rising 11% YoY vs. the industry growth of 20%/38%. The slowdown was largely because of a strategic transition towards traditional products over ULIPs, as the focus has increased on balancing growth with long-term sustainability, predictability, and quality of earnings.

* Additionally, CANHLIFE implemented underwriting-related operational guidelines required by IRDAI from Apr’26, which possibly led to temporary policy issuance delays and business deferral.

* With customer preference robust for linked products through most of FY26, the focus on non-par, protection, and annuity products impacted near-term growth for the company. We expect the moderation to subside and APE to grow at a FY26-28 CAGR of 20%, likely outperforming the industry by 400-500bp.

Playing on channel diversification and existing bancassurance strength

* CANHLIFE’s distribution architecture remains one of the most important pillars supporting the company’s long-term growth outlook. The insurer continues to increase penetration in existing channels and expand business opportunities through new distribution avenues.

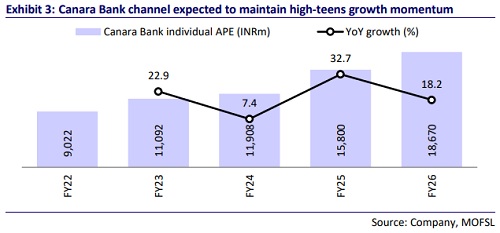

* Canara Bank channel (72% of FY26 individual APE) serves as a distribution backbone with 9,800 branches, an addressable customer base of 80m, and a current penetration level of <2%, reflecting notable headroom for growth. Branch activation (defined as ≥10 policies sold with ~INR50,000 ticket size) stands at ~54% in FY26, improving from ~50% last year.

* The Canara Bank channel functions through extensive integration of the insurer from field sales to branch to zone levels, ensuring continuity despite any changes in bank senior management. While bancassurance concentrationremains a risk, this showcases the depth and resilience of the relationship with the bank.

* A dedicated team has been set up to implement productivity improvement programs in most of the 9,800+ branches of Canara Bank, with a focus on increasing branch activation as well as deepening presence in Tier-3 cities. The insurer is also making progress on lead-based sales by activating the call centers. Growth in branch activation, along with an increase in productivity, can lead to sustained growth momentum for the Canara Bank channel at 17-18%.

* Despite LIC’s presence within the Canara Bank ecosystem, CANHLIFE aims to sustain and gradually expand its market share within the bank. Private insurers are unlikely to scale within PSU-bank ecosystems in the near term, and CANHLIFE’s long-standing operational integration with Canara Bank remains a key competitive advantage.

* Alongside the core banca franchise, an exclusive partnership with the HSBC channel (14% of FY26 individual APE) continues to deliver strong momentum, providing the insurer with access to affluent retail and NRI customers with needs of wealth-linked insurance, protection plans, and global mobility products.

* HSBC is expanding its network from its existing 26 branches to 40 potential branches, with eight new branches already opened. Apart from branch network expansion, the bank is also going aggressive on non-prime customers, initiating loans, credit cards, and private banking, which would help CANHLIFE to provide diversified offerings in this channel as well.

* The channel operates with a ULIP:traditional mix of 65:35 with higher sales of annuity and lower ULIP costs, resulting in better profitability compared to the Canara bank channel. Network expansion and new products like credit life, etc., will further provide a boost to margins in this channel.

* Activation of the additional HSBC branches, growing traction within affluent and UHNI segments, increasing mortgage-linked credit life opportunities, and the GIFT City initiative are expected to support future growth within the channel.

* Other banks (6% of FY26 individual APE) serve as a deeper penetration engine, with six regional rural banks enabling direct access to rural customers through 4,600+ branches. The focus through this channel is on first-time insurance buyers with the opportunity of bundled offerings and assisted sales.

* The recently launched agency business represents another important strategic initiative with 500 distributors onboarded and APE of INR140m during Oct’25 to Mar’26. The hybrid agency model has been adopted by CANHLIFE, similar to prevalent models in the industry.

* The company targets an agency contribution of ~5% over the next three years through a Tier-1-led branch strategy utilizing the existing infrastructure. For new locations, phase-wise deployment is planned with hiring ongoing at various levels to scale the channel.

* The agency channel’s growth trajectory is expected to be significant, owing to a low base, which insulates the company’s target growth of 18-20%. On the profitability front, the contribution of traditional as well as rider attachment in ULIPs is expected to be higher, resulting in better margins.

* Apart from the agency channel, CANHLIFE is also operating through other alternate channels like direct, brokers, etc. (8% of FY26 individual APE). The insurer is one of the premier partners for the PolicyBazaar platform.

* Overall, while bancassurance continues to remain the dominant channel, CANHLIFE appears to be gradually building a more diversified and scalable distribution franchise. The combination of deep banca integration, improving branch productivity, rising alternate channel contribution, agency buildout, and accelerating HSBC momentum could progressively improve both growth visibility and franchise resilience over time.

Product mix rebalancing taking VNB margin near the industry average

* CANHLIFE’s product mix appears to be transitioning towards a more balanced and predictable business model, with ULIP contribution declining from 54% in FY25 to 51% in FY26 and protection share rising from 4% in FY25 to 7% in FY26.

* However, on a quarterly basis, product mix has been quite volatile, with the share of traditional products reaching 80% in 4QFY26 compared to 27% in 3QFY26. While traditional products are currently being pushed aggressively, which may moderate top-line growth, the focus is to move towards a balanced product mix over the next 2-3 years, improving business quality and reducing volatility.

* The insurer recently launched new products in the par and non-par segments, which supported the rise in contribution from traditional products in 4QFY26. Within annuities, management remains focused on deferred annuity products, which offer superior long-term customer value, better persistency, and stronger earnings visibility.

* Protection continues to emerge as another important growth lever with healthy traction across both retail protection and group credit life products. The company is also witnessing improved rider attachment across ULIP products, which has helped support profitability even during periods of elevated linked product contribution.

* The product mix shift served as one of the key drivers for 330bp VNB margin expansion, with FY26 VNB margin at 22.4% despite the adverse impact from

GST-related changes and ongoing investments toward scaling newer distribution channels.

* On the cost front, CANHLIFE has accelerated investments in enhancing AI capabilities, which are expected to improve operational efficiency going forward. Digitization across the franchise has continued to improve meaningfully, with almost all new business sourcing now digital.

* Going forward, the margin is expected to benefit from 1) continued aggression towards traditional products, 2) better rider attachment, 3) launch of credit life/credit card-linked insurance in the HSBC channel, 4) term+ULIP product in the agency channel, and 5) continued operating leverage. However, this will be hit by agency ramp-up strain as well as the higher impact of GST exemption as the contribution of traditional products rises. We expect the VNB margin to be largely stable at 22.5% in FY27 and then improve to 23% in FY28, resulting in an FY26-28 VNB CAGR of 22%, which is better than our expected APE CAGR of 20%.

Maintaining high-teens operating RoEV

* CANHLIFE’s EV sensitivity has improved significantly recently owing to the expansion in hedging capacity. After the launch of non-par business in 2018, sensitivity was higher due to lower capacity of hedging, though the business has grown over the years, contributing 19% of APE in FY26.

* Generally, EV of life insurers is inversely related to the change in the reference rate. However, the high share of ULIP (~51% in FY26) for CANHLIFE has resulted in a positive relation with a change in the reference rate for the insurer.

* With better hedging and strong headroom for improvement in VNB margin, we expect the insurer to maintain operating RoEV in the range of 18-19%.

Regulatory picture – commission changes and IFRS

* Recent investor concerns around potential commission-related regulatory changes have emerged as one of the key overhangs across the life insurance sector, particularly for bancassurance-led players.

* For CANHLIFE, existing commission structures are already relatively disciplined compared with certain industry peers, with a commission rate of 6-7% of gross premium (second only to SBILIFE). As a result, even under scenarios involving tighter commission regulations or partial rollbacks toward earlier payout structures, the impact should not be material.

* Tighter industry-wide commission structures could also improve accessibility to certain partnerships that may currently remain uneconomical due to irrational pricing by competitors. Hence, while the downside of potential commission regulations is limited, there is a possibility of medium-term strategic upside from the same.

* Transition toward IFRS 17 remains a complex exercise for both companies and investors. CANHLIFE has sought a one-year forbearance period for implementation and expects parallel reporting structures initially during the transition phase.

* Investor education around IFRS interpretation could become increasingly important as reporting frameworks shift from traditional premium-based metrics toward contribution-oriented profitability measures. While the transition could initially increase modeling complexity and reduce comparability across the sector, greater disclosure sophistication may improve transparency over time.

Valuation and view

* CANHLIFE offers a rare multi-year compounding opportunity anchored in a structurally improving banca engine, rising contributions from premiumized HSBC flows, and disciplined agency expansion.

* CANHLIFE enters its listed journey at a point where both its distribution architecture and financial model are undergoing structural strengthening. The recent exemption of GST from life insurance has given a boost to the growth trajectory of the insurer. The differentiated dual-bank partnership with mass scale from Canara Bank and premium affluence from HSBC creates a distribution backbone that only a few private life insurers possess.

* The launch of the agency channel, while margin-dilutive in the near term, adds distribution resilience and long-term optionality.

* With one of the most underpenetrated PSU-bank funnels and clear visibility on branch activation, product mix upgrades, and operating leverage, we expect the company to deliver high-teens operating RoEV going ahead despite near-term ITC and agency drag. We estimate a CAGR of 20%/22% in APE/VNB. Reiterate BUY with a one-year TP of INR180 (based on 1.7x FY28E P/EV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

Life Insurance Sector Update : New business in Jul-26 - Slowdown in growth momentum by Emkay...