Neutral BPCL Ltd for the Target Rs 265 by Motilal Oswal Financial Services Ltd

Weak near-term earnings outlook; capex intensity rising

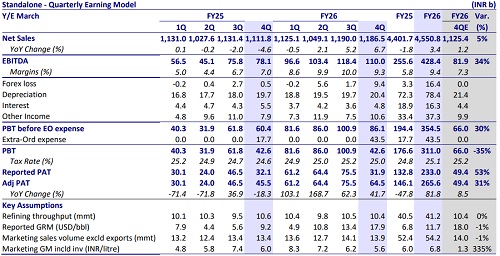

* Strong 4Q performance driven by marketing: BPCL's reported GRM came in line with our est. at ~USD17.9/bbl (our est. USD18/bbl) in 4QFY26. Marketing margin (including inv.) stood at INR5.6/lit (est.: INR1.3/lit). Both refining throughput/marketing volumes came in line with our estimates at 10.4mmt/ 13.9mmt. Consequently, standalone EBITDA/APAT came in 34%/31% above our estimate at INR110.0b/INR64.5b. Clean PAT, adjusted for forex loss, marketing inventory gain and impairment loss, stood 25% above our est. at INR62b.

* Key things we liked about the result:

1) BPCL posted a strong marketing performance, fueled by inventory gains (INR0.8/lit), with a blended gross marketing margin of INR5.6/lit (est. INR1.3/lit).

2) BPCL aims to achieve 6.5- 7mmtpa of crude production capacity (group level). INR22.5b equity shall be infused in Bharat PetroResources (BPRL) in FY27.

3) The company continues to diversify its crude basket, with Russian crude share rising to 31% in 4QFY26 from 25% in 3QFY26 (current: 40%-45%). Crude supply till Jul’26 has already been secured.

* Key monitorables:

1) Domestic LPG losses have widened sharply recently to ~INR670/cylinder in May’26 (vs. ~INR170/cylinder in Apr’26 and ~INR80+/cylinder in 4QFY26).

2) After the INR4/lit petrol/diesel retail price hike, gross auto-fuel marketing losses are still in the range of INR10-20/lit. We see the possibility of another INR2-3/lit MS/HSD retail price hike if the situation continues.

3) With OMCs making huge marketing losses, we believe that some form of government compensation/support is possible.

4) Bina petrochemical and refinery expansion project has achieved 23% progress vs. 32% planned. Delays are primarily due to geopolitical developments and supply-chain disruptions.

* Key assumption: In FY27, we model consol. EBITDA/APAT of INR103b/INR98b (declining 71%/62% YoY), as we assume:

1) gross MS and HSD marketing margin losses of INR5/INR2.5 per lit in 1QFY27/2QFY27 (normalizing to INR4.5/lit in 2HFY27-FY28).

2) LPG under-recovery per cylinder of INR200/100 in 1QFY27/2QFY27.

3) GRM of USD15/14 per bbl in 1QFY27/2QFY27 (normalizing to USD7-8/bbl in 2HFY27-FY28).

* Valuation : BPCL currently trades at 1.2x 1yr. fwd. P/B vs. 10-year average of 1.8x. We reiterate our Neutral rating with an SoTP-based valuation of INR265/share.

Valuation and view

* BPCL’s GRMs have been at a premium to SG GRMs because of the continuous optimization of refinery production, product distribution, and crude procurement. The use of advanced processing capabilities of Bina and Kochi refineries allows BPCL to process 100% of high-sulfur crude and 50% of Russian crude.

* While valuation appears reasonable, weak near-term marketing outlook and the commencement of a new capex cycle emerge as key concerns.

* BPCL currently trades at 1.3x 1yr. fwd. P/B vs. 10-year average of 1.8x. We reiterate our Neutral rating with an SoTP-based valuation of INR265/share

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

600-400.jpg)