Buy Astra Ltd for the Target Rs 1,950 by Motilal Oswal Financial Services Ltd

Robust volume growth drives performance Operating performance below our estimate

* Astral Ltd (ASTRA) reported a strong quarter with volume growth of ~24% YoY (among the highest in the industry) to 84k MT, with EBITDA growth of 27% YoY. This was led by the plumbing business with EBITDA growth of 41% YoY, while the Adhesives business dipped 20% due to raw material price pressure.

* The company highlighted its growth strategy during the analyst meet, focusing on key revenue drivers such as the CPVC resin plant for backward integration, new product launches, a higher share of value-added products, scaling up the bathware business, and decentralization of plants to improve efficiency. The company remains focused on gaining market share and driving volume growth, while backward integration and an improved product mix are expected to support margin expansion.

* We raise our FY27/FY28 EBITDA estimates by 5% each to factor in volumeled better operating leverage, raw material pricing stability, and improved product mix. Reiterate BUY with an SoTP-based TP of INR1,950.

Margins remained resilient despite volatile PVC prices

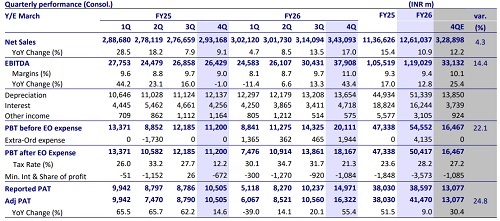

* Consolidated revenue was up 24%/35% YoY/QoQ at INR20.9b in 4Q (est. INR23.8b). EBITDA grew 27% YoY/67% QoQ to INR3.8b (est. INR4.6b). EBITDA margin expanded 40bp YoY/300bp QoQ to 18.3% (est. 19.2%), led by a 150bp YoY increase in gross margin. Adj. PAT grew 21% YoY/ 81% QoQ to INR2.2b (est. INR2.9b).

* Plumbing business revenue stood at INR15.3b (+25% YoY, +43% QoQ), EBIT was INR2.9b (+46% YoY, +2.1x QoQ), and EBIT margin came in at 19.1% (+280bp, +610bp QoQ). Volume grew 24%/36% YoY/QoQ to 84kMT, while EBIT/kg grew 18%/55% YoY/QoQ at INR34.8.

* Paint and adhesive business revenue stood at INR5.5b (+22% YoY, +18% QoQ), EBIT stood at INR228m (-45% YoY, -23% QoQ), and EBIT margin was 4.1% (-500bp, -220bp QoQ).

* In FY26, volume/revenue/EBITDA/Adj. PAT grew 16%/13%/12%/6% YoY to 263kMT/ INR65.7b/INR10.6b/INR5.5b.

* Gross debt stood at INR1.5b as of FY26 vs. INR1.4b in FY25. CFO grew 77% to INR11.2b in FY26, with a CFO/EBITDA ratio of 105%

Valuation and view

* ASTRA continues to strengthen its industry leadership through innovation, backward integration (CPVC resin), and capacity decentralization. Its investments in CPVC and new product categories underscore a long-term vision to reduce dependence on imports and enhance value addition. With consistent double-digit growth guidance (volume 10-15% with value to growth at a higher rate) and robust execution history, ASTRA remains one of the most agile players in India’s plastic pipes industry.

* We expect ASTRA to deliver a CAGR of 18%/25%/37% in revenue/EBITDA/PAT over FY26-28. We reiterate our BUY rating on the stock with an SoTP-based TP of INR1,950 (premised on 50x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412