Buy Dalmia Bharat Ltd For Target Rs. 2,230 Motilal Oswal Financial services Ltd

Muted volume growth; lower opex/t drive profitability

Near-term cost pressure; targeting above-industry growth in FY27

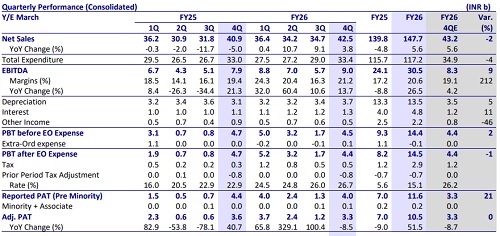

* Dalmia Bharat’s (DALBHARA) 4QFY26 EBITDA grew ~14% YoY to INR9.0b (9% beat), driven by lower-than-expected opex/t. EBITDA/t increased ~11% YoY to INR1,025 (est. INR928). OPM surged 1.9pp YoY to ~21% (+2.1pp vs. our estimate). Adjusted PAT was down ~9% YoY at INR3.3b (in line).

* Management highlighted that operating cost environment turned adverse due to the ongoing West Asia conflict. It is witnessing broad-based inflation across power & fuel, packaging, and logistics. Packaging costs have increased due to tight bag availability and higher granule prices, while fuel costs remain on an upward trend (rising sharply to ~USD160/t). Though it is implementing internal cost-control measures to cushion the impact. Further, price hikes have been taken in Apr’26 to partially offset the impact. It is adding capacity across West and South regions to reach 61.5mtpa by Dec’27 vs. 49.5mtpa currently. It is aiming to deliver industry-beating volume growth in FY27.

* We largely maintain our EBITDA estimates for FY27/FY28. We value the stock at 12x FY28E EV/EBITDA to arrive at our revised TP of INR2,230 (earlier INR2,110; raised mainly due to lower-than-expected cash outflow toward capex). Reiterate BUY.

Volume up ~2% YoY; realization/t up ~1%YoY

* 4Q consol. revenue/EBITDA/adj. PAT stood at INR42.5b/INR9.0b/INR3.3b (+4%/+14%/-9% YoY and -2%/+9%/in line vs. estimates). Volume rose ~2% YoY to 8.8mt (in line). Realization grew ~1% YoY (+2% QoQ) to INR4,824/t (~1% below our estimates).

* Opex/t declined ~1% YoY (-3% vs. our estimates). Freight costs/employee expenses per ton declined ~6%/1% YoY, while variable cost/t remained flat YoY. Other expenses/t grew ~5% YoY. OPM expanded 1.9pp YoY to ~21%, and EBITDA/t increased ~11% YoY to INR1,025. Depreciation/interest costs increased ~16%/26% YoY. Other income declined ~52% YoY.

* In FY26, revenue/EBITDA/PAT stood at INR147.7b/INR30.5/INR10.5b, up 6% /27%/52% YoY. Volume grew only ~2% YoY to 30mtpa. Realization/t grew ~3% YoY and EBITDA/t was up ~24% YoY at INR1,015. OCF stood at INR22.8b vs. INR21.1b in FY25. Capex stood at INR20.6b vs. INR26.6b in FY25. FCF stood at INR2.4b vs. net cash outflow of INR5.1b in FY25.

Highlights from the management commentary

* Management indicated a steady medium-term demand outlook for the cement industry, expecting industry volume CAGR of 7-8%, led by strong infrastructure spending across industrial corridors, affordable housing, highspeed rail, smart cities, and increasing central and state government capex.

* The company reiterated its capacity target of 75mtpa by FY28-end, and likely to share specific details in near future. Total capex guidance of INR32b-34b for FY27, including INR22b for expansion projects.

* Management maintains adequate limestone reserves across all regions, with ~2.7b tons of limestone available at its operational plants. Additionally, it holds mines across the country, which will support future capacity expansion and entry into new geographies.

Valuation and view

* DALBHARA’s 4QFY26 operating performance was above our estimates due to lower opex/t. In the near term, rising costs of key input materials (fuel, pp bags, diesel) and their availability remain key challenges. Volume growth in 4Q was partially impacted by the unexpected breakdown at its clinker plant in East. It expects newly commissioned capacity in the northeast and an expected new line in Belgaum during the year will support volume growth in FY27E

* We estimate a CAGR of 9%/11% in revenue/EBITDA over FY26-28. We estimate a volume CAGR of ~8% over FY26-28E and EBITDA/t of INR993/INR1,081 in FY27/FY28E vs. INR1,015 in FY26. We estimate ~3% PAT CAGR over FY26-28, due to higher depreciation/interest costs. The company’s net debt is estimated to surge to INR32.6b by FY28 from INR14.2b in FY26. Net-debt-to-EBITDA ratio is estimated at 0.87x in FY28 vs. 0.47x in FY26.

* At CMP, the stock is trading at 12x/10x FY27E/FY28E EV/EBITDA EV/t of USD70/USD67. We value the stock at 12x FY28E EV/EBITDA to arrive at our revised TP of INR2,230 (earlier INR2,110; raised mainly due to lower-thanexpected cash outflow towards capex). Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)