Buy Mankind Pharma Ltd for the Target Rs 2,980 by Motilal Oswal Financial Services Ltd

Margin beat on operational discipline Post two years of earnings consolidation, growth levers align for a sustained re-acceleration

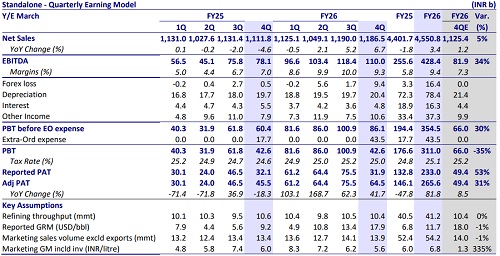

* Mankind Pharma’s (MANKIND) reported revenue was in line with expectations for 4QFY26. It delivered better-than-expected EBITDA/PAT for the quarter, driven by controlled operational costs, higher other income, and a lower tax rate.

* After almost three quarters of subdued growth in the prescription business (Ex-BSV and Consumer Health), MANKIND revived YoY growth in 4QFY26, led by superior execution across chronic therapies.

* The company also improved YoY growth in BSV’s domestic portfolio, supported by enhanced marketing and promotional efforts.

* Notably, MANKIND has achieved greater efficiency and higher MR productivity, with industry outperformance in select therapies.

* Overall growth was offset to some extent due to moderate growth in exports. Specifically, reduced business in LATAM and leadership changes in the Philippines affected exports for the quarter.

* We largely maintain our earnings estimate for FY27/FY28, with an upward revision in the operating profit largely being offset by a step-up in the effective tax rate. We value MANKIND at 40x 12M forward earnings to arrive at TP of INR2,980.

* After two years of stable earnings, we expect 21% earnings CAGR over FY26- 28, led by:

a) sustained outperformance in chronic therapies

b) normalization of the acute portfolio

c) increasing share of the specialty portfolio

d) better prospects in exports

e) improving operating leverage. Overall growth remains broad-based at therapy and product levels. Reiterate BUY.

Cost optimization drives margin expansion and earnings growth

* Sales grew 11.8% YoY to INR34.4b for the quarter (vs est. INR34.3b). ? Gross margin expanded 60bp to 72.2%.

* EBITDA margin expanded 400bp YoY to 27% (vs est. 24.3%), driven by lower employee costs (down 140bp YoY as % of sales) and other expenses (down 200bp YoY as % of sales).

* Accordingly, EBITDA grew at 31.3% YoY to INR9.3b (vs our estimates of INR8.3b).

* Adj. PAT grew 80% YoY to INR5.8b (our est: INR4.4b) due to a significant decline in interest costs.

* Revenue/EBITDA/PAT grew ~17%/18%/5% YoY to ~INR143b/INR36b/INR20b for FY26.

Strong domestic momentum offsets export headwinds

* Domestic business (84% of sales) grew 13.4% YoY to INR28.9b for the quarter, driven by strong growth in the BSV specialty business.

* Prescription business (Rx) (93% of domestic sales) grew 12.9% YoY to INR26.7b, driven by strong performance in chronic therapies

* Consumer business (7% of domestic sales) grew 19.8% YoY to INR2.1b, driven by growth in Manforce, Prega News, Gasofast, and Nimulid.

* Export (16% of sales) grew 4.2% YoY to INR5.6b., impacted by geopolitical headwinds.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412