Neutral Jubilant FoodWorks Ltd for the Target Rs 500 by Motilal Oswal Financial Services Ltd

Weak exit to FY26; near-term stress on margins

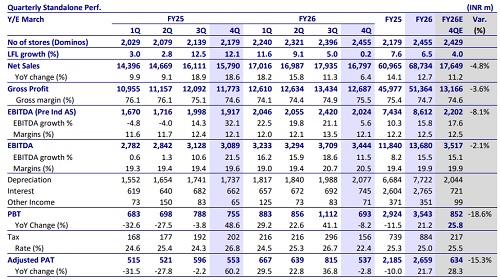

* Jubilant FoodWorks (JUBI) reported 6% YoY standalone revenue growth in 4QFY26, quite soft as compared to 13% growth in FY26. Domino’s LFL growth was flat YoY due to a high base (12%) and the shift of Navratri to 4Q from 1Q in the base. Further, the temporary shortage of LPG impacted 30- 40bp LFL; the issue has now normalized. Delivery revenue grew 10% YoY, with the delivery mix rising to 76%. Management highlighted strong delivery order trends in 1QFY27 and expects improvement in LFL growth.

* Standalone GM expanded 100bp YoY to 75.5% (supported by a better product mix and lower wastage). EBITDA margin (Pre-Ind AS) was flat YoY at 12.1%. EBITDA inched up 5% YoY, quite slow as compared to 16% growth in FY26. Cost inflation in food, packaging, and employee costs is expected to sustain pressure in the near term. The company plans to offset this through calibrated price hikes (a 1% hike so far) and tighter cost controls.

* Domino’s Turkey posted LFL growth of 9%, while Coffy’s LFL declined 9.7% (inflation-adjusted). The PAT margin stood at 7.5% (vs. 4.8% in the base). JUBI stated that DPEU’s finance cost reduced on account of the refinancing of debt from Turkish lira to euro. Domino’s Sri Lanka and Bangladesh reported strong revenue growth of 61% and 29% YoY, respectively.

* While management remains confident on medium-term growth (5-7% LFL), near-term demand trends remain monitorable amid weak dine-in traction. Higher commodity costs, along with LPG shortages and labor costs, are expected to weigh on near-term margins. We estimate standalone revenue CAGR of 13% over FY26-28 and pre-Ind-AS EBITDA margin of 12.5%-13% over FY26-28E. We reiterate our Neutral rating with a TP of INR500.

International business

* Domino’s Sri Lanka revenue was up by 60% YoY to INR367m. No stores were opened in Sri Lanka.

* Domino’s Bangladesh revenue grew 29% YoY to INR209m. No store has been opened in Bangladesh.

* Both Sri Lanka and Bangladesh turned EBITDA positive in FY26.

DPEU supported by currency

* DPEU sales grew 59% YoY to INR7.6b. supported by Turkey's inflation and currency movement. Turkey's inflation of 30% YoY in 4Q and 23% favorable movement in currency led the growth. Post-Ind-AS 29, DPEU delivered 6% revenue growth.

* Domino’s Turkey LFL growth was 9%, while COFFY LFL was down 10%.

* PAT jumped 150% YoY to INR576m (vs. INR230m in 4QFY25), while PAT margin stood at 7.5% (vs. 4.8% in the base).

* In DPEU, it opened eight stores in 4Q, taking the total count to 981.

Valuation and view

* There are no material changes to our EBITDA estimates for FY27 and FY28.

* JUBI is benefiting from strong delivery-led traffic growth, driving near-term outperformance versus peers. On the international front, DPEU’s interest costs are fully funded by the Turkey business with no cash outflow from India.

* JUBI’s focus on customer acquisition and order frequency has been driving strong delivery growth. For dine-in, the company continues to take various steps, such as value offerings and product innovations, to drive channel growth.

* While management remains confident on medium-term growth (5-7% LFL), near-term demand trends remain monitorable amid weak dine-in traction. Higher commodity costs, along with LPG shortages and labor costs, are expected to weigh on near-term margins. We estimate standalone revenue CAGR of 13% over FY26-28 and pre-Ind-AS EBITDA margin of 12.5%-13.0% over FY26-28E. We value the India business at 25x EV/EBITDA (pre-IND AS) and the international business at 10x EV/EBITDA on Mar’28E. We reiterate our Neutral rating with a TP of INR500

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412