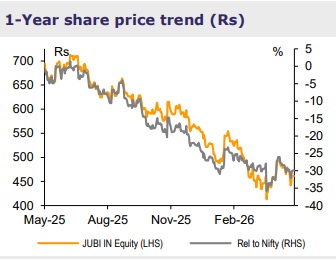

Buy Jubilant FoodWorks Ltd for the Target Rs.550 by Emkay Global Financial Services Ltd

We maintain BUY on JUBI, despite ~8% cut in TP to Rs550 (22x Mar28 EBITDA) from Rs600. JUBI delivered a 5-8% beat to our/street EBITDA estimates in Q4, however, its commentary highlighted near-term inflationary pressures in labor, utility, and logistics, leading us to cut India EBITDA estimates by 6-7%. JUBI attributed the Q4 growth moderation—flat LFL vs 6.5% in FY26—largely to a high base, with 2Y LFL growth remaining in the 6- 7% range across FY26 quarters. The company expects growth trends to improve through FY27, though the guided ~200bps margin gain by FY28E is likely to be delayed to some extent. Encouragingly, JUBI has taken price hikes across select menu mix, which, along with efforts to reduce margin drag from emerging segments (~200bps in FY25/26), should help deliver the targeted margin expansion, in our view. Among emerging formats, Popeyes delivered 28% SSG in FY26 and JUBI plans to accelerate expansion of this format going ahead. The Turkey business delivered 29%/62% revenue/PAT growth in FY26, helped by a return to volume growth in Q4 and favorable FX movements, albeit the Coffy format saw a ~10% LFL decline (inflation adjusted) in Q4. Higher PAT growth in Turkey was driven by debt refinancing.

Underlying demand healthy; Sri Lanka/Bangladesh EBITDA positive in FY26

Consolidated revenue rose 19.3% YoY, led by ~60% growth in DP Eurasia, benefiting from higher favorable currency movement contributing ~23% to YoY growth and higher inflation in Turkey contributing ~30%. JUBI’s India revenue grew 6.4% in Q4, led by Domino’s India growth at 5%, driven by order growth of 10.4% (0.2% LFL). Growth was impacted by temporary factors (sequential occurrence of Ramadan, school examinations, and the shift of Navratri into Q4 from Q1 last year) and LPG issues impacting Domino’s LFL by 30-40bps, though the management alluded that the underlying demand trends remained healthy. The management reiterated its medium-term target of 5-7% LFL. India gross margin (GM) increased ~100bps YoY to 75.5%, led by better mix and reduction in wastage. India business EBITDA margin (pre-IndAS) stood at 12%, down ~10bps (though ~2% higher vs our estimates), largely due to inflation in wage and energy cost. Sri Lanka/Bangladesh posted robust double-digit revenue growth at ~61%/29% YoY in Q4. Encouragingly, both markets have turned EBITDA positive in FY26

Strong momentum continues in Popeyes

Popeyes continued to demonstrate strong momentum, delivering 28% SSG growth in FY26, with southern markets (Bengaluru and Chennai) witnessing even stronger growth despite an expanding store base. The company added 5/17 stores in Q4/FY26, taking the total store count to 78. The management remains confident on the long-term scale-up potential of Popeyes, supported by the underpenetrated chicken QSR category and strong consumer acceptance for the Popeyes brand, as reflected in category-leading app and store ratings across key markets.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

Ltd ( 1 ).jpg)