Neutral Jyothy Laboratories Ltd for the Target Rs. 275 by Motilal Oswal Financial Services Ltd

Margin miss continues on high competition

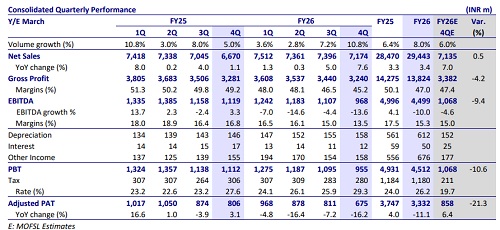

* Jyothy Laboratories (JYL) posted 8% (in line) sales growth in 4QFY26, while volumes rose ~11% (est. 6%; 4QFY25 5%, 3QFY26 7%). Volume growth was broad-based across categories. As seen in 3QFY26, the difference between value and volume growth was primarily due to pricing actions in dishwash amid high competition. The competitive intensity remained high among peers, offering higher grammage at lower MRPs. The company expects this gap to narrow going forward. Fabric Care continued to demonstrate strong growth, clocking 14% growth YoY. HI and Personal Care reported 3% and 20% growth on the back of a 5% and 9% decline in the base, respectively. Dishwash revenue was flat YoY, but volume grew by 5%, driven by pricing actions and promotions.

* GM remained under pressure and contracted 400bp YoY to 45.2% (est. 47.4%, 46.5% in 3QFY26). Since JYL’s 50-60% of RM is crude-linked, cost inflation is expected to sustain. The company has taken ~4% price hike at the company level to pass on RM inflation and will remain watchful of any further price hikes. EBITDA margin contracted 330bp YoY to 13.5% (miss). Management flagged near-term margin uncertainty due to geopolitical volatility, forex and crude fluctuations, and intensifying competition.

* We remain cautious on JYL’s near-term outlook, with elevated competitive intensity from category leaders likely to constrain both growth and margin. This, coupled with sharp inflation in crude and its derivatives, is expected to further pressure JYL’s performance. We remain cautious on JYL’s margin recovery owing to competition; margin recovery further appears delayed in high-cost inflation. Following a ~500bp EBITDA margin expansion to 17.5% over FY23–FY25, we believe margins had peaked and model a moderation to ~15–15.5% over FY27–FY28 (15.3% in FY26). We reiterate our Neutral rating on the stock with a TP of INR275 (premised on 25x Mar’28E P/E).

Strong volume growth at 11%; miss on profitability

* In-line revenue growth, beat on volume growth: JYL’s net sales grew 8% YoY to INR7,174m (est. INR7,135m). Volume growth was 10.8% (est. 6%, 5% in 4QFY25) in 4QFY26. Consumption trends in 4Q remained steady, with stable demand and sustained volume growth across categories. Rural demand remained relatively stable through most of the year, while urban demand showed improvement following GST rate changes.

* Strong Fabric Care growth continued: Fabric Care delivered value growth of 14.4% and volume growth of 17.8% YoY in 4QFY26. Liquid detergent category pricing remains competitive; the company continues to scale liquid detergents while ensuring profitability remains intact. The Dishwash segment recorded flat value growth and 5% volume growth in 4QFY26, with the divergence attributable to price reductions and increased grammage offerings. Liquids continued to outperform bars.

* HI benefits from an improving mix, while GST aids in Personal Care, albeit on a low base: HI and Personal Care reported 3% and 20% growth on the back of 5% and 9% decline in the base, respectively. Personal care posted 20.8% volume growth as demand improved after GST rate changes, with the impact becoming fully visible in 4Q. In HI, there was strong volume growth in Liquid Vaporizers, while Coils saw a decline.

* Miss on margins: Gross margin contracted 400bp YoY to 45.2% (est. 47.4%, 46.5% in 3QFY26). GM remained under pressure due to crude inflation amid ongoing geopolitical tensions. Packaging costs account for 15-20% of JYL’s total material cost. Employee expenses and other expenses rose 9% each, while Ad spends declined 6% YoY. EBITDA margin contracted 330bp YoY to 13.5%. (est. 15%).

* EBIT margin continues to contract for most segments: Dish washing EBIT margin contracted sharply by 770bp to 10.4%, while Fabric Care contracted 420bp to 18%. Personal Care EBIT margins contracted 270bp to 7.9%. HI EBIT margins, on the other hand, improved from -7% to +6.3%.

* Decline in profitability: EBITDA declined by 14% YoY to INR968m (est. of INR1,068m). Similarly, PBT declined 14% YoY to INR955m (est. INR1,068m). Adj. PAT dipped 16% YoY to INR675m (est. INR858m).

* In FY26, revenue grew 3% YoY, while EBITDA/APAT declined 10%/11%, respectively.

Highlights from the management commentary

* Rural demand remained relatively stable through most of the year, while urban demand showed improvement following GST rate changes.

* Management further alluded that while urban demand showed early signs of recovery, persistently high crude prices and retail inflation pose a risk to overall demand momentum.

* JYL’s 50-60% of RM is crude-linked. Therefore, a sharp increase in crude prices, along with a weaker rupee, has put pressure on the overall cost structure.

* JYL took ~4% price hike at the company level in March. ? The company expects to narrow the gap between value and volume growth in the near term.

Valuation and view

* We largely maintain our EPS estimates for FY27E-28E.

* We have been cautious on revenue growth and sustaining operating margin previously as well. We believe the elevated competitive intensity from larger players will continue to impact growth/margin in the near term. This, coupled with sharp inflation in crude and its derivatives, is expected to further exert pressure on JYL’s performance. EBITDA margin witnessed ~500bp expansion to 17.5% during FY23-FY25. We model a downward trajectory and cut EPS by 5-6% for FY26-FY28. In addition, we model a 9% revenue and 11% EBITDA CAGR for FY26-FY28.

* We reiterate our Neutral rating on the stock with a TP of INR275 (premised on 25x Mar’28E P/E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412