Buy Dr. Agarwals Health Care Ltd For Target Rs. 610 by Motilal Oswal Financial Services Ltd

Surgical franchise in full stride with ~10K patients per day

Operating leverage to drive a 400bp expansion in RoE and RoCE each

* Dr. Agarwal Healthcare (DAHL) exited FY26 with a strong all-round performance, outperforming our growth, margins, and cash conversion estimates. DAHL continues scaling its surgical franchise and network at an impressive pace, reinforcing our conviction in the secular growth story.

* DAHL delivered strong FY26: The revenue/EBITDA/PAT growth of 22%/ 26%/60% YoY, margins of 26-27%, and CFO at ~91% of EBITDA signal high earnings quality.

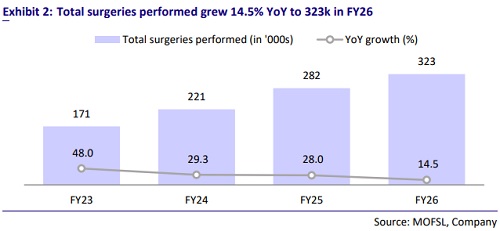

* Surgical engine in full stride:surgeries grew 14.5% YoY to 323k, realizations improved 8.5% YoY to ~INR42.9k due to premiumization and case mix improvement, and femto-assisted cataract surgeries jumped 87% YoY.

* DAHL’s execution remains best-in-class: Network stood at 288 (+57 in FY26), the number of doctors was 968, volumes stood at 3.0m (+24% YoY), SSS came in at 14%, and mature facilities stood at 30.5%.

* South India anchors growth (61% revenue, 64% surgeries): Having said this, all regions grew in double digits with no weak links in the portfolio.

* Operating leverage + cash conversion to drive a 400bp expansion in RoE and RoCE each over FY26-28E.

* Company is expected to add 60 facility in FY27, while deepening in Mumbai and Delhi-NCR is underway, keeping the growth runway intact.

* We forecast a revenue/EBITDA/PAT CAGR of 22%/23%/40% over FY26–28E, driven by network expansion, specialist doctor additions, faster center rampups, and a premiumizing surgical mix. We reiterate our BUY rating with an SoTP-based TP of INR610 (surgical at 25x, opticals at 15x, and pharmacy at 10x EV/EBITDA).

Expanding networks and advanced procedures fuel surgical growth

* DAHL’s surgical business continues to scale strongly, with surgeries rising 14.5% YoY to 323k in FY26 and average revenue per surgery increasing 8.5% YoY to ~INR42.9k, reflecting premiumization, richer case mix, and growing adoption of advanced treatments.

* This growth is supported by broad-based expansion across specialties, with cataract and other surgeries growing 14% and 19% YoY, respectively, while femto-assisted cataract procedures surged 87% YoY and increased their share of total specialized surgical procedures to 21%.

* Parallel investments in network expansion and clinical capabilities are being executed through an organic-led strategy, with 57 facilities added in FY26, taking the network to 288 facilities, while the doctor base expanded to 968 from 403 in FY22.

* Strong execution is visible in healthy operating metrics, with patient volumes increasing 24% YoY to 3m, same-store sales growing 14% YoY.

* Supported by a scalable hub-and-spoke network encompassing 288 facilities across 155 cities in 10 countries, and with management’s plan to add 60 facilities in FY27, DAHL is well-positioned to drive sustained volume growth, premiumization, and market share gains.

South anchors growth as expansion gains momentum

* DAHL’s regional portfolio remains anchored by South India, which contributed 61.2% of FY26 revenue and 64% of total surgeries, reinforcing its leadership position in the company’s largest and most mature market.

* Growth was broad-based across geographies, with FY26 revenue increasing 22.0% YoY, led by South (+22.6%), while North (+20.9%), West (+19.0%), and East (+18.5%) also delivered healthy expansion, highlighting the scalability of the operating model beyond its core markets.

* DAHL’s strong patient reach is reflected in 2.87m domestic patients served during FY26, with South accounting for nearly 66% of volumes, emphasizing its deep market penetration and brand strength in the region.

* Going forward, DAHL is focused on deepening its dominance in South India while accelerating expansion in underpenetrated markets such as Mumbai and Delhi-NCR, positioning the company for broader geographic diversification and sustained growth.

Healthy growth, stable margins, and strong cash conversion support higher returns

* DAHL delivered a strong FY26, with revenue, EBITDA, and PAT increasing 22%, 26%, and 60% YoY, respectively, reflecting healthy operating momentum across the business.

* It maintained an EBITDA margin of 26–27% throughout FY22–26, demonstrating the resilience and scalability of its operating model.

* Liquidity remained strong in FY26, with operating cash flow representing ~91% of EBITDA, underlining robust cash conversion and earnings quality.

* Continued profitability improvement is expected to support ~400bp expansion in both RoE and RoCE over FY26-28E, driven by operating leverage and efficient capital deployment.

Valuation and view

* We forecast a revenue/EBITDA/PAT CAGR of 22%/23%/40% over FY26–28E, supported by deeper market penetration, continued facility expansion, the addition of specialist doctors, and strong brand equity.

* Growth is expected to be further driven by the robust pace of new facility additions, faster ramp-up of existing centers, and an increasing mix of premium surgical procedures.

* We value DAHL using the SoTP method. We assign EV/EBITDA multiples of 25x to the surgical business, 15x to the optical business, and 10x to the pharmacy business, while adjusting for its stake in Dr. Agarwal Eye Hospital and Thind Hospital, to arrive at our TP of INR610. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412