Buy Blue Jet Healthcare Ltd for the Target Rs 580 by Motilal Oswal Financial Services Ltd

Pharma destocking hurts performance; FY27 recovery likely Earnings above our estimates

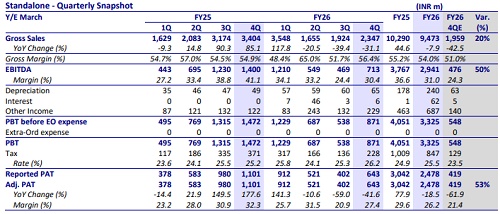

* Blue Jet Healthcare (BLUEJET) reported revenue of INR2.3b in 4Q, down 31% YoY, primarily due to pharma intermediate (PI) destocking (revenue down 99% YoY). This was partially offset by the healthy performances of contrast media/high-intensity sweeteners (up 91%/24% YoY).

* However, we expect the pharma intermediates segment to recover in FY27, boosted by improving shipment trends, normalization after industry-wide destocking, and strong visibility in select programs. This will be further supported by management guidance of double-digit growth in the contrast media segment on the back of new launches.

* Factoring in recovery in the PI segment and management guidance, we raise our FY27/FY28 earnings estimates by 14% each. We value the stock at 30x FY28E EPS to arrive at our TP of INR580. Reiterate BUY.

Valuation and view

* We anticipate a recovery in pharma intermediates in FY27, led by the end of destocking. Growth is likely to be supported by strong momentum in contrast media through new launches, NCE molecule commercialization, backward integration, and capacity expansion, alongside recovery in pharma intermediates supported by healthy order visibility and new opportunities.

* Further, ongoing investments in Vizag, Hyderabad, and CDMO capabilities are expected to support the company’s next phase of commercialization-led growth.

* We expect a CAGR of 16%/19%/16% in revenue/EBITDA/PAT over FY26-28. Factoring in recovery in the PI segment and management guidance, we raise our FY27/FY28 earnings estimates by 14% each. We value the stock at 30x FY28E EPS to arrive at our TP of INR580. Reiterate BUY

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)

More News

Buy Raymond Lifestyle Ltd for the Target Rs 880 by Motilal Oswal Financial Services Ltd