Buy Blue Star Ltd For Target Rs.1,873 by Prabhudas Liladhar Capital Ltd

Capturing India's Massive Cooling Opportunity

We initiate coverage on Blue Star (BLSTR) with ‘BUY’ rating and SoTP-based TP of INR1,873, implying 44x FY28E P/E, given its strong earnings visibility, improving profitability and leadership across the heating, ventilation and air conditioning (HVAC) industry. BLSTR is one of India's leading air conditioning and commercial refrigeration companies, with a diversified presence across room air conditioners (RAC), commercial air conditioners (CAC), electro-mechanical projects (EMP), commercial refrigeration and industrial solutions. The company is well positioned to capitalize on India's structural cooling demand, supported by

1) Rising RAC penetration and market share gains

2) Leadership in CAC and EMP

3) Timely expansion of manufacturing capacity through the Sri City facility

4) Emerging opportunities from data center expansion and infrastructure development. We expect revenue/EBITDA/PAT to grow at 18.9%/22.9%/24.9% CAGR over FY26-28E, driven by sustained demand across both the Unitary Cooling Products (UCP) and EMP businesses, higher capacity utilization and operating leverage. Initiate with ‘BUY’.

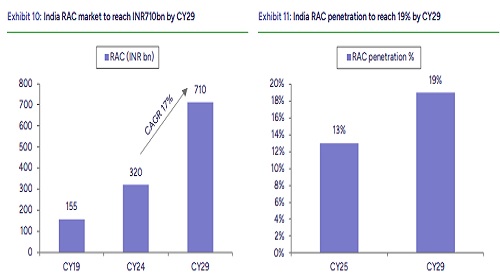

Positioned to capture India’s RAC penetration story:

India's RAC penetration remains low at ~13%, providing a long runway for growth. BLSTR has steadily increased its RAC market share from ~7% in FY14 to ~14.3% in FY26 through strong brand positioning, an expanding product portfolio and a growing distribution network. With continued investments in manufacturing, product innovation and channel expansion, the company is well placed to benefit from the structural growth in residential AC demand.

Capitalizing on India's data center expansion:

India's data center market is witnessing a multi-year investment cycle driven by cloud adoption, AI workloads and digital transformation. As the market leader in mechanical, electrical & plumbing (MEP) solutions for data centers, BLSTR is estimated to have generated ~INR10bn revenue from this segment in FY26. The management expects this opportunity to scale significantly over the medium term, supported by a robust project pipeline and increasing investments in hyperscale and colocation facilities.

Sri City facility expands RAC capabilities:

BLSTR has strengthened its manufacturing footprint through phased investments in its Sri City facility, which has expanded RAC manufacturing capacity to 1.2mn units annually. Combined with higher localization, backward integration and manufacturing automation, the facility enhances supply-chain resilience, supports new product launches and provides sufficient headroom to capture future demand while driving operating leverage and margin improvement.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271