Neutral R R Kabel Ltd for the Target Rs. 2,020 by Motilal Oswal Financial Services Ltd

Resilient demand; margin expansion on track

* RRKABEL is experiencing healthy demand across key end-user segments. However, near-term growth is expected to moderate due to the ongoing crisisin West Asia. The company: 1) expects marginsto remain stable, supported by effective cost pass-throughs, and 2) remains focused on scaling its cables and export businesses through its INR12b capex and expansion into higher-voltage segments. While exports have been impacted by the ongoing Middle East crisis, the company expects the impact to gradually normalize over time.

* Near-term revenue growth is expected to be largely price-led, fueled by elevated copper and aluminum prices and the subsequent price hikes. Meanwhile, the FMEG segment remains in an investment phase, with the company expanding its presence in kitchen appliances and premium product categories. Management continues to target breakeven in the FMEG segment by FY27.

C&W: Pricing actions amid elevated RM costs

* Copper and aluminum prices remained elevated, rising ~20% and ~15% YoY, respectively, in FY26. Given their ~55%-60% share in RM costs, the sharp increase resulted in a meaningful cost push. The uptrend continued into 1QFY27, with prices increasing sharply by ~57%/~63% YoY in Apr– May’26.

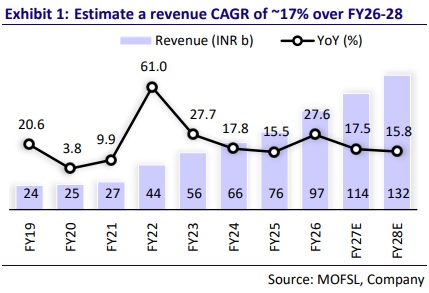

* The C&W segment delivered strong performance in FY26, with volumes growing ~16% and revenue rising ~31%, aided by calibrated price hikes and effective pass-through of higher input costs. The company expects C&W volume growth of ~16%-18% in FY27, continuing to outpace industry growth.

* Within the segment, wire volumes are projected to grow ~11%-12%, while cable volumes are expected to witness a stronger ~25% growth over the next two years, supported by rising demand from infrastructure, data centers, renewables, and exports. As a result, the share of cables in the W&C mix is expected to increase from ~27% currently to ~31% over time.

Demand drivers, market exposure, and distribution strength

* Demand is fueled by the power transmission segment (~30% contribution), followed by utilities, EPC contractors, and discoms. The cable portfolio spans EHV, HV, MV, and LV segments, reflecting a fullstack presence across voltage categories. Within infrastructure, incremental demand drivers include data centers, renewable energy, and replacement demand, along with applications such as overhead cabling.

* Volume growth remains robust, reflecting healthy underlying demand across key end-user segments such as housing, real estate, infrastructure, renewables, and broader electrification. This momentum is driven by the government’s sustained capex push, alongside continued traction in private sector investments, supporting a structurally strong demand environment.

* The industry remains largely relationship-driven, particularly in cables, where ~90% of sales are routed through distributors. End-user exposure is well diversified across power transmission, utilities, EPC, discoms, data centers, and renewables, supporting demand visibility.

* The company has significantly strengthened and scaled its distribution network, building a strong nationwide presence with over 6,000 dealers across India, supported by nearly 150,000 retail touchpoints. Over FY20-26, its dealer network clocked ~16% CAGR, strengthening market reach and supporting volume growth.

* RRKABEL’s partnership with Kolkata Knight Riders as Principal Partner for IPL’26 has enhanced its brand visibility across India. The company leverages ATL, BTL, digital campaigns, and on-ground electrician outreach programs.

Growth strategy, expansion of exports, and margin profile

* Under Project RRISE, management remains on track to deliver ~18% CAGR in the W&C segment and expand margins by 3.0pp to ~10.5% by FY28. Around 1.3pp of the targeted margin expansion has already been achieved. FY27 margin guidance stands at ~9.5%, supported by better utilization, operating leverage, improved product mix, premiumization, export growth, automation, and logistics optimization. The portfolio remains skewed toward wires (~73%) versus cables (~27%) in FY26.

* Exports contributed ~26% of revenue in FY26, with the company targeting higher growth in the C&W export business through product expansion and deeper penetration across existing and new markets. While Middle East disruptions may continue to impact 1QFY27, diversified exports and domestic demand are expected to partly offset the impact. Europe remains a key focus market, supported by opportunities in non-specialized cables and replacement demand from aging infrastructure. The company exports C&W to 74 countries and has over 57 international certifications.

* Profitability remains higher in wires, with domestic margins at ~12%, compared to ~5%–6% in international markets due to their commoditized nature. In cables, domestic margins are ~5–6% due to lower scale, while exports are stronger at ~10%–12%. Freight costs are largely pass-through, and scaling up the cables business remains a key lever for margin expansion.

* Wires command ~10%–12% market share, supported by a strong distribution network, while cables remain underpenetrated at ~2%, offering significant headroom for scale-up. However, rising competitive intensity, including the entry of UTCEM, could affect the segment in the near term.

Capacity expansion and a shift toward high-voltage cables

* Cable utilization remains strong at ~90%, while wire utilization is relatively lower at ~70% due to higher SKU complexity. To capitalize on the cable opportunity, the company has outlined an INR12b capex plan over FY26-FY28E, with ~80% allocated toward expanding cable manufacturing capacity, and the balance to be invested in modernization, automation, warehousing, and digital systems to improve operational efficiency. The company has already invested INR3.5b, while the majority of the capex is expected to be deployed in FY27.

* RRKABEL currently manufactures cables up to 66 kV (with 132 kV capability) and aims to scale up to 132 kV and 220 kV over the next three years. This is expected to expand the company’s addressable market and support margins, as higher kV cables are more complex, face lower competition, and command premium pricing.

FMEG segment: Expansion in its portfolio

* RRKABEL’s FMEG segment currently contributes ~10% of total revenues and has a well-defined product mix, with fans accounting for ~50%, lighting contributing ~32%–35%, and the remaining ~18% coming from appliances and switches/switchgear. Premium and mid-premium products, such as BLDC fans and smart lighting, already account for ~20% of segment revenues.

* Building on this base, the company has expanded its portfolio by entering the kitchen appliances segment under its premium brand ‘RR Signature’, with the launch of mixer grinders, electric cooktops, and hand blenders. In parallel, it has strengthened its air coolers portfolio by introducing industrial (semi-commercial) variants, broadening its presence within the consumer electrical ecosystem. The company plans to build on this momentum by progressively adding new categories in kitchen appliances over the coming years.

* Management expects the FMEG segment to deliver ~25% revenue CAGR by FY28, while FY27 revenue growth is guided at ~20%-25%. The company also targets breakeven in FY27, supported by operating leverage and scale benefits. Earlier breakeven plans were deferred due to weak summer demand and higher input costs, particularly in categories where price pass-through takes longer, resulting in temporary margin pressure in 4QFY26.

Valuation and view

* RRKABEL witnessed an uptick in C&W’s performance during FY26 after a lower margin in FY25 led by a pickup in demand and a sharp increase in copper and aluminum prices, which are largely pass-through in nature for C&W companies. The segment’s EBIT margin expanded to ~8.9% vs ~7.4% in FY25. Additionally, lower EBIT loss from the FMEG business supported the company’s overall operating performance.

* While the C&W segment is expected to deliver strong revenue growth, driven by higher RM prices (copper/aluminum prices in Apr-May’26 rose ~57%/63% YoY), we expect competitive intensity to increase with the anticipated entry of UTCEM in this space by 4QFY27. We believe UTCEM is likely to have a higher share of wires in its product portfolio, where gaining market share is relatively easier than in cables. EBIT margin in RRKABEL’s C&W segment has remained volatile over the last few years, making margin stability a key monitorable going forward.

* Given the higher RM prices and better margin in FY26, we increase FY27/28E EPS estimate by 9%/12%, respectively. We reiterate our Neutral rating on the stock with a TP of INR2,020, based on 30x FY28 EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412