Buy Brigade Enterprises Ltd for the Target Rs. 910 by Motilal Oswal Financial Services Ltd

FY26 pre-sales impacted by lack of material launches

Residential launch pipeline of 12msf provides near-term growth visibility

* In 4QFY26, Brigade Enterprises’ (BRGD) pre-sales rose 3% YoY to INR25.2b (6.7% below estimates). Volumes stood at 2msf, down 4% YoY. BRGD launched seven residential projects with a TDA of 4msf in 4Q across Chennai, Bengaluru, and Hyderabad. It sold roughly 2msf that came from Brigade Lumina (0.6 msf) in North Bengaluru, which sold about 85% of the units, and Brigade Belvedere (1.04 msf), which sold about 19.7% of the units (150 units sold/760 launched).

* In FY26, pre-sales declined 5% YoY at INR74b, while volumes declined 13% YoY to 6.1msf. Overall, the company launched 12 residential projects during the year with a TDA of 8.3msf across Bengaluru, Hyderabad, and Chennai. In FY26, it added ~13msf of projects with a GDV of ~INR150b, primarily across Bengaluru and Hyderabad. The company plans to launch ~11.59msf in the next four quarters across Bangalore (6 projects), Chennai (3 projects), Hyderabad (2 projects), and Mysuru (3 projects).

* In FY27, BRGD plans to launch 11.6msf (INR116b GDV) in Bengaluru, Chennai, and Hyderabad. On the back of sustenance sales and new launches, we bake in a 20% CAGR in pre-sales over FY26-28E, reaching INR107b.

Collections lack in FY26 to spill over in FY27/28

* Consolidated collections rose 3% YoY to INR19.9b. CFO stood at INR3.8b, down 35% YoY due to a rise in construction costs. In FY26, collections stood at INR75b, rising 3% YoY, while CFO declined 34% YoY to INR14.1b.

* Gross debt rose INR7.3b to INR52.3b, while net debt rose to INR23b (INR4b increase QoQ). Its net debt-to-equity stood at 0.3x by 4Q-end (vs 0.2x in 3QFY26); the cost of debt declined to 7.57%. As launches were deferred in FY26, collections are estimated to come in FY27/FY28; hence, we bake in a 19% CAGR over FY26-28E to INR66b.

Leasing to grow with new assets coming in; Hospitality occupancy to rise

* Leasing: In FY26, leasing revenue grew 10% YoY to INR13b, while EBITDA stood at INR7.3b, with a margin of 56%. Retail footfalls increased 7% YoY, with an 18% YoY growth in consumption. Portfolio occupancy stood at 88%. 4.51msf of area is expected to be launched in the next four quarters. We bake in an 11% CAGR in lease rentals over FY26-28 to INR16b.

* Hospitality: In FY26, Brigade Hotel Ventures Limited (BHVL) reported revenue growth of 13% YoY to INR6b, while EBITDA stood at INR2.1, up 11% YoY.

* BHVL currently has 1,604 keys. Nine hotels with a total of 1,700 keys are under the planning stage, of which six hotels with 940 keys are in agreement with Marriott International.

P&L performance

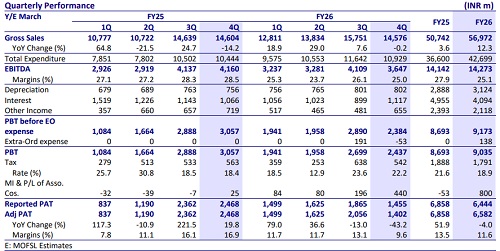

* In 4QFY26, revenue was flat YoY at INR14.6b. EBITDA stood at INR3.6b, down 12% YoY. EBITDA margin came in at 25%. Adj. PAT was at INR1.4b, down 43% YoY, clocking a margin of 9.6%.

* In FY26, revenue rose 12% YoY to INR57b. EBITDA was flat YoY at INR14.3b, with margins at 25%, while adj. PAT dipped 4% YoY to INR6.6b, with margin at 11.6%.

* The Board has recommended a bonus issue of 1:3, i.e., one bonus share of INR10 each for every three equity shares held by the shareholders as of the record date, subject to the approval of the members of the company.

Valuation and view

* Despite a lack of material launches in FY26, the company also has a strong residential launch pipeline of ~12msf, which should enable it to sustain the growth traction going forward.

* We value the residential segment by DCF of cash flows and commercial at a cap rate of 8.5%.

* We reiterate our BUY rating with a TP of INR910, implying an 18% potential upside.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412