Buy Shriram Finance Ltd for the Target Rs. 1,175 by Motilal Oswal Financial Services Ltd

Capital strength and NIM expansion to accelerate earnings growth

Lower funding costs and operating leverage support profitability outlook

Shriram Finance (SHFL) continues to reinforce its position as a leading retail-focused NBFC, backed by its strong presence in rural and semi-urban markets, diversified product portfolio, and disciplined execution capabilities. Over the years, the company has built a robust customer franchise across vehicle finance, MSME lending, and other retail lending segments, enabling it to consistently deliver resilient performance across economic cycles. The company’s well-established franchise, further strengthened by its strategic partnership with MUFG, is well positioned to capitalize on emerging growth opportunities, supported by strong execution and deep customer relationships.

* SHFL’s strategic partnership with MUFG, involving the acquisition of a ~20% stake through a capital infusion of ~USD4.4b, marks a transformational milestone for the company. The enhanced capital base is expected to strengthen SHFL’s growth outlook and support medium-term AUM growth of ~18-20%, compared to its historical growth trajectory of ~15-16%. Growth is likely to be driven by rising financing penetration, resilient rural demand, and a structurally lower cost of funds, with borrowing costs expected to decline by ~1pp over the next 2-3 years.

* Despite its strong capital position, SHFL does not intend to materially alter its core business model or pursue aggressive expansions. Instead, the company focuses on deepening its presence in rural and semi-urban markets, particularly across northern, central, and eastern India, where it continues to see significant headroom for penetration and sustainable growth.

* Vehicle finance remains a core strength for the company, driven by its market leadership in used vehicle financing and increasing opportunities in new vehicle finance through customer upgrades and retention. SHFL also maintains a strong position in 2W finance. In MSME lending, the company focuses on prudent cash flow-based underwriting while gradually increasing the share of secured lending. Gold loans are also emerging as a meaningful growth driver, supported by crossselling opportunities, branch expansion, and deeper engagement with the existing customer base.

* Asset quality trends remain stable, with recent stress (in Mar’26 quarter) largely driven by temporary cash flow disruptions rather than structural weaknesses. SHFL maintains a conservative provisioning stance and expects credit costs to gradually moderate, supported by a rising secured lending mix.

* SHFL’s continued emphasis on disciplined underwriting and rural-focused expansion provides a strong foundation for sustainable earnings growth. With balance sheet strength improving and credit costs expected to remain below 2%, the company’s earnings trajectory is likely to be driven by a combination of healthy AUM growth, margin stability, and improving operating leverage.

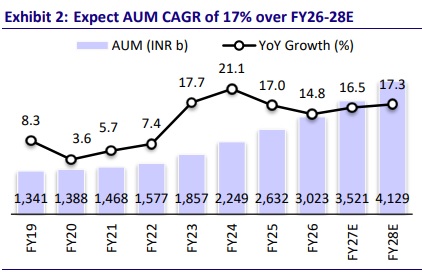

* We expect SHFL to deliver a CAGR of ~17%/~26% in AUM/PAT over FY26-28E, along with RoA/RoE of ~3.8%/13% by FY28E. Reiterate BUY with a TP of INR1,175 (premised on 2.2x FY28E BVPS).

MUFG partnership strengthens capital base and growth trajectory

* SHFL’s strategic partnership with MUFG, involving the acquisition of a 20% stake through a capital infusion of ~USD4.4b, marks a transformational milestone for the company. It will materially strengthen SHFL’s balance sheet, funding profile, and long-term growth capacity while enhancing its capabilities across digital solutions, treasury management and liability diversification through access to MUFG’s global expertise and network.

* Supported by a stronger capital base and improved funding flexibility, SHFL expects its medium-term AUM growth trajectory to improve to ~18-20%, driven by structural credit demand, rising financing penetration, resilient rural demand, and a gradual reduction in the cost of funds. Despite having an enhanced growth opportunity, the company remains committed to disciplined execution and its core business philosophy, balancing scalable growth with prudent risk management and portfolio stability.

Diversified product expansion and customer retention reinforce growth outlook

* SHFL focuses on rural and semi-urban India, where it continues to see significant untapped financing opportunities, particularly across northern, central, and eastern regions. Rather than aggressively expanding into metro markets, the company aims to deepen penetration within existing geographies and customer ecosystems.

* Vehicle finance remains a key strength, supported by leadership in used vehicles and rising opportunities in new vehicle financing through existing customer upgrades. SHFL also continues to strengthen its position in 2W finance while selectively expanding into premium motorcycles.

* In MSME lending, SHFL maintains a prudent underwriting approach with a focus on cash flow-based lending while gradually increasing the share of secured lending within the portfolio. Gold loans are emerging as an important growth driver, aided by strong cross-selling opportunities, branch expansion, and dedicated gold loan branches. Despite increasing competitive intensity, it remains confident of sustaining healthy growth and yields in the segment (18- 20%), supported by its strong distribution and diversified customer franchise.

* We expect SHFL to deliver ~17% AUM CAGR over FY26-28E, supported by healthy demand across loan products and improving customer retention.

Margin expansion and operating leverage to strengthen profitability

* A key benefit of the MUFG transaction is the expected structural improvement in SHFL’s liability profile. The company expects ~1pp reduction in borrowing costs over the next 2-3 years, supported by rating upgrades, liability repricing, lower deposit rates, and improved access to debt capital markets.

* Incremental borrowing costs have already started declining, with benefits expected to flow gradually as the liability book reprices. Despite selectively passing on part of the funding benefit to customers, management expects NIMs to remain stable at ~8.5-9.0%, aided by lower CoF and a favorable portfolio mix.

* SHFL also expects its multi-product distribution model to improve branch productivity, cross-selling, customer retention, and operating leverage over time. While the company continues to invest in manpower and branch

expansion, particularly in gold loans, operating expenses are expected to remain well controlled relative to business growth.

* We expect SHFL’s NIM (calc.) to expand to ~8.8%/~9.0% in FY27E/FY28E, supported by declining CoF. We also expect the cost-to-income ratio to gradually improve to ~26-27% by FY28E (FY26: ~30%).

Credit costs set to ease; MSME stress remains contained

* SHFL’s asset quality trends remain broadly stable across business segments, with the recent stress largely attributable to temporary cash flow mismatches rather than any structural weakness in the borrower base. Incremental stress has primarily been confined to select MSME-linked sectors affected by tariffrelated issues, geopolitical disruptions, and export slowdown. However, we believe these pressures remain manageable, supported by resilient rural demand, stable transportation activity, and healthy collections across key portfolios.

* The company maintains a prudent provisioning approach amid prevailing macro uncertainties while remaining confident on recoverability given the rising share of collateral-backed MSME lending. Over the medium term, management expects credit costs to gradually moderate as the secured lending mix improves, customer retention strengthens, and lower funding costs enhance overall portfolio resilience. We estimate credit costs (as a % of avg. assets) at ~1.9%/~1.8% for FY27E/FY28E.

Valuation and view

* The entry of MUFG as a strategic partner marks a significant milestone for SHFL, materially strengthening its capital base, funding profile, and credit credibility. The partnership is expected to enhance SHFL’s ability to scale across vehicle finance, MSME, and retail lending while maintaining financial discipline and operational stability.

* Despite near-term macroeconomic uncertainties, management remains constructive on the broader credit environment, supported by resilient rural demand and healthy financing penetration trends. Vehicle finance demand remains robust, aided by replacement demand, improving rural recovery, and SHFL’s strong positioning in the used vehicle segment. While MSME growth remains relatively moderate due to global headwinds and export-related pressure, diversification into alternative export markets will help contain stress and maintain portfolio stability. Overall, SHFL appears well positioned to deliver healthy AUM growth, supported by improving operating leverage and strong capitalization.

* We expect SHFL to deliver a CAGR of ~17%/~26% in AUM/PAT over FY26-28E, along with RoA/RoE of ~3.8%/13% by FY28E. Reiterate BUY with a TP of INR1,175 (premised on 2.2x FY28E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412