Buy Aditya Birla Real Estate Ltd for the Target Rs. 1,920 by Motilal Oswal Financial Services Ltd

Presales likely to improve post-FY27

New launches support presales in 4QFY26 Aditya Birla Real Estate (ABREL)’s 4Q presales dipped 24% YoY to INR42.9b; however, they were in line with our estimate. In 4Q, the launch of Birla Arika P2 (Sector 31, Gurugram) saw ~INR16b bookings with ~97% sold within a month, while Birla Taranya (Thane) recorded ~INR9.5b bookings, supporting MMR traction. Additionally, the launch of 6 more projects/phases during FY26 supported presales momentum across key projects, including Birla Pravaah (Sector 71, Gurugram), Birla Trimaya P-4 (Bengaluru), Birla Evara (Bengaluru), Birla Evam (Pune), and Birla Punya (Pune). Overall, FY26 presales stood at INR81.4b, broadly flat YoY (in-line).

Birla Niyaara’s P-3 launch to aid FY27 presales; BD to be monitored

The company has planned for the launch of Birla Niyaara P-3 (INR49b GDV) in 1HFY27, whereas other new phases at the existing projects, including Thane, Trimaya, Navya, Punya, Evam, Evara, and Boisar, are likely to be launched in 2HFY27. Given the limited sustenance inventory and few major launches planned in FY27, we expect the current year’s presales to be flat. ABREL entered into the redevelopment space through the acquisition of the Khar West project (~INR17b GDV) in FY26, and we expect this project to be launched in 4QFY27. Further, we expect the Mathura Road project to be launched early in the next year (1HFY28) and hence we bake in 22% YoY presales growth in FY28. The BD activity has been slow in the last one year, and more project additions remain key for the continuity of growth over the medium term.

Deleveraging on the cards

Collections in the quarter declined 7% YoY to INR9.9b. However, despite flattish presales in FY26, collections grew by 23% YoY to INR33b, which is encouraging. Based on the presales growth and project execution, we expect 30% CAGR in collections to INR56b during FY26-28E. Additionally, ABREL expects to receive proceeds worth INR35b (pre-tax) pertaining to the paper division sale in 1QFY27. Net debt has declined by INR3.7b to INR32b in FY26. With the strong cash flows expected in the coming quarters, it would sharply deleverage the balance sheet and offer flexibility in terms of large, outright, or joint development projects.

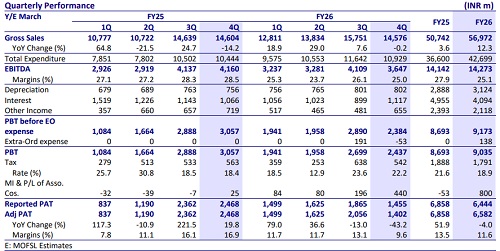

Financials

* In 4QFY26, revenue was down 79% YoY to INR826m. The company reported an operating loss of INR1.6b vs. a loss of INR250m YoY. Adj. PAT stood at INR133m vs. a loss of INR70m YoY.

* In FY26, revenue was down 67% YoY at INR4.1b. EBITDA loss was at INR3.6b vs. EBITDA profit of INR295m YoY. Loss after tax stood at INR784m vs. a loss of INR373m YoY.

Valuation and view

* ABREL has recorded robust scale-up in the real estate segment since its inception, as it clocked a 61% presales CAGR during FY20-26. Further, this growth has come along with maintaining focus on balance sheet strength. Exit from the paper business in FY27 would lead to the release of management bandwidth vis-à-vis increased focus on real estate development. The BD activity has been slow in the past one year and remains crucial for better growth visibility over the medium term. Hence, we are currently valuing the residential business at its NAV, and ramping up in the BD activity would unlock value.

* The focus on sharply ramping up the annuity portfolio is positive and would provide cash flow stability post-FY30.

* We have a BUY rating on the stock with a TP of INR1,920, implying a 21% upside potential.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412