Buy Home First Finance Ltd for the Target Rs. 1,425 by Motilal Oswal Financial Services Ltd.

Entering FY27 with improved execution and growth visibility

AUM growth healthy at ~25% YoY; NIM dips ~10bp QoQ

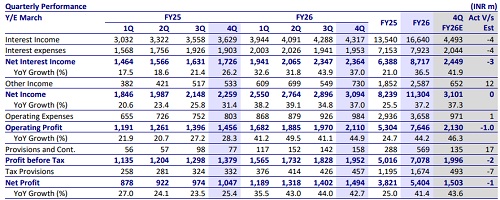

* Home First Finance (HOMEFIRST)’s 4QFY26 PAT grew 43% YoY to INR1.5b (in line). PAT for FY26 grew ~41% YoY to INR5.4b. NII in 4QFY26 grew 37% YoY to INR2.4b (in line). Other income grew 37% YoY to INR730m.

* Opex grew 23% YoY to INR984m (inline). PPoP rose ~45% YoY to INR2.1b (inline). PPoP for FY26 grew ~44% YoY to INR7.6b.

* Credit costs stood at INR158m (17% higher than est.), translating into an annualized credit cost of ~50bp (PQ: ~47bp and PY: ~30bp).

* HOMEFIRST’s future growth is expected to be driven by a combination of calibrated distribution expansion, deeper market penetration, and sustained productivity gains. The company plans to add ~30-40 branches in FY27 while simultaneously increasing branch density in existing high-potential cities, strengthening customer access, and sourcing efficiency. This physical expansion is complemented by a stronger connector ecosystem (~78% of leads generated), enabling a larger addressable market and improved conversion. Management has guided ~25% AUM growth in FY27.

* Management clarified that HOMEFIRST continues to operate within the affordable segment and is not moving towards prime lending, and the increase in ticket sizes reflects higher property values (on the back of inflation), rather than any shift in risk profile or product positioning. The company does not expect higher ticket sizes to lead to any yield compression, as customers continue to demonstrate willingness to pay a premium for faster and more flexible access to credit.

* HOMEFIRST demonstrated resilience in navigating transitory headwinds around growth, attrition, and early-stage delinquencies in 1HFY26, with operational execution improving meaningfully as the year progressed. The company enters FY27 on a stronger footing, supported by stabilized teams, improved on-ground execution, and strengthening asset quality trends. Management remains confident of sustaining stable spreads, aided by its 100% floating-rate balance sheet, which limits interest rate risk and preserves pricing flexibility. Overall, with improving operational momentum and a steady credit environment, the franchise is well-positioned for the next phase of growth.

* The stock currently trades at ~2.6x FY27E P/B. We estimate a CAGR of ~23%/~18% in AUM/PAT over FY26-28E and an RoA/RoE of ~3.7%/14.2% in FY28E. Reiterate BUY with a TP of INR1,425 (based on 2.6x FY28E BV).

Asset quality improves due to stronger collections/underwriting discipline

* GS3 declined ~20bp QoQ to 1.8% and NS3 also declined ~20bp QoQ to 1.4%. PCR improved ~2pp QoQ to ~24%.

* 1+dpd improved ~60bp QoQ to 4.7%. Bounce rates declined ~80bp QoQ to ~15.9% in 4QFY26 (v/s ~16.7% in 3QFY26). Apr’26 bounce rates were 16.3%.

* HOMEFIRST has focused on strengthening portfolio performance through tighter front-end underwriting, improved collection discipline, and sharper resolution of early bucket delinquencies. Early indicators suggest improving collection trends and lower fresh slippages in Apr’26 compared to the previous two years, with no material stress emerging from external macro factors. We estimate credit costs of ~40bp/35bp in FY27E/FY28E.

AUM rises ~25% YoY; BT-OUT rate declines YoY and QoQ

* Disbursements grew 24% YoY/ 19% QoQ to ~INR15.7b, and this led to AUM growth of 25% YoY/ 6% QoQ to ~INR159b. BT-OUT rate (annualized) in 4QFY26 declined to ~6.4% (PQ: ~6.6% and PY: ~7.5%).

* We expect HOMEFIRST to deliver an AUM CAGR of ~23% for FY26-28E.

Reported NIM contracts ~10bp QoQ, but spreads remain stable

* Reported yields declined ~20bp QoQ to ~13.1%. The reported CoF also declined ~20bp QoQ to ~7.9%. Overall spreads remained stable QoQ at 5.2%.

* Incremental CoF and origination yield in 4QFY26 stood at 7.6% (PQ: 7.7%) and 13% (PQ: 13.1%), respectively. Reported NIM declined ~10bp QoQ to 5.9%. We model a NIM (calc.) of ~6.1%/~5.8% for FY27E/FY28E.

Highlights from the management commentary

* A calibrated branch expansion plan is in place, with ~30-40 branches planned to be added during the year, along with a focus on improving productivity across the network. Branch expansion will follow a dual approach of entering new geographies while deepening presence in existing high-potential cities through network strengthening.

* The company has not observed any material impact on asset quality from geopolitical tensions in the Middle East.

Valuation and view

* HOMEFIRST delivered a healthy 4QFY26 performance, supported by healthy AUM and disbursement growth. The management expressed confidence in maintaining spreads, even as yields witnessed some compression during the period. Asset quality is also expected to remain stable, with no observable impact from the Middle East conflict, aided by tighter underwriting standards and stronger collection efforts. Overall, the operating environment appears benign, with execution discipline and credit quality trends remaining well anchored, heading into the next phase of growth.

* The stock currently trades at ~2.6x FY27E P/B. We estimate a CAGR of ~23%/~18% in AUM/PAT over FY26-28E and an RoA/RoE of ~3.7%/14.2% in FY28E. Reiterate BUY with a TP of INR1,425 (based on 2.6x FY28E BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412