Buy Rubicon Research Ltd for the Target Rs. 780 by Motilal Oswal Financial Services Ltd

Outperformance across metrics; stellar start to the post-IPO phase

Conservative upgrade; continued delivery to drive valuation re-rating

* Rubicon Research (Rubicon) delivered better-than-expected performance, with a 7%/18%/21% beat on revenue/EBITDA/PAT for the quarter. Improved revenue from new launches and steady traction in existing products led to strong operating leverage for the quarter.

* Rubicon started its post-IPO journey on a strong note, reporting robust YoY revenue growth and enhanced profitability, with annualized pre-tax ROCE reaching 36% for the 12M ending Sep’25.

* Rubicon has further strengthened its R&D team to 190 scientists at the end of 1HFY26 from 143 at the end of FY24. With a widened focus on product development in the CNS segment, R&D spend continued to rise, reaching INR818m in 1HFY26 vs INR700m/INR1.3b in 2QFY25/FY25.

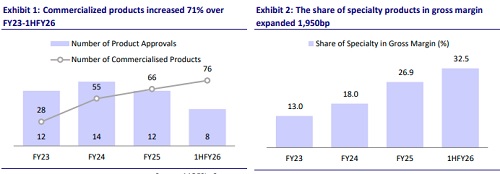

* Rubicon commercialized six products in 2QFY26 and sustained momentum in its existing products, achieving a commercialization rate of 93% in 2QFY26.

* Despite 2QFY26 results materially surpassing our estimates, we raise our earnings estimate by 4%/3%/2% for FY26/FY27/FY28, as we await consistency in performance going forward. Even with this earnings upgrade, we expect a phenomenal 44% earnings CAGR over FY25-28.

* We value Rubicon at 35x 12M forward earnings to arrive at a TP of INR780. We remain positive on Rubicon on the back of: a) a leading R&D turnover, b) consistent compliance, and c) focused product selection driving development, manufacturing, and conversion to a commercialization rate exceeding 90%. Reiterate BUY.

Strong commercialization drives revenue; outsourcing impact outweighed by operating leverage

* 2QFY26 revenue grew 39.2% YoY to INR4.1b (our est: INR3.85b).

* Gross margin contracted 400bp YoY to 69%, driven by higher outsourcing.

* However, EBITDA margin expanded 210bp YoY to 22.9% (our est: 20.8%), driven by better operational efficiency (other expense/employee expense down 410bp/190bp YoY as % of sales).

* EBITDA grew 53% YoY to INR943m (our est: INR801m).

* Interestingly, R&D expense increased 120bp YoY as a % of sales to 11.2% for the quarter (INR463m on an absolute basis).

* PAT grew 56% YoY to INR539m (our estimate: INR443m).

* Revenue/EBITDA/PAT grew 25%/42%/62% YoY in 1HFY26 to INR7.6b/1.7b/1.0b.

Highlights from the management commentary

* Rubicon guided for annual R&D spend to be 10-11% of sales for the next 4-5 years.

*EBITDA margin is expected to sustain going forward. This is after considering additional opex related to the Alkem plant.

* The Pithampur plant is expected to be operational from mid-CY26 onwards.

* Over FY20-1HFY26, equity raise of INR1.1b, debt raise of INR4.7b, and internal accruals of INR12.3b have been utilized for R&D (INR6.5b), capex (INR5b), and working capital requirements (INR6.7b).

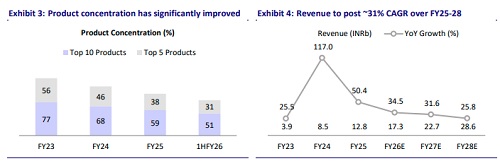

* The top 5/10 products formed 30%/51% of revenue in 2QFY26. Contribution from the top 10 products is expected to remain sub-50% over the medium term.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412