Neutral United Foodbrands Ltd for the Target Rs 425 by Motilal Oswal Financial Services Ltd

Strong SSSG recovery; margin guidance appears aggressive

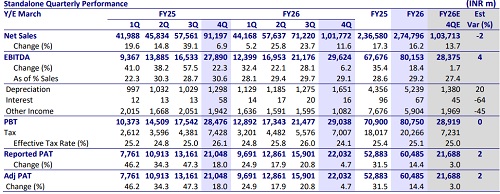

* United Foodbrands (UFBL) reported consolidated revenue growth of 23% YoY to INR3.6b in 4QFY26 (beat), led by 14% SSSG (est. 8.4%, 8% in 3Q). Dine-in revenue registered 21% YoY growth (+43% volume), and delivery revenue rose 32% YoY. BBQ India’s revenue rose 22% YoY to INR2.8b, driven by a 16.7% SSSG and 8% YoY store expansion. BBQ India added 8 stores to 207 stores in 4Q.

* BBQ International’s revenue grew 27% YoY to INR336m with a 5.5% SSSG, while Premium CDR revenue increased 23% YoY to INR489m, supported by 40% YoY store additions and 7% SSSG.

* Gross margin contracted 410bp YoY to 62.8% due to lower realizations from new stores and value offerings. RoM Pre-Ind AS margin expanded 150bp YoY to 11.6% on operating leverage. RoM expanded 40% YoY.

* Consolidated GM contracted 300bp YoY to 65.5%, as India GM witnessed a 400bp dip to 62.8%, driven by lower realizations from new stores and value offering. RoM for India was at 11.6% (up 150bp YoY), supported by healthy topline growth. Consolidated EBITDA margin (Pre-Ind AS) contracted 100bp YoY to 5.5% due to higher investments in backend capabilities and digital infrastructure.

* Management expects 100-200bp GM recovery in FY27 despite rising cost inflation. Moreover, it has guided for a 9-10% EBITDA Pre-Ind AS margin vs. 5.4% in FY26 and 7.4% in FY27. Given the overall cost inflation and value offering by the company, we consider such margin guidance aggressive. We model EBITDA Pre Ind AS margin of 7% for FY27 and 7.5% for FY28. The growth achieved over the last 2 quarters came after a slight margin hit, and achieving both growth and margin expansion in this environment could be a challenge for the company. Given the volatile execution in the past, we reiterate our Neutral rating with a TP of INR425.

SSSG up 14%; operationally in-line performance

* Strong revenue delivery: Consolidated sales grew 23% YoY to INR3.6b (est. INR 3.4b) in 4QFY26. Same store sales rose 14.4% in 4QFY26 (est. 8.4), led by transaction growth. Dine-in channel (82% of sales) grew 21% YoY to INR3.0b. Delivery channel (18% of sales) rose 32% YoY to INR0.6b.

* Digital KPIs: Cumulative app downloads stood at 9.1m in 4QFY26 vs 7.4m in 4QFY25. Own digital asset contribution was at 60.9% vs. 33.6% in 4QFY25.

* Store addition continues; plans to achieve 300 stores by FY27: The company has added 13 stores, leading to a total store count of 262. Of this, BBQN has 207 stores, international BBQN has 13 stores, and Toscano and Salt has 42 stores. Total metro and tier-1 accounted for 207 stores and tier 2/3 accounted for 55 stores in 4QFY26. The company plans to achieve 300 stores by FY27.

* Contraction in margins: Consolidated GM contracted 300bp YoY to 65.5%. (est. 67%) . EBITDA rose 2% YoY to INR544m (est. INR568m). EBITDA margin contracted 310bp YoY to 15.1% (est. 16.6%). EBITDA (Pre-Ind AS) increased 5% YoY to INR199m in 4QFY26, and margin contracted 100bp YoY to 5.5%. RoM Pre-Ind As rose 23% YoY, and margin remained flat YoY at 12.6%.

* In FY26, net sales grew 9%, while SSSG stood at 5%. EBITDA Pre-Ind As declined 20% YoY. EBITDA Post-Ind AS dipped 2% YoY.

Valuation and view

* We raise our EBITDA estimates by 12% for FY27 and 7% for FY28 on better delivery of revenue in 4QFY26.

* Management expects 100-200bp GM recovery in FY27 despite rising cost inflation. Moreover, it has guided for a 9-10% EBITDA Pre-Ind AS margin vs. 5.4% in FY26 and 7.4% in FY27. Given the overall cost inflation and value offering by the company, we consider such margin guidance aggressive. We model EBITDA Pre-Ind AS margin of 7% for FY27 and 7.5% for FY28. The growth achieved over the last two quarters came after a slight margin hit, and achieving both growth and margin expansion in this environment could be a challenge for the company. Given the volatile execution in the past, we reiterate our Neutral rating with a TP of INR425 (15x Mar’28E Pre-Ind AS EV/EBITDA).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412