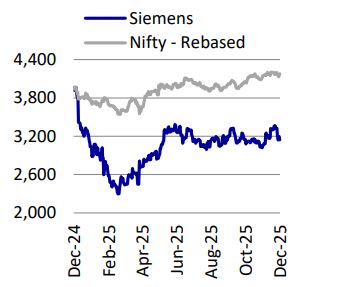

Buy Siemens Ltd for the Target Rs. 3,250 by Motilal Oswal Financial Services Ltd

Growing selectively

Siemens (SIEM) in its analyst meet highlighted healthy growth traction in the smart infrastructure segment and the possibility of improved revenue growth and margin profile for the mobility segment as locomotive delivery commences. Uncertainty persists about the timing of orders from the government, mainly railways, and private capex revival. We cut our estimates by 1%/4%/4% in 18MFY26E/12MFY27E/12MFY28E to factor in lower margin in digital industries. We expect revenue/EBITDA/PAT to grow at a CAGR of 11%/13%/8% over FY24 (Sep-ending)-FY28 (Mar-ending). The stock is currently trading at 50.4x/42.2x P/E on FY27/28E earnings. We reiterate our Neutral rating on the stock with a revised TP of INR3,250, (from INR3,350 earlier), based on 45x Dec’27E earnings. A broad-based capex revival and margin improvement will be the key drivers for earnings and valuation re-rating.

Key takeaways from analyst meet

Smart infrastructure well placed to sustain double-digit growth

The smart infrastructure segment delivered strong growth in 12MFY25, with revenue up 14% YoY to INR92b and orders up 15% YoY to INR103b. Order growth was driven by power utilities, semiconductors, batteries and EVs, while a strong backlog supported revenue and helped to maintain healthy EBIT margins despite higher competition. The business is focused on T&D, data centers, commercial buildings, and the company provides switchgear, substation automation, grid software, building automation solutions, etc. to clients. The company expects these end-markets to continue to grow at 8-10% CAGR over FY25-30. We expect this segment to get the benefit of demand growth, capacity expansion, and potential M&A. It is already localized to an extent of 60% and further localization and increased traction of C&S in export markets can help to improve margins going forward.

Mobility division to benefit from locomotive deliveries and operating leverage

Mobility segment scaled up well in 12MFY25, with revenue up 15% YoY to INR33b and orders up 49% YoY to INR50b, supported by major wins in highspeed rail and metro signaling, along with continued locomotive ramp-up with the first prototype delivered. With a broader portfolio across rolling stock, propulsion and signaling, particularly Kavach, the business is well placed to benefit from rail and metro capex as and when ordering starts ramping up. The company expects the mobility addressable market to grow at around 10% CAGR over FY25-30. It has already submitted the locomotive prototype and as it is approved, the company would begin the locomotive deliveries in line with the original schedule (Exhibit 8). This should drive revenue growth and margin expansion for the segment.

Digital industries segment may continue to see low margins

The segment delivered 12MFY25 orders of INR38b, up 13% YoY, while revenue declined 7% YoY to INR37b. Orders were weak at the start of 12MFY25 but recovered strongly with 34% growth in 4Q, led by Chemicals, Pharma and Metals. Revenue was limited by a low opening backlog and soft private capex. The business offers automation and software across key manufacturing verticals, and management plans to run a unified, vertical?focused sales model, strengthen the partner network and grow higher?margin services from the installed base. This segment mainly focuses on private capex and earns 40-50% of revenue from industries such as machine building, metals and automotive and the rest from pharmaceuticals, cement, chemicals, etc. These segments have grown at 5-8% and future growth may also be in a similar range. Due to lower-than-expected demand and higher import content, management has guided for a margin range of 6-8% from the segment and an additional buffer can come once service share improves. We thus reduce our margin estimates for this segment.

Low-voltage motors divestment to Innomotics India

SIEM has approved a slump sale of its low?voltage motors business to Innomotics India for INR22b (50.5x FY25 EBITDA), at the same enterprise value at which it had earlier proposed in FY23 to sell the business to Siemens AG. The transaction is expected to close in Jun’26, subject to requisite regulatory and customary approvals. The exit removes a small, low?return, non?core business, allowing management to focus more on its core operations.

Our outlook going forward

The company’s strong order inflows in 12MFY25 provide good visibility for revenue growth. We believe that going forward, growth will be driven more by the smart infrastructure segment and mobility, while the digital industries segment will remain impacted by weak private capex growth. We expect margin improvement in smart infrastructure and mobility as localization and operating leverage benefits play out. Uncertainties exist about the timing of ordering from railways as well as from private capex.

Financial outlook and view

We cut our estimates by 1%/4%/4% in 18MFY26E/12MFY27E/12MFY28E to factor in lower margin in digital industries. We expect revenue/EBITDA/PAT to grow at a CAGR of 11%/13%/8% over FY24 (Sep-ending)-FY28 (Mar-ending). The stock is currently trading at 50.4x/42.2x P/E on FY27/28E earnings. We reiterate our Neutral rating on the stock with a revised TP of INR3,250, (from INR3,350 earlier), based on 45x Dec’27E earnings. A broad-based capex revival and margin improvement will be the key drivers for earnings and valuation re-rating.

Key risks and concerns

Key risks: 1) slowdown in order inflows from key government-focused segments, 2) aggression in bids to procure large-sized projects would adversely impact margins, and 3) related-party transactions with parent group entities at lower-than-market valuations to weigh on the stock performance.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412