Buy Cummins India Ltd for the Target Rs.5,500 by Motilal Oswal Financial Services Ltd

Demand environment remains strong

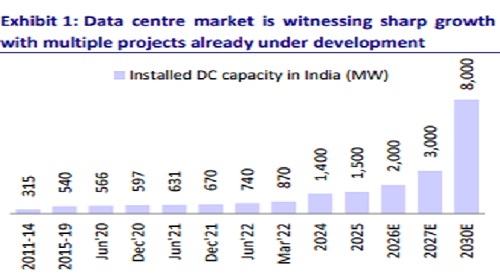

Key takeaways from our interaction with the management We reiterate our positive stance on Cummins India (KKC) post our recent meeting with the management. The company continues to benefit from: 1) healthy demand momentum in powergen, coupled with strong growth opportunities from fast-growing data centre market, 2) improving demand for industrial segment, which was impacted in 9MFY26 due to slower capex, 3) higher installed base for distribution, and 4) improving trends in exports. Cummins has already localized 70-80% of CPCB 4+ genset requirements and can easily expand capacity in order to cater to increased demand requirements. We revise our estimates upwards by 5%/7% for FY27/28 to bake in better demand for HHP, distribution, and correspondingly better margins on improved product mix. We reiterate BUY with a revised TP of INR5,500 based on 45x Mar’28 earnings. We revise our multiple upward from 42x to 45x, factoring in the stronger data centre demand outlook and the company’s ability to capitalize on it, supported by its market leadership in the segment

Powergen market demand remains strong

KKC’s powergen segment demand remains strong across kVA ranges. Below 750kVA ranges, demand is being driven by infrastructure, real estate, and manufacturing, while for HHP, demand drivers remain strong across data centres, hotels, and hospitals. The data centre market demand is being driven by colocation as well as hyperscalers. The company expects this demand momentum for product as well as project businesses to sustain going forward, supported by increasing investments toward data centres. Project business may continue to remain lumpy for the initial few years, as the company recognizes project revenues only at the time of installation. The company is continuously evaluating opportunities with its clients and is hopeful of materializing more additions as Indian data center market matures over time. The ordering-todelivery timeline is typically two years, and hence, we believe growth for company in the HHP segment can continue to remain strong for the next few years as the DC market grows. We revise our powergen revenue estimates upwards and expect this segment’s revenues to clock a 17% CAGR over FY25-28.

Localization benefits can further play out with scale

The company indicated that localization for any engine depends on economies of scale. For K38 and K50 engines, company has been able to localize fully due to higher demand for these in both domestic and international markets. It is also enhancing capacity to increase per-day output for these. For new CPCB 4+ gensets too, KKC has been able to achieve 70-80% localization. For data centreled requirements, most demand comes for QSK60, QSK78, and QSK95 – of which QSK60 is made by the company, while QSK78 and QSK95 are imported. Non-hyperscaler requirements mostly come for QSK60, while hyperscalers require QSK78 and QSK95, which cost around INR50-110m per unit. Company plans to localize these once it sees strong sustainable demand and market for them in India. Players like Caterpillar and MTU do have QSK78 and QSK95 engines, but KKC is ahead of competition as it provides a value-added service to the customers, services, engineers on board, extended AMCs, a strong distribution network, and easier availability of parts.

Industrial business outlook positive on increased tendering activity

Industrial demand remains strong in defence and marine, while mining remains relatively subdued. For railways, the company has supplied two hotel load converters and given demos for 3T technology for rail electrification, which will run on Vande Bharat trains. Defence demand remains strong, supported by higher budgetary allocations and indigenization efforts, particularly in marine defence, where engine sales are complemented by multi-year parts and service commitments. Marine activity has also improved under port modernization and Sagarmala initiatives, benefiting both commercial and government shipbuilding programs. Industrial segment’s 9MFY26 performance was impacted by prolonged monsoons that slowed construction activity, but execution has begun normalizing with a gradual pickup. We, thus, increase our industrial segment’s estimates to grow at an 11% CAGR over FY25-28

Distribution segment backed by expanding installed base

The distribution segment remains a high-growth business, driven by: 1) spare parts, 2) warranty and annual maintenance contracts, and 3) third-party components along with rebuild and service solutions. Spare parts contribute the largest share, supported by a growing installed base, while multi-year maintenance contracts ensure recurring income and customer stickiness. Management highlighted that CPCB-IV+ has inbuilt telematics and fault code monitoring for predictive maintenance, and these are up for warranty renewal starting from July’26. Thirdly, RECD (retrofit emission control devices) are being deployed for older CPCB-II engines in emission sensitive regions to ensure regulatory compliance. The company operates through more than 200 customer care touchpoints, around 480 service response locations, and over 3,500 service engineers, enabling strong field penetration and uptime assurance. Management sees sustained growth in the distribution business with a widening asset base and increasing rebuild opportunities as engines age. We expect segment revenue to expand at a CAGR of 23% over FY25-28.

Exports to normalize in coming quarters

For exports, while there was moderation in certain regions during the previous quarter due to inventory adjustments by channel partners, management expects gradual normalization beginning from 4QFY26 onwards as stocking levels stabilize. Demand patterns are region-specific, with low horsepower demand coming mostly from Turkey, Chile, and Mexico, while mid-HP demand has been fairly consistent from the Middle East and Africa. HHP demand has particularly come from European markets. The export strategy is aligned with KKC’s global supply chain architecture, where India serves specific geographies based on product capability and cost competitiveness. Over the medium term, export growth will be linked to regional infrastructure demand and order visibility. We expect exports to expand at a CAGR of 16% over FY25-28.

BESS complementary to powergen Battery energy storage systems (BESS) represent an emerging opportunity, positioned as a complementary solution to diesel gensets rather than a replacement. The company has completed demonstrations across more than 25 tates covering over 4,500 kilometres and received over 180+ customer inquiries. It offers containerized 100 to 300 kilowatt solutions that can provide 2-4 hours of backup and help customers manage peak or high tariff periods by storing grid or renewable energy for later use. Target segments include residential complexes, healthcare, water treatment, remote industrial sites, mining, and EV charging infrastructure. The product is currently imported and remains in the solutionizing stage, with management indicating gradual scaling as energy economics improve.

KKC and CTIL operating framework

KKC primarily caters to the off-highway segment, including industrial, powergen, railways, marine, mining, and defence applications, with manufacturing scale largely in the 40-60 litre engine range, whereas Cummins Technologies India Private Limited (CTIL) operates in the on-highway domain and manufactures engines and components suited for on-highway applications, including certain litre platforms, such as the 23 litre engine. Management stated that while both entities are not comparable in terms of business mix, they both function under distinct products and end-markets within the broader Cummins group framework.

Valuation and recommendation

The stock currently trades at 56.3x/47.7x/40.5x on FY26/FY27/FY28E EPS. We reiterate our BUY rating on the stock with a revised TP of INR5,500 (based on 45x Mar’28E earnings). Our revised multiple from 42x earlier to 45x takes into account the improved demand scenario for data centres and the company’s ability to benefit from this, owing to its market leadership in this segment.

Key risks and concerns

Key risks to our recommendation would come from lower-than-expected demand for key segments, higher commodity prices, intensified competition, and lowerthan-expected recovery in exports.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041