Buy Tech Mahindra Ltd For Target Rs.1,660 by Prabhudas Liladhar Capital Ltd

Strong Margin Improvement, Await Revenue Acceleration

Quick Pointers

* Margin improvement trajectory continues

* Deal wins of US$ 1.07 bn, 2nd straight qtr, of USD 1bn+ TCV

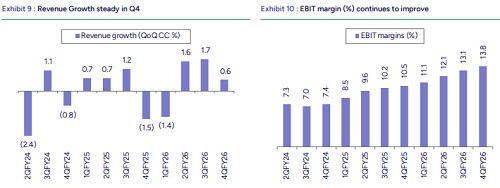

The revenue growth (+0.6% CC QoQ) exceeded our estimates (+0.1% CC QoQ), aided by Comviva seasonality. The growth performance was balanced even beyond communications vertical, ex-Comm USD growth was 0.5% QoQ. The management also delved into three-year strategic initiatives (undertook in FY24), while mapping the progress on stabilizing growth and improving margins in FY26. On successfully achieving the milestone, the company is now gearing up to deliver industry average growth and achieve the last mile of margin improvement in FY27E. The earlier efforts of integrating portfolio companies, scaling the must-have accounts, hiring senior leaders and expanding high-margin service lines are largely concluded in FY26. These initiatives have resulted in shaping multi-tower quality deals and growing engagements with potential accounts. Additionally, the overdependency on Communications seems to have reduced largely with senior domain experts hiring within key sub-verticals, further derisking the dominance of Communications. The FY26 deal TCV looks encouraging at USD3.8b (+41.5% YoY), which is coming over and above 42.5% YoY TCV growth delivered in FY25. We believe the restructuring exercise has largely calibrated margins to a comfort band, now it requires paddling more on the revenue conversions. On margins, we believe since operational stability has achieved, the incremental engagement on FP contracts would an additional support to margin levers beyond the operating leverage achieving through growth acceleration in FY27E. We are keeping our revenue growth unchanged at +4.8%/5.8% CC YoY while improving margins by 20bps each to 14.5% and 15.0% YoY in FY27E/FY28E. We assign 19x to arrive at a TP of Rs. 1,660. Retain BUY.

Project Helix: Management highlighted Project Helix as a core AI pillar, integrating human and agentic AI capabilities to deliver scalable, end-to-end solutions, driving modernization and differentiated AI-led services.

FY27 growth strategy: TechM sees FY27 as a transition year amid macro and AI-led disruption, while focusing on AI (Project Helix), large deals, and key account mining to drive growth; the strategy also emphasizes GCC/nearshore expansion and domain-led offerings to support margins.

Growth in focused metrics: TechM delivered solid FY26 execution with strong deal wins (US$3.8bn, +41.6% YoY), improved large account traction and geographic mix, alongside better margin discipline and talent metrics; notably, ~95% of key clients are now infused with AI, highlighting progress on its AI-led transformation.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271