The Economy Observer :Fiscal monthly: Center and states maintain strong capex growth by Motilal Oswal Financial Services Ltd

Center’s finances (Jan’26 and 10MFY26):

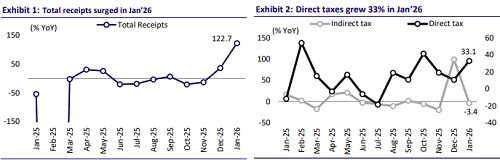

* Total receipts increased sharply in Jan’26, supported by higher tax collections as well as an improvement in non-debt capital receipts. Non-debt capital receipts saw a strong rise compared to last year, reflecting better realizations from disinvestment (INR93b in Jan’26; INR371.6b in 10MFY26, 312% YoY). The bulk of the proceeds has come from minority stake sales in CPSEs, such as BHEL, Mazagon Dock, Bank of Maharashtra, IRFC, and Indian Overseas Bank. The transactions have largely been executed through the Offer for Sale (OFS) route.

* Gross tax revenue grew at a healthy pace in Jan’26, driven by strong expansion in direct taxes (33% YoY in Jan’26). Corporate tax collections rose sharply on a favorable base (180.8% YoY in Jan’26), while income tax posted steady growth of 12.6% YoY. In contrast, indirect taxes saw a mild contraction (-3.4% YoY in Jan’26), largely due to weaker GST collections .

* On the expenditure side, total spending declined 8.5% YoY in Jan’26, led by contraction in both revex (-4.2% YoY) as well as capex (-24.5% YoY). The decline in capex during the month needs to be viewed in the context of front-loaded spending earlier in the fiscal year. On a YTD basis, capex continues to grow at a healthy double-digit pace (11.2% YoY;). Although overall capital expenditure declined in Jan’26, spending continued in key priority areas. Transfers to states remained significant (37% of total capex in Jan’26), and allocations toward Defense, Railways, and Road Transport & Highways indicate that core infrastructure and strategic sectors continued to receive support during the month.

* As a result of restrained spending and better direct tax performance, the fiscal deficit narrowed sharply by 50.8% YoY in Jan’26.

* On a 10MFY26 basis, the Centre’s revenues remain healthy. Gross tax revenue has grown 8.6% YoY in 10MFY26, led by steady growth in both direct and indirect taxes. Non-tax revenue has also risen strongly. Overall, total receipts are up 12.8% YoY and have achieved about 79.5% of REs in 10MFY26.

* Expenditure growth has been contained at 3.4% YoY. Revenue spending has increased only marginally, while capital expenditure has grown at a strong pace of 11.2% YoY in 10MFY26. About 76.9% of the full-year capex target (REs) has already been utilized.

* The fiscal deficit stands at around 63% of the annual target. This suggests that the Center remains on track to meet its consolidation goal while maintaining a capex push . In the context of the updated nominal GDP number of INR345t as against INR357t previously, the fiscal deficit target for FY26 is revised to 4.5% from the earlier level of 4.4%.

Finances of 22 states for Jan’26 and 10MFY26:

* For the 22 states combined, Jan’26 revenue was mixed. Total receipts increased compared to last year, but revenue receipts declined mainly due to a sharp drop in states’ share of Union taxes. Tax revenue contracted 14.9% YoY in Jan’26, although stamp duties and state excise collections remained strong.

* On the expenditure side, total spending rose 11.5% YoY in Jan’26, driven primarily by a strong pickup in capital expenditure (23.5% YoY in Jan’26), while revenue expenditure rose at a more moderate pace.

* In 10MFY26, states’ finances show steady growth. Total receipts have increased 9.7% YoY, while total expenditure has risen 9.4% YoY, keeping the overall fiscal position broadly stable.

* Revenue expenditure has grown broadly in line with receipts. In contrast, capital expenditure has increased 17.2% YoY in 10MFY26, highlighting the continued infrastructure push at the state level. However, capex utilization stands at only 52.7% of BEs, suggesting likely acceleration in spending in Feb and Mar, the final quarter.

* GST collections in Feb’26: Gross GST collections stood at INR1.84t in Feb’26, registering healthy growth of 8.6% YoY, on a low base. This was primarily led by imported GST collections, which grew 14.7% YoY. Cumulatively, GST collections in FY26 have reached INR20.3t against the FY26BE of INR24.5t, thus reaching 83% of the full-year target, indicating that GST revenues are broadly on track going into the last month of the fiscal year

Outlook:

* Overall, the combined fiscal stance of the Centre and states remains growth supportive. The Centre has maintained strong YTD capital expenditure growth despite a softer January reading, while states are also expanding capex at a healthy pace. Total states (INR5.2t) + center capex (INR8.4t) stood at INR13.6t in 10MFY26, growing 12.4% YoY. Fiscal consolidation is progressing through controlled revenue spending rather than cuts to productive capital outlays.

* On the disinvestment front, the government remains confident about its roadmap. According to the DIPAM Secretary, the combined disinvestment and asset monetization target of INR800b for FY27 is ambitious but achievable. The strategy includes greater use of OFS and QIP routes, along with efforts to unlock value from PSU land assets through structures such as REITs.

* A key transaction in focus is the strategic sale of IDBI Bank, which has progressed to an advanced stage. Technical and financial bids have been invited, and further clarity on the outcome is expected before the end of FY26, subject to bid evaluation and regulatory approvals. This marks an important step beyond incremental stake dilution toward a full strategic divestment.

* The key watchpoint for the remainder of the year remains revenue collection momentum. However, with capex growth intact and disinvestment providing supplementary fiscal support, the public investment cycle continues to underpin growth.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412