Buy Rural Electrification Corp. Ltd For Target Rs. 440 Motilal Oswal Financial services Ltd

PPoP in line; earnings miss driven by higher credit costs

Loan growth muted at 3% YoY; PCR on standard assets rises ~13bp QoQ

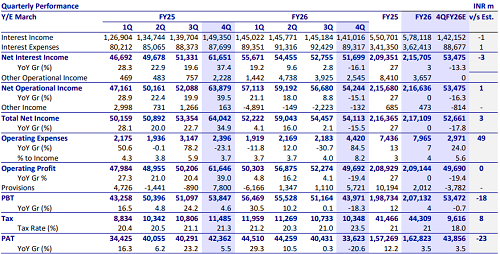

* Rural Electrification Corp’s (RECL) 4QFY26 PAT declined ~21% YoY to INR33.6b (23% miss). PAT for FY26 grew ~3% YoY to ~INR163b. NII in 4QFY26 declined ~16% YoY to ~INR51.7b (in line). Other income was flat YoY at INR2.4b. This included fee and commission income of INR2.5b (PQ: INR3.9b and PY: INR2.2b).

* Opex grew ~84% YoY to ~INR4.4b, and cost-income ratio rose to ~6.7% (PQ: 3.2% and PY: 3.1%). PPoP declined ~19% YoY to INR49.7b (in line). PPoP for FY26 remained flat YoY at ~INR209b.

* Provisions rose to INR5.7b (vs. est. provision writebacks of INR3.8b). This translated into annualized credit costs of 10bp (PY: 14bp and PQ: 2bp).

* RECL declared a final dividend of ~INR1.55/share. Including interim dividends, the total dividend for FY26 stood at INR18.55/share.

Pressure on yields, but spreads resilient

* Yields (calc.) declined ~30bp QoQ to ~9.6%, while CoB (calc.) declined ~30bp QoQ to ~7.1%, resulting in spreads (calc.) remaining stable at ~2.56%.

* Reported NIM for FY26 declined ~9bp to ~3.43% (9M: 3.52%). NIMs (calc.) declined ~10bp QoQ to 3.5% in 4QFY26. We expect RECL to maintain NIM of ~3.7% over FY27-28E, supported by the declining CoF.

Loan growth muted; renewable portfolio drives momentum

* Loan book stood at INR5.84t, growing 3% YoY and remaining flat QoQ. Repayments during the quarter declined sequentially to ~30% (PQ: 34.6% and PY: 31%). Renewable loan book grew 30% YoY to INR753b.

* Disbursements in 4QFY26 were weak and remained flat YoY at INR457b. FY26 disbursements (excluding RBPF) grew 28% YoY to INR1.46t.

* We expect RECL to deliver an AUM CAGR of ~11% over FY26-28.

Asset quality improves; RECL increases PCR on standard assets

* GS3 and NS3 declined ~70bp/~10bp QoQ to ~0.24% and 0.12%, respectively. PCR on Stage 3 stood at ~51% (PQ: 77%). Standard asset (Stage 1 and 2) provisions rose ~13bp QoQ to 1.06% (PQ: 0.93%).

* RECL wrote off ~INR12.9b related to Sinnar Thermal Power after adjusting cash recoveries of INR10.4b and reversed ECL provisions of INR5.7b. The company has also fully recovered INR138m from Bhavnagar Biomass Power Projects Private Ltd, along with a reversal of ECL provisions of INR27.5m. Moreover, the company took technical write-offs on five loan accounts, with total exposure of ~INR14b. These loan assets were earlier classified as Stage 3 with 100% provision cover.

* We model RECL’s credit costs to remain benign at ~20bp over FY27-FY28E.

Valuation and view

* RECL reported a subdued quarter, with the loan book exhibiting a modest growth of ~3% YoY. Disbursements continued to remain weak (flat YoY), and repayments moderated sequentially in 4QFY26. A decline in yields was offset by lower funding costs, which helped keep spreads stable. Asset quality improved further, with GNPA declining to ~0.2% as of Mar’26.

* RECL trades at 1x FY27E P/ABV, which is attractive. However, weak loan growth and pressure on margins remain key monitorables. We cut our PAT estimates by ~9%/~11% for FY27/ FY28 to account for lower margins and higher credit costs, and model a CAGR of 12%/11%/5% in disbursement/loans/PAT over FY26-28E. We expect RECL to deliver a RoA/RoE of 2.4%/18% in FY28E. Reiterate BUY with a TP of INR440 (premised on 1.1x FY28E BVPS).

* Key risks: 1) continued weak loan growth; 2) contraction in spreads/margins amid high competition.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412