Neutral Eris Lifesciences Ltd for the Target Rs1,435 by Motilal Oswal Financial Services Ltd

Below-par delivery; Semaglutide market share gain offers comfort Regulatory resolution and Semaglutide ramp up key monitorable

* Eris Lifesciences (ERIS) posted lower-than-expected revenue/EBITDA (9%/ 5% miss) in 4QFY26. Regulatory delay for product approvals and reduced business outlook for certain products impacted the performance in 4QFY26.

* Having said this, Eris has gained considerable market share in terms of value/units/prescriptions (Rx) for Semaglutide post its launch in Mar’26. Management has further plans to launch a Pen version as well as an obesity SKU to have a comprehensive offering. This would be further supported by in-house manufacturing.

* International business prospects have been affected to some extent due to observations from the EU regulatory agency and supply chain disruption due to political turmoil.

* We largely maintain our estimates for FY27/FY28. We value ERIS at 25x 12M forward earnings to arrive at our TP of INR1,435.

* ERIS is implementing efforts to outperform India pharma market by enhanced marketing efforts towards newer introductions. The base business growth, particularly in the oral anti-diabetes category, remains under check. ERIS also continues to build the CDMO orderbook in oral as well as injectable dosages. It is working to resolve the issues highlighted by the regulatory agency at the earliest. On the overall basis, we build 13%/15%/29% revenue/EBITDA/PAT CAGR over FY26-28. The current valuation adequately factors the earnings upside. Reiterate Neutral.

Product mix impact offset by better operating leverage

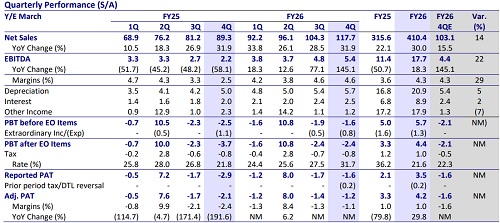

* ERIS 4QFY26 revenues grew 7.3% YoY to INR7.6b (vs our est: INR8.3b).

* Domestic Branded Formulation revenue grew 12% YoY to INR6.7b.

* International business revenue decline 8% YoY to INR860m.

* Gross margin contracted 40bp YoY to 75.5%.

* However, EBITDA margin expanded 40bps YoY to ~36.2% (our est. 34.7%).

* EBITDA increased by 8.4% YoY to INR2.7b (vs our estimate: INR2.9b)

* Adj. PAT increased by 34.4% YoY to INR1.3b (vs our estimate: INR1.2b).

* For FY26, Revenue/EBITDA/PAT grew 8.1%/10.1%/35.1% YoY.

Valuation and view

* We largely maintain our estimates for FY27/FY28. We value ERIS at 25x 12M forward earnings to arrive at our TP of INR1,435.

* ERIS is implementing efforts to outperform India pharma market by enhanced marketing efforts towards newer introductions. The base business growth, particularly in the oral anti-diabetes category, remains under check. ERIS also continues to build the CDMO orderbook in oral as well as injectable dosages. It is working to resolve the issues highlighted by the regulatory agency at the earliest. On the overall basis, we build 13%/15%/29% revenue/EBITDA/PAT CAGR over FY26-28. The current valuation adequately factors the earnings upside. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412