Buy PI Industries Ltd for the Target Rs 3,500 by Motilal Oswal Financial Services Ltd

Weak CSM volume offtake weighs on performance Operating performance misses our estimate

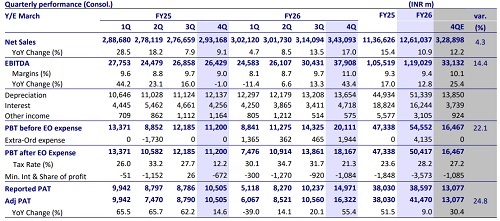

* PI Industries (PI) reported a weak quarter as revenue declined 12% YoY, primarily due to a 15% YoY dip in the CSM business, attributed to the global slowdown and cautious customer scheduling (volume declined 14% YoY). Domestic Agri also reported a revenue decline of 9% YoY, while the Pharma business grew 23% YoY. Gross margins expanded 280bp YoY due to a better product mix and operational efficiency, while lower volumes led to adverse operating leverage, thereby resulting in an overall EBITDA margin contraction of 400bp YoY.

* Going forward, we remain cautiously optimistic on FY27, supported by a strong order book, committed customer offtake plans, and the planned launch of over 5+ new molecules in the CSM business, which should accelerate growth in 2HFY27. In addition, the Biologicals pipeline and potential inorganic opportunities continue to strengthen the growth outlook.

* We largely maintain our FY27/FY28 earnings estimates and reiterate our BUY rating with a TP of INR3,500 (based on 33x FY28E EPS, i.e. a discount of ~10% to the company’s six-year historical P/E at 37x).

Adverse operating leverage contracts margins

* Revenue stood at INR15.7b (est. in line), declining 12% YoY. Agrochemicals business revenue declined 14% YoY to INR14.6b, and the Pharma business revenue rose 23% YoY to INR1b.

* EBITDA stood at INR3.4b (est. INR3.8b), declining 26% YoY. EBITDA margins contracted 400bp YoY to 21.5% (est. 24.1%); gross margins stood at 58% (up 280bp YoY); employee expenses rose 350bp YoY to 14.5%; other expenses rose 330bp YoY to 21.8% of sales.

* For FY26, Agrochemicals business revenue declined 17% to INR64b, while Pharma business revenue grew 40% to INR3b.

* EBIT margins for the Agrochemical business stood at 22.8% (down 660bp), and the Pharma business reported an operating loss of INR486m vs an operating loss of INR821m in 4QFY25. Adj. PAT declined 39% YoY to INR2.0b (est. INR2.7b).

* For FY26, EBIT margins for the agrochemical business stood at 28.0% (down 280bp), and the pharma business reported an operating loss of INR2.7b vs an operating loss of INR3b in FY25.

* For FY26, Revenue/EBITDA/Adj PAT declined 16%/22%/25% to INR67b/INR17b/INR12b.

* Gross debt stood at INR2.4b vs INR1.1b as of Mar’25. CFO stood at INR4.7b vs INR14.1b as of Mar’25.

* PAT was adjusted for a one-time labor code adjustment of INR20m

Valuation and view

* The company’s CSM business witnessed a sharp slowdown in FY26 due to weak industry demand, elevated channel inventories globally, and customers adopting a cautious just-in-time procurement strategy, resulting in a volume decline.

* Going forward, we believe growth recovery will be led by:

1) improving growth prospects in the CSM business due to faster growth in new molecules (commercialization of 20+ molecules over the last few years ), ramp up of new molecules (18-20% share), strong pipeline of 90+ molecules ( >60% in advanced stages of development)

2) robust pipeline of biological products across various development stages

3) the ramp-up of its pharma business with profitable growth.

* We expect a CAGR of 13%/16%/14% in revenue/EBITDA/adj. PAT over FY26-28. We reiterate our BUY rating with a TP of INR3,500 (based on 33x FY28E EPS, i.e. a discount of ~10% to the company’s six-year historical P/E at 37x).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412