Buy Prince Pipes and Fittings Ltd for the Target Rs 330 by Motilal Oswal Financial Services Ltd

Volume-led strong operating performance Earnings miss estimates

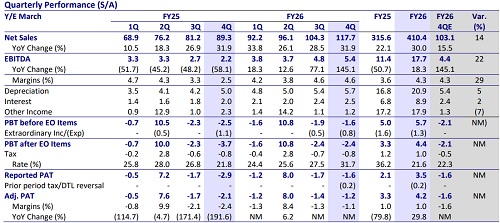

* Prince Pipes and Fittings (PRINCPIP) posted a robust quarter, driven by strong volume growth of 23% YoY, leading to operating leverage-led margin expansion of 530bp YoY. Inventory gains during the quarter were entirely passed on to distributors and channel partners to support faster inventory movement (helped reduce working capital days) and foster better relations with them, aiding market share gains (reflected in volume growth).

* With volatility persisting due to the West Asia conflict, Apr’26 witnessed inventory destocking, leading to lower volumes, while May’26 saw strong primary volume growth. FY26 witnessed healthy improvement in working capital days and liquidity, which management expects to improve further in FY27.

* Despite a miss in our 4Q estimates, we largely maintain our FY27/FY28 earnings estimate on the back of healthy volume growth (12-15%) and margin guidance (11-13%) for FY27. We value the stock at 18x FY28E EPS to arrive at our TP of INR330. Reiterate BUY.

Operating leverage and better product mix improve margins

* Consolidated revenue grew 18% YoY/48% QoQ to INR85b (est INR9.9b), while volumes increased 23%/46% YoY/QoQ to 62.2KMT. Realization declined 4% YoY, while improving 2% QoQ to INR136.7/kg, with the entire inventory gain passed on.

* Consolidated EBITDA surged 2x YoY to INR1.1b (est. INR1.4b), with an EBITDA margin of 12.9% (est. 13.7%). EBITDA/kg stood at INR17.6/kg (up 62% YoY and 2.7X QoQ). Adj. PAT (after tax) was INR561m vs. INR242m YoY (est. INR771m).

* Net working capital days improved to 45 as of Mar’26 vs. 98 as of Mar’25. This was largely led by lower inventory (down 18 days), lower receivables (down 10 days), and higher payable days (up 25 days).

* For FY26, revenue, EBITDA, and PAT grew 3%, 44%, and 73% to INR26b, INR2.3b, and INR747m, respectively. Meanwhile, volume and EBITDA/kg grew 8% and 33% to 191.2k MT and INR12.1, respectively.

Valuation and view

* FY26 ended on a strong footing, with volume-led growth improving market share. FY27 is expected to be better, supported by healthy volume growth on the back of improving demand, the ramp-up of the new Begusarai (Bihar) plant, and expansion of the bathware segment into the Southern and Eastern markets. Additionally, improving product mix and operating leverage are likely to lead to better margins for FY27.

* We expect PRINCPIP to clock an 18%/33%/66% CAGR in revenue/EBITDA/PAT over FY26-28. We value the stock at 18x FY28 EPS to arrive at our TP of INR330. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412