Buy Sirca Paints India Ltd for Target Rs.625 by Choice Institutional Equities

NDR Takeaways: A Compounding Story

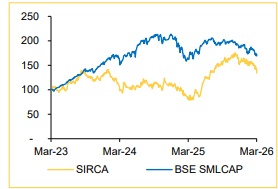

We hosted a Non-Deal Roadshow with Sirca Paints India Ltd. Management in Mumbai on March 13, 2026, with Institutional Investors, where discussions primarily focused on the wood coating industry dynamics (demand and supply trend, competitive edge and profitability expansion) and future growth prospects.

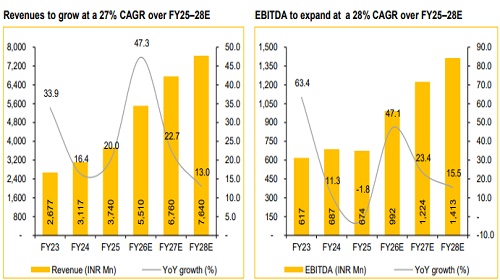

Management expects strong growth driven by capacity expansion and consolidation of the Wembley and Welcome facilities, portfolio expansion into mass wood coatings, increased domestic manufacturing of previously imported products, and structural demand from India’s growing furniture industry, supporting medium to long-term scale-up.

Valuation

We use a DCF-based approach to value SIRCA. Our base case scenario TP is INR 625/sh and the upside scenario (20–25% probability event) fair value is INR 800/sh, whereas our downside scenario (15–20% probability event) fair value is INR 360/sh.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131