Buy Coal India Ltd For Target Rs. 530 Motilal Oswal Financial services Ltd

Beat on earnings; outlook positive

* The company has retrospectively restated the FY24/25 financials following an audit-led reassessment of coal levy accounting, shifting certain levies from agent to principal basis. Due to this adjustment, the company has now added the collected cess to revenue and adjusted in other expenses. Adjustments include coal cess equalization balances, correction of capital asset misclassification, deferred tax recognition errors, and regrouping of prior-period expenses.

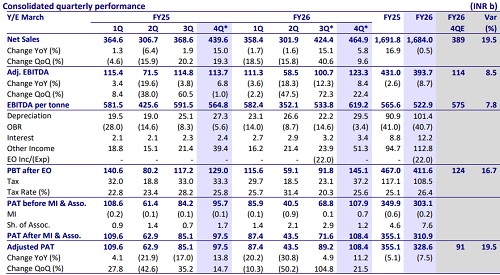

* Reported revenue for 4QFY26 stood at INR465b (+6% YoY and +10% QoQ).

* Adj. EBITDA (excluding OBR exp) stood at INR123b (+8% YoY and +22% QoQ) against our estimate of INR114b. EBITDA/t improved to INR620/t (+10% YoY and +16% QoQ) vs. our estimate of INR575/t.

* APAT came in at INR108b (+11% YoY and +22% QoQ) against our est. of INR91b during the quarter. The beat was mainly attributed to better operating profit and higher-than-expected other income of INR51b (+30% YoY and +114% QoQ) in 4QFY26.

* Production for 4QFY26 stood at 239mt (+1% YoY and +19% QoQ) and Offtake stood at 199mt (-1% YoY and +6% QoQ).

* E-auction premium for the quarter stood at 36% with volume of 28mt (~14% contribution to total sales volume) vs. 47% with volume of 22mt (~11% contribution to total sales volume) in 4QFY25.

* In FY26, revenue stood flat YoY at INR1,684b, while adj. EBITDA and APAT decline by 9% (INR394b) and 8% YoY (INR329b), respectively.

* The production volume in FY26 declined by 1% YoY to 773mt and offtake was down by 2% YoY at 747mt.

* The board recommended a final dividend of INR5.25/share, subject to approval, totaling INR26.75/share in FY26.

Valuation and view

* Coal India (COAL) delivered a decent performance, mainly supported by higher e-auction volumes (accounted for ~14% of total volumes). Premium stood at 36% in 4QFY26. We expect COAL to post a 4% volume CAGR in FY26-28E, while a higher share of e-auction volumes with better premium will support overall NSR and margins. This is expected to translate into a CAGR of 5% and 12% in revenue and EBITDA over FY26-28E, respectively.

* The company’s focus on increasing coal-washer capacity will improve its market share in domestic coking/non-coking coal. Further, management remains focused on expanding its coal mining operations, which will be funded through internal accruals.

* At CMP, the stock is trading at 5x on FY28E EV/EBITDA. We reiterate our BUY rating with a TP of INR530, valuing the stock at 6x FY28E EV/EBITDA.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)