Buy Hindustan Aeronautics Ltd for the Target Rs.5,500 by Motilal Oswal Financial Services Ltd

Tejas deliveries shifted to 2QFY27

Hindustan Aeronautics (HAL)’s 4QFY26 results were ahead of our estimates on betterthan-expected margin and other income. Despite witnessing issues in Tejas Mk1A deliveries during FY26, the company scaled up execution across ALH, AL31-FP, and RD-33 engines and platforms and grew manufacturing revenue by 30% YoY in FY26. With an order book of INR2.5t, we expect manufacturing revenues to scale up as HAL would be working on various platforms such as LCA Mk1A, LCH, Su-30 engine upgrade, Su-30, HTT40, and Dornier simultaneously in FY27. HAL is targeting 20 deliveries of the Tejas Mk1A in FY27 contingent upon receipt of engines from GE. For other platforms, too, execution ramp-up is expected to be faster as the supply chain is under control for those projects. We raise our estimates by 15%/8% to bake in slightly lower revenue and higher margin, in line with the delivery schedule of platforms. We reiterate our BUY rating with a TP of INR5,500, implying a 30x P/E two-year forward earnings. HAL continues to remain the cheapest stock in our defense coverage universe. However, re-rating is dependent upon platform deliveries, which are likely to commence from 2QFY27

Better-than-expected profitability

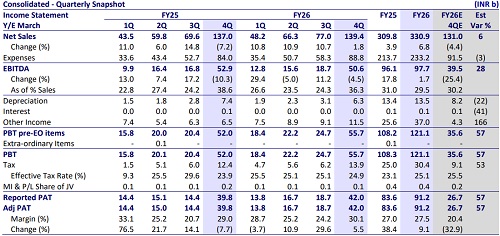

Revenue increased 2% YoY to INR139b, 6% above our estimate of INR131b. Gross margin contracted to 54.0% vs our estimate of 57.9%. However, lowerthan-expected provision made during the quarter led to a 28% beat on absolute EBITDA of INR50.6b (-5% YoY), while EBITDA margin contracted 230bp YoY to 36.3% (vs our est. of 30.2%). Aided by higher-than-expected other income, PAT at INR42b increased 6% YoY, beating our estimates by 57%. For FY26, revenue/ EBITDA/PAT increased 7%/2%/9% YoY to INR331b/98b/91b, while EBITDA margin contracted 150bp YoY to 29.5%. The company reported an order book of INR2.5t in FY26 vs ~INR1.9t last year. The increase is mainly due to the signing of major orders with the MoD for the supply of 97 additional LCA Mk1A aircraft (INR624b), six ALH CG (INR27b), and eight Dornier CG (INR219b). OCF/FCF declined 20%/18% YoY to INR109b/INR100b.

Strong order book visibility

HAL closed FY26 with an order book of INR2.5t (vs INR1.9t at the beginning of the year). The company received fresh orders worth INR970b during the year, which included manufacturing contracts worth INR697b, ROH orders worth INR265b, development orders of INR30b, and export orders of INR4b. Key contracts received during the year included 97 LCA Tejas Mk1A aircraft for the Indian Air Force, 6 ALH Mk3 helicopters for the Indian Coast Guard, and 8 Dornier-228 aircraft. Management also highlighted a strong near-term pipeline of ~INR900b over the next two years, which includes 143 ALH helicopter orders for the Indian Army and Air Force, Sukhoi upgrades, and Dornier upgrade programs. The company expects the ALH order to be the single largest contributor within the upcoming order pipeline. Management also indicated that future approvals related to AMCA production participation and other indigenous aircraft programs could further strengthen long-term order visibility.

Financial outlook

We revise our estimates upward by 15%/8% to bake in slightly lower revenue and higher margin, in line with the delivery schedule of platforms. We expect the overall revenue/EBITDA/PAT to clock a CAGR of 20%/18%/15% over FY26-28. EBITDA margin is projected to remain strong at 29.4% in FY27, while it is expected to go down slightly to 28.9% in FY28 as the share of manufacturing revenues ramps up. The stock is currently trading at 29.3x/24.4x P/E on FY27E/FY28E EPS. We reiterate our BUY rating with a TP of INR5,500, implying 30x P/E two-year forward earnings.

Key risks and concerns

Key risks would include

1) slower-than-expected finalization of large platform orders

2) further delays in deliveries of key components such as engines for the Tejas Mk1A

3) delays in payments from the MoD

4) higher involvement of the private sector.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412