Neutral Alembic Pharma Ltd for the Target Rs.725 by Motilal Oswal Financial Services Ltd

Weak acute portfolio, high investments weigh on earnings Commercial execution in Pivya and future launches critical for next phase of growth

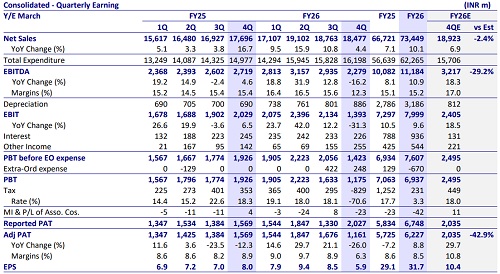

* Alembic Pharma (ALPM) reported a lower-than-expected financial performance in 4QFY26, as revenue/EBITDA/PAT came in 2%/29%/43% below our estimates. 4Q performance was affected by an inferior show in acute therapies in the domestic formulation (DF) segment, stable non-US sales and higher R&D spending.

* US sales growth in FY26 was moderate at 7% YoY (CC terms) despite a healthy pace of launches.

* Acute therapies delivered stable sales for the fourth consecutive year. The specialty segment faced challenges in FY26.

* Animal health and non-US segments maintained their robust growth momentum, offsetting the adverse impact of other business segments.

* ALPM is in the process of scaling up branded products in the US. Given the recent commercial launch, we await progress on prescription increase as well as doctor reach.

* We cut our earnings estimates by 12%/6% for FY27/FY28, factoring in

a) slower growth in branded generics in DF segment

b) higher spending on product development

c) lower operating leverage. We value ALPM at 14x 12-month forward earnings to arrive at a TP of INR725.

* ALPM ended FY26 with earnings growth of 9% YoY. We estimate a CAGR of 21%/26% in EBITDA/PAT over FY26-28, considering the scale-up in US business (on increased pace of launches), commercial success in branded business in the US, and growth momentum in non-US/API segments. However, the current valuation adequately captures any potential upside in the earnings. Maintain Neutral.

Product mix benefit more than offset by higher opex

* Sales grew 4.4% YoY to INR18.5b (our est: INR18.9b).

* Gross margin expanded 120bp YoY to 71.2%.

* EBITDA Margin contracted 310bp YoY to 12.3%, driven by higher operational cost as well as R&D expenses.

* R&D spending was INR2.1b vs. INR1.6b YoY.

* Consequently, EBITDA declined 16.2% YoY to INR2.3b (our est: INR3.2b).

* Adj. PAT fell 26% YoY to INR1.2b. (our est: INR2b).

* For FY26, revenue/EBITDA/PAT increased by 10%/11%/9% YoY to INR73b/INR11b/INR6b.

Key highlights from the management commentary

* Management expects FY27 growth of 10-15% in the US business, over 15% in ROW business, and ~10% in the API business, while the India business is expected to grow in line with market growth.

* Overall consolidated revenue growth is expected to be in the low double-digit range in FY27.

* R&D investments are likely to be around INR7.5-8.0b (~9%) in FY27.

* Capex is expected to be in the range of INR3.0-3.5b, primarily for capacity expansion, debottlenecking, and replacement capex.

* Management expects margin improvement in FY27 and reiterates its aspiration to achieve ~20% EBITDA margins over the next two to three years.

* Management expects product launches in the international business to be phased through FY27, including a few meaningful day-one launches in the first couple of quarters, along with better volumes from the existing portfolio.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

Buy Granules India Ltd for the Target 950 by Emkay Global Financial Services Ltd