Buy Gland Pharma Ltd for the Target Rs 2,300 by Motilal Oswal Financial Services Ltd

Broad-based growth across markets drives earnings Complex pipeline/GLP-1 contracts to drive growth momentum

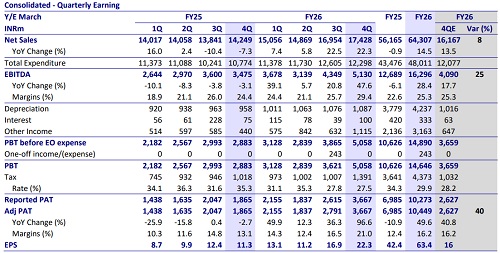

* Gland Pharma (GLAND) exhibited better-than-expected financial performance, with 8%/25%/40% beat on revenue, EBITDA, and PAT for the quarter. This is the second consecutive quarter of an earnings beat.

* Core markets and Cenexi delivered superior revenue growth for the quarter.

* Improved operating leverage led to the highest EBITDA margin in 12 quarters.

* Product launches led to an all-time high revenue in the core markets of GLAND.

* The Europe segment witnessed a healthy scale-up in inactivated vaccine and sterile ophthalmic gel, driving revenue for the quarter.

* We raise our earnings estimate by 8%/10% for FY27/FY28, factoring in:

a) a healthy pace of product launches in core markets

b) improvement in profitability of the Cenexi business

c) currency depreciation tailwinds.

* We value GLAND at 27x 12M forward earnings to arrive at a TP of INR2,300. We expect a 19% earnings CAGR over FY26-28 on the back of a complex product pipeline comprising injectables, scale-up of CDMO contracts, and improved synergy from Cenexi. GLAND is geared to benefit from the GLP-1 opportunity as well. Reiterate BUY.

Healthy revenue growth; operating leverage drives margins YoY

* GLAND’s 4QFY26 revenues grew 22.3% YoY to INR17.4b (our estimate: INR16.2b).

* Gross margin (GM) expanded 30bp YoY to 66.1%.

* EBITDA margin expanded 500bp YoY to 29.4% (our estimate: 25.3%). On ex-Cenexi basis, the EBITDA margin was 40.2% (up 190bp YoY).

* EBITDA grew 47.6%YoY to INR5.1b (our estimate: INR4.1b).

* Adj. PAT grew 96.6% YoY at INR3.7b (our estimate: INR2.6b).

* For FY26, Revenue/EBITDA/PAT grew 14.5%/28.4%/49.6% YoY to INR64b/INR16.3b/INR10.5b.

Highlights from the management commentary

* GLAND guided for 12-13% YoY growth in revenue in FY27 on a CC basis. It does not include any business prospects from GLP-contracts.

* The overall YoY revenue growth is expected to improve over the next three years, with a meaningful increase expected in FY29.

* GLAND expects Cenexi to achieve a mid-single-digit EBITDA margin in FY27 vs an EBITDA loss (2%) in FY26.

* GLAND reported a 9%/5% revenue share/milestone income for 4QFY26.

* Management indicated capex of INR20b over the next five years for ophthalmics, alongside dedicated capex for certain CDMO contracts. GLAND also aims to invest in building capacity with respect to blow-fill technologies.

* In the GLP-1 segment, GLAND signed 8 contracts, while additional 6-7 contracts are expected to be signed shortly.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412