Buy Premier Energies Ltd for the Target Rs 1,195 by Motilal Oswal Financial Services Ltd

Sustains margins, beats estimates

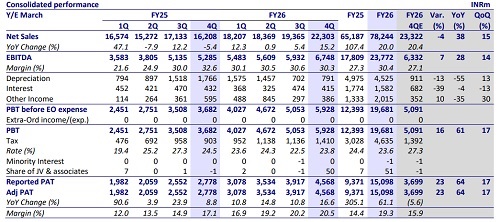

* Strong 4Q: Premier Energies (PEL) delivered a strong performance, with an EBITDA of INR6.7b (7% beat), as EBITDA margin remained strong at 30% (vs. our estimate of 27%). APAT beat our est. by 23% at INR4.6b, owing to lower-than-expected depreciation, finance costs, and tax. FY26 revenue/EBITDA/APAT stood at INR78b/ INR24b/INR15b (+ 20%/33%/61% YoY). Module/Cell production for the year was 3.6/2.3GW (+47%/41% YoY).

* Key things we liked about the result:

1) EBITDA margin was sustained through continued cost optimization initiatives, operational efficiency improvements, operating leverage, and scale benefits

2) The 5.6GW module manufacturing facility was commissioned at FY26 end (in line with the guidance). PEL continues to maintain industry-leading cell utilization levels, with Cell CUF at 84% in 4QFY26

3) Management remains constructive on growth opportunities in both European and US markets and is evaluating the establishment of cell manufacturing capacity in the US and expects to finalize strategic partnership decisions over the coming months.

* Key monitorables:

1) Timely commissioning and ramp-up of the upcoming 7GW cell manufacturing capacity (4.8GW by Jun’26 and the remaining 2.2GW by Sep’26)

2) The impact of volatility in commodity prices

3) flow of new orders amid a slower utility-scale tendering activity.

* Valuation : We had earlier factored in earnings contributions from the BESS and inverter businesses commencing from FY27. However, these contributions have now been deferred to FY28 and beyond. Additionally, we have revised our EBITDA margin assumptions upward to 25%/23% for FY27/FY28 (vs. 24%/ 21% earlier), resulting in a 2%/7% upward revision to our FY27/ FY28 EBITDA estimates. We now value the domestic module business at 14x FY28E EBITDA (vs. 13x earlier) and the new business segment at 10x FY28E EBITDA (unchanged). The sum of these segment valuations (adjusting for net debt) resulted in a TP of INR1,195. Reiterate BUY

Highlights of the 4QFY26 performance

* The 5.6GW module manufacturing plant is expected to ramp up to full capacity over the next two months.

* The order book surged 66% YoY to INR140b, with more than two-thirds expected to be executed in FY27 and a substantial portion of solar cell orders extending into FY28.

* FY27 capex guidance stands at INR51b, with overall planned capex of ~INR120b across FY26 to FY28, covering ingots, wafers, batteries, and inverters.

* Management is targeting a Debt/Equity ratio of ~1x and a Debt/EBITDA ratio of 1.5x or below.

* Management sees strong opportunities in both Europe and the US. Discussions regarding a US solar cell joint venture with Heliene have resumed, with site evaluations restarted and a decision on strategic partnerships expected within the coming months.

* Premier has completed the acquisition of a 51% stake in TransCon, which reported annual revenue of INR4.2b and PAT of INR0.4b, with management noting a sharp improvement in EBITDA and PAT margins post-acquisition.

Valuation and view

* The valuation of PEL has been derived through a sum-of-the-parts (SoTP) methodology: The domestic module business is valued at 14x FY28E EBITDA. The new business segment is valued at 10x FY28E EBITDA, consistent with domestic peer valuations. The sum of these segment valuations (adjusting for net debt) results in a TP of INR1,195. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)