Buy SAIL Ltd for the Target Rs.225 by Motilal Oswal Financial Services Ltd

Strong earnings in 4Q; outlook improves with better steel prices and cost controls

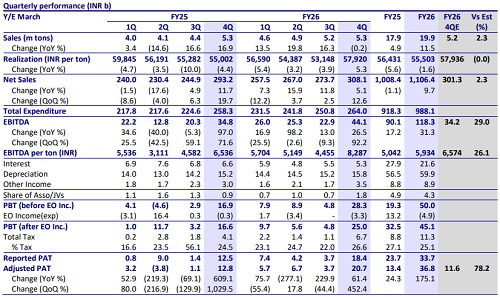

* SAIL reported in-line revenue of INR308b (+5% YoY and +13% QoQ), driven by healthy volume growth and NSR.

* EBITDA stood at INR44.9b (+27% YoY and +92% QoQ), against our estimate of INR34b during the quarter, led by better NSR with operational efficiency gains of INR4.3b, offsetting higher input costs of INR2.7b during 4QFY26. This translates into EBITDA/t of INR8,287/t (vs. our est. of INR6,574/t), rising 27% YoY and 86% QoQ in 4QFY26.

* Adj PAT came in at INR21.7b (vs our est. INR11.6b), rising 69% YoY in 4QFY26, compared to INR3.7b in 3QFY26. This was mainly driven by strong operating performance and higher other income.

* Volumes during the quarter were in line with our estimate, where crude steel production stood at 5.1mt (flat YoY and +5% QoQ), and sales volume stood at 5.3mt (flat YoY and +3% QoQ), led by aggressive inventory liquidation and improved market outreach. Volume contribution from NMDC steel (NSL) declined to merely ~0.1mt in 4QFY26, as SAIL discontinued the sale of the product.

* ASP for the quarter came INR57,920/t, as expected, rising 5% YoY and 9% QoQ, driven by an increase in steel prices during the quarter.

* In FY26, sales volume stood at 19.9mt (+12% YoY), which was slightly offset by an NSR decline of 2% (INR55,500/t), resulting in revenue of INR1,106b (+10% YoY).

* Out of 19.9mt sales volume in FY26, the third-party contribution stood at 1.17mt. Of this, NSL contributed ~1.12mt, and RINL contributed 0.05mt (mainly during Feb-Mar’26). On account of strong volume growth, EBITDA for FY26 stood at INR118b (+31% YoY; INR5,934/t) and Adj. PAT was INR36.8b (+175% YoY).

Highlights from the management commentary

* For FY27, management guided sales volumes of ~22.5mt, compared to ~20mt achieved in FY26 (includes ~0.6-0.7mt of RINL-related sales volumes). The higher blast furnace productivity, oxygen enrichment, higher PCI usage, and shutdown of inefficient smaller furnaces are enabling production beyond rated capacity.

* SAIL reduced inventory by nearly 0.9mt during FY26, including 0.4mt reduction in finished steel inventory and 0.5mt reduction in work-inprogress inventory.

* Management indicated that Apr-May’26 realizations improved sharply, with long product NSR jumping to INR57,000-57,800/t, whereas the flat product NSR increased to INR56,000-56,700/t, implying QoQ NSR improvement of roughly INR4,000-5,000/t in 1QFY27.

* Coking coal procurement cost increased materially from INR18,200/t in 4QFY26 to INR21,000/t in Apr’26 and INR21,800/t in May’26. Management expects the increase in coal costs to result in an INR1,400-1,500/t rise in production cost during 1QFY27 after inventory blending effects. Overall, management believes higher steel prices should support profitability in FY27, despite higher input costs.

* FY26 capex stood at INR91b vs the initial guidance of INR100b. Management guided for a higher capex of INR150b in FY27. SAIL expects annual capex to further increase to INR180-190b in FY28 and stabilize at around 200-250b annually during the expansion phase

Valuation and view

* NSR recovery with operational efficiency led to strong earnings for SAIL in 4QFY26. This earnings trend is expected to improve further in 1Q, led by steel price recovery and better volumes, backed by inventory liquidation, offsetting the input cost inflation.

* We increase our FY28 revenue estimates by 4% to reflect improving steel prices and incremental volume from RINL, translating into an EBITDA/PAT rise by 6% and 8%, respectively.

* We reiterate our BUY rating on the stock with a revised TP of INR225 (premised on 8.5x EV/EBITDA on FY28 estimate).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)