Buy Devyani International Ltd for the Target Rs 165 by Motilal Oswal Financial Services Ltd

KFC’s print improves; operational profitability in line

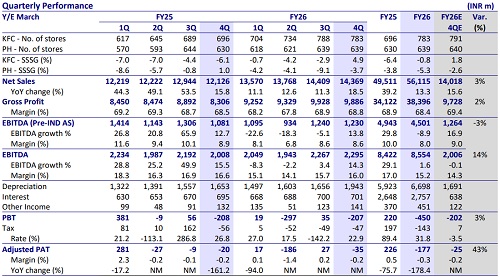

* Devyani International’s (DEVYANI) consolidated revenue grew 19% YoY in 4QFY26. The Indian revenue was up 18% YoY, led by KFC and the Skygate acquisition. KFC’s SSSG was better than expected, while PH’s same-store sales continued to decline in 4Q. The company is witnessing a gradual recovery in demand trends across its brands.

* KFC’s sales rose 15% YoY, with SSSG improving to 5% (base -6.1%; -3% in 3Q). KFC closed five stores in 4Q. Pizza Hut (PH)’s revenue declined 4% YoY, with SSSG at -3.7% YoY. There was no store addition in 4Q. Franchise brands’ (Costa Coffee, NYF, and SK) revenue grew 3% YoY, while its acquired brands’ (Vaango and Sky Gate) revenue stood at INR911m.

* India ROM was up 13% YoY to INR1.2b while margin contracted by 50bp YoY to 12.9%. KFC’s ROM improved 70bp YoY to 17% backed by strong GM expansion (+120bp), while PH’s ROM stood at -1.4% vs. +0.7% in base.

* International revenue grew 20% YoY to INR5b with RoM at INR890m (vs. INR677m in 4QFY25), and margin expanded 160bp YoY to 17.7%.

* Weak unit economics have remained a key overhang for QSR players over the past couple of years amid aggressive store expansion. 4QFY26 saw store rationalization, indicating the company’s focus on fixing the unit economics. KFC's performance is now witnessing an improving trajectory, aided by its consumer recruitment strategy. The proposed Devyani–Sapphire merger, likely to be completed by the end of FY27, is expected to unlock scale efficiencies and enhance execution capabilities across brands and geographies. We reiterate our BUY rating on the stock and value the entity at 25x Mar’28E EV/EBITDA (pre-Ind AS) to arrive at our TP of INR165.

FY26 revenue/EBITDA (pre-IND AS) up 13%/down 9% YoY

* Management believes geopolitical disruptions disproportionately impact smaller players, potentially aiding market share gain for larger organized QSR operators.

* Devyani undertook only a marginal price increase of less than 0.5% on its menu at the portfolio level. Future pricing actions will remain dependent on the inflationary environment and commodity trends.

* Management emphasized that business disruption from the ongoing gas crisis has been minimal, despite supply challenges related to the Middle East conflict.

* The Devyani-Sapphire merger is expected to be completed by the end of FY27.

Valuation and view

* We broadly retain our EBITDA estimates for FY27 and FY28.

* Management remains committed to improving ADS and profitability across the existing network and brands and will adopt a more cautious approach to future store openings.

* The merger of Devyani and Sapphire is expected to unlock meaningful scale benefits, improve unit economics through operating leverage and revised commercial terms, and enhance execution across brands and geographies.

* The merger is expected to deliver recurring annual synergies of ~INR2.2b, driven by lower Pizza Hut operating costs, reduction in overall corporate overheads, and other operational efficiencies. We estimate an EBITDA gain of ~INR500m in FY28, considering weak QSR industry performance and any delay in the occurrence of synergy benefits (refer to our detailed merger note).

* We value the entity at 25x EV/EBITDA (pre-IND AS) on Mar’28E, which implies a per share value of INR165. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412