Buy P N Gadgil Jewellers Ltd for the Target Rs 715 by Motilal Oswal Financial Services Ltd

Beat on revenue growth; miss on margin

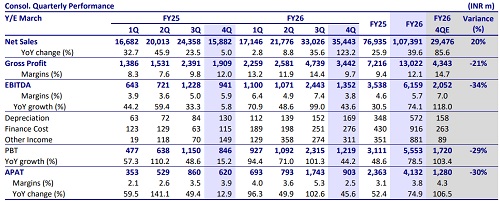

* PN Gadgil Jewellers (PNGJL) reported strong consolidated revenue growth of 123% YoY to INR35.4bn (vs est. INR29.5bn) in 4QFY26. It was driven by a robust same-store sales growth (SSSG) of 86%. Retail revenue grew 102% YoY, franchisee revenue increased 132%, while e-commerce sales rose 67%; bar & coin sales surged >200% to INR14b. Customer footfalls increased 10%, with a healthy conversion rate of 93%.

* PNGJL added 12 stores during the quarter, taking the total store count to 78 (48 COCO, 17 FOCO, 13 LiteStyle) across 36 cities. The company plans to add 25 stores in FY27 (5 COCO and 20 FOCO), with majority of the expansion focused outside Maharashtra.

* However, gross margin contracted sharply by 230bp YoY to 9.7% (vs est. 14.7%), primarily due to a higher gold bar and coin mix (150bp impact), lower studded jewellery contribution (30bp impact), and elevated promotional discounts during Foundation Day and Gratitude Day campaigns (50bp impact). Consequently, EBITDA margin witnessed a sharp dip by 210bp YoY to 3.8%. Management maintained FY27 PAT margin guidance of ~4%. We model PAT margins of ~3.5% for FY27/FY28.

* We model revenue, EBITDA, and APAT CAGR of 17%, 13%, and 10% over FY26-28E. Management highlighted that an increase in gold customs duty from 6% to 15% could moderate bullion demand and accelerate old gold exchange trends. PNGJL remains focused on increasing old gold contribution from the current ~40% to 50% through its ‘Suvarna Swarajya’ initiative. Additionally, the company plans to increase the hedging ratio to 75-80% from ~60% in FY26 to reduce margin volatility. Given the ongoing strategic initiatives and long-term growth visibility, we reiterate our BUY rating on the stock with a TP of INR715.

Key takeaways from the management commentary

* Management guided revenue of INR135b for FY27. Growth is expected to be supported by strong SSSG and continued store expansion.

* Franchisee margins were structurally lower at around 2.5%-3%, which also impacted consolidated margins.

* Make-to-order jewellery contribution remained stable at 30–35% of sales. Outside Maharashtra, the make-to-order contribution stood at ~22% of sales.

* Management stated that the QIP resolution remains valid till Aug’26. The company currently does not require immediate capital infusion as internal accruals remain sufficient to support growth plans.

Valuation and view

* We decrease our EPS estimates by 3% for FY27 and 1% for FY28.

* We model revenue, EBITDA, and APAT CAGR of 17%, 13%, and 10% over FY26– 28E. Management highlighted that an increase in gold customs duty from 6% to 15% could moderate bullion demand and accelerate old gold exchange trends. PNGJL remains focused on increasing old gold contribution from the current ~40% to 50% through its ‘Suvarna Swarajya’ initiative. Additionally, the company plans to increase the hedging ratio to 75–80% from ~60% in FY26 to reduce margin volatility. Given the ongoing strategic initiatives and long-term growth visibility, we reiterate our BUY rating on the stock with a TP of INR715.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412