Sell Tata Motors Passenger Vehicles Ltd for the Target Rs.303 by Motilal Oswal Financial Services Ltd

Healthy performance revival across segments Multiple headwinds ahead

* Tata Motors Passenger Vehicles’ (TMPV) 4Q PAT at INR58.8b was well above our estimate due to better-than-expected performance at both the Indian business and JLR. While Indian margins expanded 90bp YoY to 8.7% (vs our estimate of 7%), JLR EBIT margins sharply expanded from -6.8% in 3Q to 9.2% in 4Q due to improved volumes, higher product capitalization, reduced depreciation, and benefit from forex gains (not quantified), even as gross margins declined QoQ.

* 4Q performance has certainly been ahead of estimates, both in India and at JLR. While the Indian PV demand outlook remains positive, it is expected to see margin pressure in the near term, given the material surge in input costs. Further, JLR continues to face multiple headwinds, both on the demand and cost front. While JLR has embarked on a major cost reduction initiative, it is likely to only help partially offset the current headwinds. Given the significant challenges at JLR and the continued geopolitical uncertainty, we reiterate our Sell rating on the stock with a SoTP-based TP of INR303 per share (based on FY28E). We value both JLR and India PV business at 2x and 13x EV/EBITDA, respectively.

Healthy performance revival both in India and at JLR

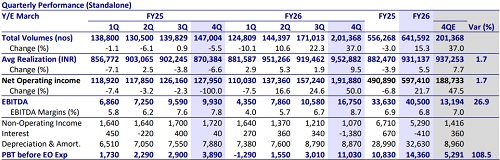

* TMPV reported a profit of INR58.8b in 4Q, well ahead of our estimate of INR22.3b due to better-than-expected performance at both the Indian business and JLR.

* Standalone Indian business saw a strong 50% YoY increase in revenues to INR192b, in line with our estimates. However, margins expanded 90bp YoY to 8.7% (vs our estimate of 7%). As a result, PBT beat our expectations, almost tripling YoY to INR11b.

* JLR volumes had recovered significantly in 4Q as production returned to normal levels, though still posting a 14.4% YoY decline. EBIT margins sharply improved from -6.8% in 3Q to 9.2% in 4Q due to improved volumes, higher product capitalization, reduced depreciation, and benefit from forex gains in other expenses (not quantified), even as gross margins declined QoQ. PBT beat our estimates, coming in at GBP458m, having fallen ~48% YoY.

* RoCE for the 12-month rolling period stood at 1.2%.

* The Indian business’s FY26 Revenue/EBITDA/PBT rose 22%/20%/33% YoY to INR597b/40.5b/14.4b, respectively.

* JLR, on the other hand, saw a full-year Revenue/EBITDA decline of 21%/63% to GBP22.9b/GBP1.5b. However, its PBT sharply declined to GBP14m from GBP2.5b YoY.

* JLR has delivered a negative FCF of GBP2.2b in FY26.

* Net consolidated automotive debt stood at INR307b, with a large portion attributed to JLR (INR327b), while the Indian business continues to be net cash.

Valuation and view

4Q performance has certainly been ahead of estimates, both in India and JLR. While the Indian PV demand outlook remains positive, the company is expected to see margin pressure in the near term, given the material surge in input costs. Further, JLR continues to face multiple headwinds, both on the demand and cost front. While the company has embarked on a major cost reduction initiative, it is likely to only help partially offset the current headwinds. Given significant challenges at JLR and the continued geopolitical uncertainty, we reiterate our Sell rating on the stock with an SoTP-based TP of INR 303 per share (based on FY28E). We value both JLR and the Indian PV business at 2x and 13x EV/EBITDA, respectively.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412