Buy Inventurus Knowledge Solutions Ltd for the Target Rs.1,953 by Motilal Oswal Financial Services Ltd

Revenue in line; beat on profitability

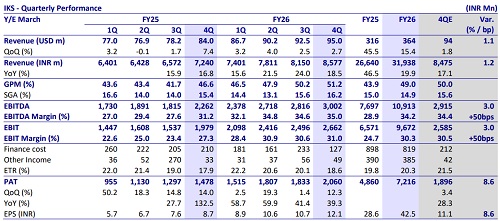

Inventurus Knowledge Solutions’ (IKS) 4QFY26 USD revenue rose 12.6% YoY to USD364m, led by strong performance from top clients and healthy contribution from new deals and partnerships. INR revenue grew 18.5% YoY to INR8.6 (estimate INR8.5b), while EBITDA rose 41.8% YoY to INR3.0b (estimate INR2.9b) and margin stood at 35.0% (528bp YoY, 40bp QoQ).PAT grew 12.3% QoQ and 39.3% YoY to INR2.1b, (estimate INR1.9b). We expect its revenue/EBITDA/PAT to grow at 17%/20%/24% CAGR over FY26-28. We value the stock at 30x FY28E EPS to arrive at our TP of INR1,953. We reiterate our BUY rating on the stock.

Our View: US healthcare cost pressure remains a structural tailwind

* The US healthcare delegated-task TAM is estimated at >USD260b, while the currently outsourced TAM stands at ~USD35b and is growing at ~12%. Management indicated that sustaining growth above 12% would imply continued market share gains.

* Total clients: FY26: 600 /FY25: 500/FY24: 850 (client rationalization is progressing well).

* The company has revised its GTM strategy:

a) mid-sized health systems with full-platform offerings

b) large health systems approached through a ‘landand-expand’ strategy, initially focused on point solutions such as RCM, coding, and patient access.

* With headcount growing just 5% YoY amid 15.4% USD revenue growth, the business model reveals clear non-linearity in revenue generation, indicating efficiency gains and scalable operations.

* Key AI focus areas include: autonomous clinical documentation, ambient AI scribing, autonomous coding, prior authorization, patient onboarding, scheduling optimization, eligibility verification, patient engagement, and revenue cycle management.

* IKS believes that hybrid AI-plus-human workflows may drive superior physician adoption and greater burden reduction compared with purely autonomous competitors.

IKS Business Highlights

* The company partnered with Certilytics to integrate payer rules and provider workflows through a combination of agentic AI and human oversight.

* It also signed a multi-year partnership with Holyoke Medical Center to drive AI-led clinical and administrative transformation.

* Additionally, IKS expanded its engagement with Mission Community Hospital to deliver advanced in-hospital AI capabilities aimed at improving operational efficiency.

* On the RCM and VBC front, the company broadened its partnership with a top-five US health system to expand services across additional regions and states

Valuation and view

We believe IKS is uniquely positioned to benefit from long-term structural tailwinds in the US healthcare technology, supported by its strong financial profile, differentiated tech-first platform, and expanding market opportunity. We reiterate a BUY rating on IKS with a TP of INR1,953, valuing it at 30x FY28E EPS (~24% EPS CAGR over FY26-28E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412