Buy Siemens Energy India Ltd for the Target Rs. 3,800 by Motilal Oswal Financial Services Ltd

Demand and pricing power remain strong

Siemens Energy in its analyst meet highlighted the opportunity pipeline across domestic and international markets for power transmission business. Management is optimistic about 1) 10-15% YoY growth on a sustainable basis for power transmission segment; 2) margin improvement, aided by pricing power and operating leverage benefits; 3) adequate capacity utilization of new capacities that will come in FY27 as enquiry levels remain strong. The company focuses on VSCbased HVDC projects, and in the near term, limited opportunities in these projects can limit domestic HVDC order inflows for the company, though TAM remains strong for non-HVDC projects. Power generation business, which is dependent on base industries like cement, steel, sugar, ethanol etc can grow slightly slower than power transmission business. We broadly maintain our estimates and retain BUY on Siemens Energy with an unchanged TP of INR3,800, based on 60x two-year forward earnings.

Key takeaways from analyst meet

Power transmission remains key growth driver

The power transmission segment remains a key growth engine, supported by strong sector tailwinds in grid expansion, stabilization, and digitalization. Management highlighted technology leadership in transformers, AIS/GIS switchgear, grid solutions (FACTS, STATCOMs, SYNCONs) and HVDC VSC, noting that ~30% of India’s HVDC capacity has been built using Siemens technology, along with marquee wins such as large STATCOM orders and India’s first SF6- free 145 kV circuit breaker. The company focuses on VSC-based HVDC projects, and we expect the outcome of the South Olepad HVDC project in the next few days. While near-term VSC-based HVDC opportunities remain limited, demand stays strong for non-HVDC transmission projects. New transformer and switchgear capacities are targeted for commissioning by late FY26/early FY27, and margins are expected to improve as pricing power remains intact and operating leverage plays out.

Power generation outlook remains stable

The segment delivered double?digit revenue growth with stable profitability in FY25, underpinned by its large installed base and strong services franchise. Management highlighted that ~55% of India’s large steam turbines and ~25% of gas turbines are built using Siemens energy’s technology, supporting ongoing opportunities in services, modernization and upgrades. Management expects high-single digit growth in the power generation business, driven by stable demand for industrial steam turbines in cement, steel, sugar and ethanol, and continued services activity, while gas turbine demand in India is limited by fuel availability. The company would also be eyeing opportunities in nuclear power, where it can target large steam turbines. Along with this, the company would also target gas turbines for data center-related opportunities.

Future growth strategy

Looking ahead, Siemens Energy remains optimistic about its growth trajectory across its key segments. In power transmission, we expect the company to benefit from the planned doubling of its transformation capacity by 2032, driving demand for transformers, AIS/GIS, HVDC VSC and grid?stabilization solutions, with exports providing an additional growth lever. In power generation, the company sees steady demand from the upkeep, flexibilization and modernization of India’s large steam and gas turbine fleet, incremental nuclear capacity, and rising need for efficient captive and industrial generation. In Industries and New Energy, management is focusing on electrification and automation of process industries, growth in data centers and maritime electrification, and emerging platforms such as PEM electrolysers and power?to?X under the Green Hydrogen Mission. With a healthy share of 23% of revenue coming from exports, and within segments, a healthy share of 26% from services, we expect margin support to be visible going forward.

Financial outlook

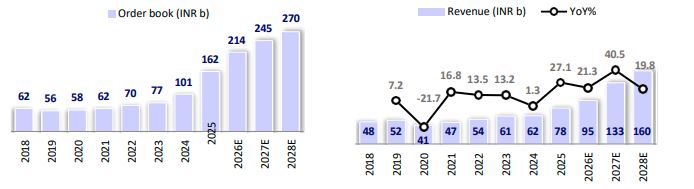

We broadly maintain our estimates. We expect revenue/EBITDA/PAT CAGR of 27%/32%/34% over FY25-28E, led by strong growth across power transmission (39% CAGR) and power generation (9% CAGR). Power transmission segment growth will be supported by commissioning of capacities by FY26-end/early FY27. We expect EBITDA margins of 20.7%/21.7%/21.8% for FY26E/FY27E/FY28 as we expect margin improvement to come from stable gross margin and operating leverage benefits as revenue scales up.

Valuation and view

Siemens Energy is currently trading at 72.7x/49x/40.1x P/E on FY26E/27E/28E EPS. We broadly maintain our estimates and reiterate BUY with an unchanged TP of INR3,800, based on 60x two-year forward earnings.

Key risks and concerns

Key risks to our thesis can come from a slowdown in ordering and supply chain issues, thus impacting margin.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412