Buy LT Foods Ltd For Target Rs.460 by Motilal Oswal Financial Services Ltd

Consistent growth trajectory continues

Earnings below estimates due to higher interest cost

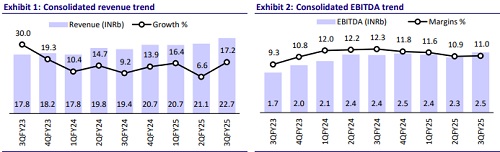

* LT Foods (LTFOODS) reported a healthy quarter with revenue growing 17%, led by Basmati and Other Specialty Rice (up 17% YoY) and Organic Foods (up 26% YoY). EBITDA margins took a hit of 130bp due to higher freight costs.

* The higher freight cost impact will weigh on the company’s margins for 4QFY25/1QFY26 before tapering down with renewed contracts (at lower rates). Additionally, paddy procurement has been at a lower rate for the current year (~INR32/kg, i.e. down 10-15% YoY), which will help improve margins in FY26.

* We largely maintain our EPS estimates for FY25/FY26/FY27. We reiterate our BUY rating on the stock with a TP of INR460 (16x FY27E EPS).

Volume growth remains strong, led by healthy demand

* In 3QFY25, consolidated revenue stood at INR22.7b (+17% YoY, +8% QoQ), in line with our est. EBITDA grew 14%/9% YoY/QoQ to INR2.5b during the quarter (in line). EBITDA margin contracted 130bp YoY, while it expanded 10bp to 11% (in line).

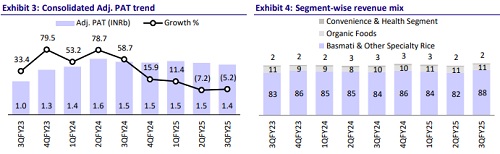

* Adj. PAT declined 5%/3% YoY/QoQ to INR1.4b vs. estimate of INR1.5b, with earnings missed largely due to higher-than-anticipated finance costs of INR236m (+28% YoY/+21% QoQ).

* The Basmati & Other Specialty Rice segment grew 19% YoY, led by strong growth in the International segment (up 22% YoY), while domestic grew ~14% YoY. Gross/EBITDA margins stood at 32.4%/11.7%, down 160/310bp YoY, due to higher input and freight costs.

* Organic foods grew 26% YoY, while gross/EBITDA margins expanded 860/290bp YoY to 42.6%/11.8%.

* The Convenience & Health segment’s revenue declined 16% YoY, primarily due to the discontinuance of Daawat Sehat. Gross margin expanded 410bp to 41.1% and operating loss stood at INR42m.

Highlights from the management commentary

* Guidance: The company guided for margin improvement in FY26, led by better pricing strategy and lower freight cost. The Organic Foods segment is expected to grow 10% in FY26 (revenue of INR10b+) with EBITDA margins of over 14%.

* Basmati Business: The company is seeing healthy demand growth in both India and international markets, which has led to a higher inventory stock in 3QFY25. The management guided the overall volume growth for FY25/FY26 to be in the range of 12-13%.

* Freight Cost: EU and US are two regions that have been impacted by Red Sea issues. US freight costs remain high, while EU freight costs have started to decline. Last year, freight costs were ~5% of sales, which have increased to 7.2% now. However, the company expects freight costs to decrease to 6% in FY26.

Valuation and view

* LTFOODS has reported consistent performance over the longer term and is expected to continue this momentum, led by: higher growth in the Basmati and Other Specialty Rice segment in both Indian and international markets, and margin expansion supported by lower input prices and an increasing mix of Organic and Convenience & Health segments.

* We estimate a CAGR of 15%/19%/36% in revenue/EBITDA/Adj. PAT over FY24- FY27. We reiterate our BUY rating on the stock with a TP of INR460 (16x FY27E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412