Neutral Pidilite Industries Ltd for the Target Rs. 1,550 by Motilal Oswal Financial Services Ltd

Growth trajectory sustains; rich valuation limits upside

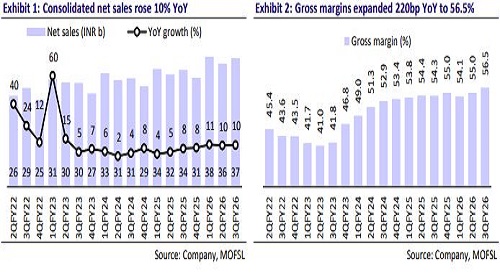

* Pidilite Industries (PIDI) reported consolidated revenue growth of 10% YoY (in line) in 3QFY26. Standalone revenue grew 11% YoY, led by 9% underlying volume growth (UVG) (vs est. 12%). Ex-exports, growth was at ~12%, as exports declined 13% due to the US tariff impact.

* In the C&B business, value/volume growth stood at 12%/10% YoY, supported by mix and premiumization. The B2B segment saw 3% value growth and 7% volume growth, impacted by export headwinds, though domestic B2B grew in the mid-teens. The domestic business (C&B + B2B) delivered ~11% UVG. Price growth was driven by selective price laddering, premium mix, and tactical pricing in select categories, with management targeting a ~100–150bp price–volume gap on a sustained basis.

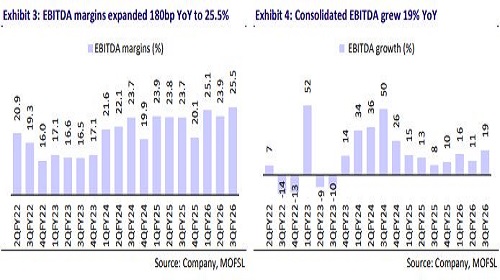

* Gross margin (GM) expanded 220bp YoY to 56.5%, at an all-time high on benign RM prices and better mix (higher B-C mix). VAM dipped to ~USD830/t in 3QFY26 from USD884/t in 3QFY25. GM is expected to remain stable, with no major volatility in VAM prices. PIDI continues to prioritize reinvestment in brand building and customer acquisition. EBITDA margin expanded 180bp YoY to 25.5% (adjusted to one-time impact of INR523m for the labor codes). EBITDA grew 19% YoY (est. 13%).

* Consolidated EBIT growth for the consumer business was healthy at 21% YoY (17% in 9MFY26, 10% in FY25). B2B business EBIT declined 2% (9% in 9MFY26, 53% in FY25).

* The company aspires to sustain double-digit volume growth. PIDI’s volume growth trajectory remains encouraging, especially amid a challenging demand environment. Operating margins remain elevated (>24% EBITDA margin), and it will be crucial to monitor whether the company can sustain these levels. We model a 13% revenue and 14% EBITDA CAGR over the medium term. Given the rich valuations, we reiterate our Neutral rating on the stock with a TP of INR1,550 (50x Dec’27E EPS).

Steady performance; volume up 9%

* Steady volume growth sustains: Consol. sales grew 10% YoY to INR37.1b (est. INR37.8b). Underlying volume growth remained strong at 9% (est. 12%, 10.3% in 2QFY26). UVG was 10% for C&B businesses and 7% for B2B businesses.

* Healthy growth in C&B: Consumer & Bazaar (C&B) segment revenue increased 11% YoY to INR29.7b (est. INR29.7), with segmental EBIT growing 21% YoY to INR9.5b (est. INR8.9b). It is adjusted by INR415m, reflecting the impact of labor code implementation. Segmental EBIT margins expanded 260bp YoY to 32%.

* Muted B2B performance: B2B segment revenue rose 3% YoY to INR7.8b (est. INR8.5b). The segmental EBIT decreased 2% to INR1.3b (est. INR1.4b). It is adjusted by INR108m, reflecting the impact of the labor code implementation. Segmental EBIT margins contracted 80bp YoY to 16.8%.

* Improvement in margins - Gross margins expanded ~220bp YoY to 56.5% (est. 55%), at an all-time high. The cost impact of INR523m arising from the implementation of the new labor codes has been treated as an exceptional item. Employee expenses rose 9% YoY (adjusted INR523m due to new labor codes), and other expenses rose 13% YoY. EBITDA margin expanded 180bp YoY to 25.5% in 3QFY26 (est. 23.8%). We also adjusted segmental EBIT by allocating the cost proportionately to segment revenue.

* Double-digit growth in profitability: EBITDA grew 19% YoY (est. 13%) after adjusting for an INR523m impact of labor codes. PBT grew 19% YoY to INR9.0b (est. INR8.6b). Adj. PAT increased 22% YoY to INR6.8b (est. INR6.4b). ? In 9MFY26, net sales, EBITDA, and APAT grew 10%, 15%, and 17%.

* Subsidiary performance: Domestic subsidiaries’ C&B revenue grew 13% YoY and EBITDA grew 27%. Domestic B2B revenue declined 8% YoY and EBITDA declined 52%. Middle East and Africa revenue grew 3% and EBITDA rose 2%. Asia revenue grew 9% and EBITDA grew 26%

Highlights from the management commentary

* The domestic B2B segment delivered mid-teen growth, and management plans to bring the overall B2B business back to at least mid-teen growth levels. Exports form a relatively small part of the business. However, the pigments segment, which has direct exposure to the US, along with allied B2B segments such as footwear, leather, and textiles, faced pressure through 3Q, though management believes the worst impact is largely behind.

* The company expects to sustain double-digit volume growth, driven by an improving performance of growth brands and a robust pipeline of pioneering innovations, premium products.

* Price growth is driven by selective price laddering, mix/premiumization, and tactical pricing in a few categories, with management aiming to sustain a ~100– 150bp price–volume gap over time, though not necessarily on a consistent QoQ basis.

* The growth in Roff will continue, given the growth in tile markets. Tile adhesive is a higher-value substitute for cement, and while overall tile demand in India is growing at ~8–10%, the real growth driver is the rapid increase in tile-adhesive penetration in tile fixing (high double-digit growth).

Valuations and view

* We maintain our EPS estimates for FY27 and FY28.

* PIDI’s core categories still enjoy a GDP multiplier. The advantage of penetration and distribution can help PIDI deliver healthy volume-led growth in the medium term. EBITDA margin is already high (>24% in 9MFY26). We do not estimate much expansion as growth drivers (consumer acquisition, distribution expansion, and brand investments) will require high opex. We build in a CAGR of 13%/14%/15% in revenue/EBITDA/PAT during FY26-28E.

* PIDI stands out for its market-leading position in the adhesives market, along with a strong brand and a solid balance sheet. However, we believe the current valuation limits the upside potential. As a result, we reiterate our Neutral rating on the stock with a TP of INR1,550 (premised on 50x Dec’27E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412